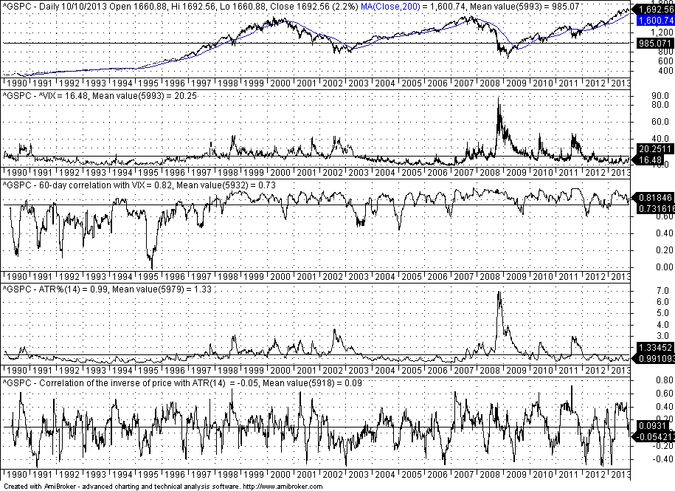

I have argued in the past that VIX, for all practical purposes, tracks the inverse S&P 500 index. Actually, there are much better technical indicators of volatility, like for example the Average True Range (ATR) measure. It is shown here that VIX has maintained a very high correlation with the inverse of the price of S&P 500 index since the late 1990s. This high correlation is not present in the case of ATR(14).

On the above S&P 500 daily chart, the first indicator pane plots the value of VIX. The second pane shows the 60-day rolling correlation of the close of S&P 500 index with VIX. It is clear that the correlation has remained at high levels after the late 1990s and the average value since the 01/1990 is 0.73. Current value of the correlation is +0.83.

The ATR(14) on the other hand when expressed as a percentage of the closing price, shown on the third pane, has an average value of 1.33% for the chart period and an average correlation with the inverse of closing prices of S&P 500 index 0f +0.09, i.e. basically no correlation. Therefore, this indicator is a better measure of volatility because it is not correlated with price but reflects how price changes affect volatility. For example, the market can surge on a particular day, as it did yesterday, and volatility will increase, as shown by the rising ATR(14) value. On the other hand, the value of VIX dropped a whopping -16% yesterday by virtue of tracking the inverse of price. One might as well look at the inverse of price and forget about VIX.

Related posts

https://www.priceactionlab.com/Blog/2012/08/on-the-zero-predictive-capacity-of-vix/

https://www.priceactionlab.com/Blog/2012/08/a-new-paradigm-for-equity-investment-risk/

https://www.priceactionlab.com/Blog/2012/08/further-analytical-evidence-that-vix-just-tracks-the-inverse-of-price/

https://www.priceactionlab.com/Blog/2012/09/the-vix-illusion/

Disclosure: no relevant positions.

Charting program: Amibroker

Disclaimer