Trading short volatility via VIX-related ETFs is very popular nowadays but involves extreme tail risk.

Many strategies to trade short volatility via ETFs are optimized so that tail risk in past data is avoided but risk of ruin has high probability in forward trading.

Below is a chart that shows 1-day and 5-day positive returns of VIX since inception.

It may be seen that 1-day returns in excess of 30% have been very common and that the 5-day return exceeded 200% in August 2015. By the way, 2015 was the year that the customers of many volatility trading signal providers experienced devastating losses. However, although some stopped providing signals there is now resurgence in the number of offerings by some who think they have a better mousetrap.

We have been asked repeatedly to provide volatility trading signals but we have declined because the above chart shows that tail risk is extreme and ruin is certain. Obviously we have lost business because of that but we have protected our reputation.

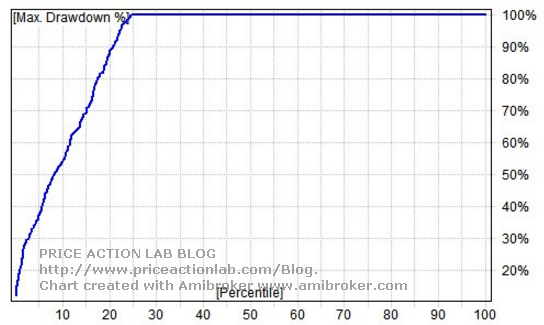

Below are results of a Monte Carlo simulation of the plain vanilla long-only strategy that switches between XIV and VXX depending on the value of ratio of VIX to VXV moving below or above 1. The results show that there is 75% probability of 100% loss.

Shorting volatility via inverse ETFs such as XIV or ZIV is extreme speculative trading. Although some inexperienced trading system developers think they have found the Holy Grail of trading, there will be disappointed in the future as the analysis shows.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting program: Amibroker

Copyright notice: Any unauthorized copy, reproduction, distribution, publication, display, modification, or transmission of any part of this report is strictly prohibited without prior written permission.