Simulations of a random system since SPY inception show that nearly 35% of random traders, human or automated, have made some profit. However, only 1% of random traders were lucky enough to exceed the buy and hold return with dividend reinvestment, estimated at 8.60%. Even at that significance level, the market is still overly generous compared to other recreational gambling systems and whoever prefers those over the market is ignorant of these important statistics.

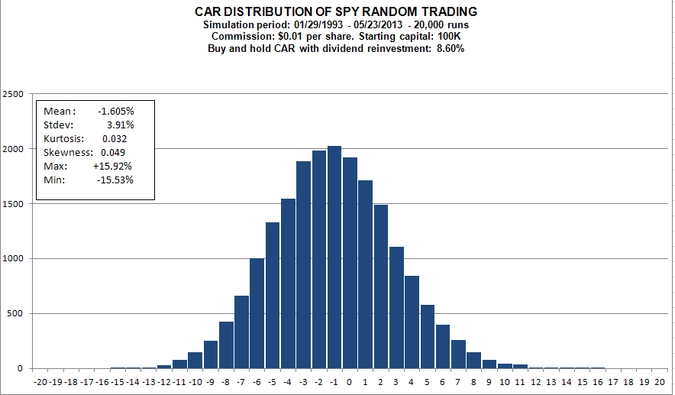

A gambler may have more fun trading the market by flipping a coin and a much higher probability of breaking even or making a profit than with any other gambling system. Below is the CAR (compound annual return) distribution of a random SPY trading system that flips a coin at every close and enters a long position at the next open if the outcome is heads or a short position if it is tails. Positions are held open and are exited when a reverse signal is generated . Commission was set at 1 cent per share:

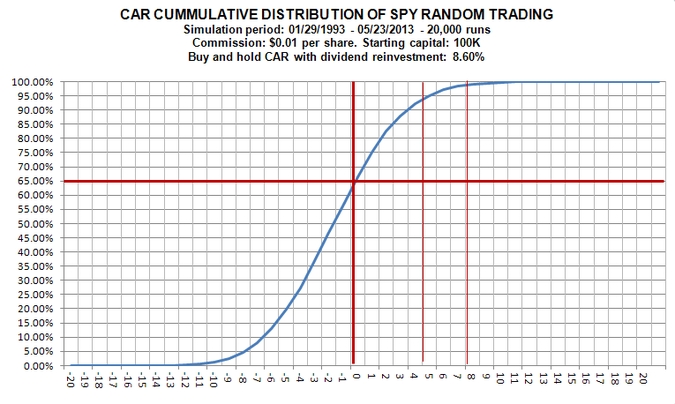

It may be seen from the above distribution of 20,000 random systems that flipped a coin to trade SPY since inception that the mean CAR is -1.605% and the standard deviation is 3.91%. The distribution has very small kurtosis and skewness and it is nearly normal. The cumulative distribution is shown below:

The cumulative distribution tells us that nearly 35% of all random traders/systems made a profit (vertical thick red line). Even about 1 out of 100 random traders exceeded the significant buy and hold return with dividend reinvestment of about 8.60% for the period. This is much better than any gambling system has to offer for recreational traders relying on charts, indicators, candlesticks, and other methods that are no better than random trading on the average unless they can systematically produce of return above the buy and hold, which unfortunately for them in this case is much above the 95% confidence level that requires return of about 5% only.

The implication from these statistics are many and below are the two most important, in my opinion:

(1) If one wants to gamble, then the market is the best place to do it but one must do it right and avoid leveraged schemes, like futures and forex, that can drive an account to zero in one day. Gamblers also provide liquidity for serious traders and fund managers and contribute to price discovery while they have a much higher chance to profit than in a casino.

(2) Technical traders and fund manager can only claim they were not lucky only if they generate returns above the 1% significance level. In the case of SPY, this means that they must be better than 99% of the rest of traders/fund managers to claim they have some kind of an edge. Please note that this does not mean that a manager who generates a consistent return of about 4% each year, for example, is lucky but only that she cannot claim that she has an edge. It is known that many high profile academicians do not understand this difference and equate buy and hold under-performers with the lucky ones. This is because they do not understand the notion of edge, time dependency of returns and their probabilities.

Disclosure: no relevant position at the time of this post and no plans to initiate any positions within the next 72 hours..

Charts created with AmiBroker – advanced charting and technical analysis software. http://www.amibroker.com/

Related posts

https://www.priceactionlab.com/Blog/2013/05/random-trading-versus-trading-randomly/

https://www.priceactionlab.com/Blog/2012/06/fooled-by-randomness-through-selection-bias/

https://www.priceactionlab.com/Blog/2013/04/eliminating-selection-and-data-mining-bias-from-trading-systems-development/