In the last 20 years the best time to buy stocks was during periods of high volatility that marked the lows of major bear markets. Yet, the timing of long entries of many investment models is based on low volatility, contrary to what the charts indicate. This may be due to a lack of a clear relationship between volatility and risk.

As I have already written in another post regarding VIX, stock market volatility is inversely proportional to price and as prices rise, volatility falls and vice versa. This is an inherently unstable positive feedback system that can lead to irrational exuberance in the sense that investors perceive low volatility as low risk but in reality this low risk is associated with very high prices and low expected reward. Therefore, the relationship between risk and volatility is not often clear and some are using the wrong models. Volatility is associated with risk only when volatility represents risk. But it does not always. Often high volatility is associated with great opportunity. I am not interested in finding out why some in academia do not understand this. Actually, the academic community has a very poor record in dealing with the markets, even at a very basic and rudimentary level, mainly due to stubbornness in enforcing its simplistic models on them rather than trying to comprehend reality. Neither high volatility equates to high risk, nor low volatility equates to low risk at all times, necessarily. Only an empirical food would assert the opposite.

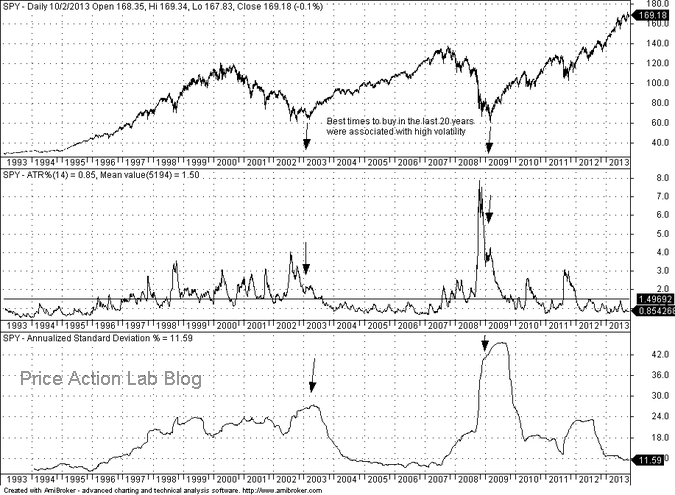

On the above SPY chart since inception of this ETF I have plotted two measures of volatility, an ATR(14) on the middle pane and the rolling annualized standard deviation of daily log returns on the bottom pane. It is clear that the best time to buy stocks for longer-term gains were at the two points indicated by the arrows on the chart that coincided with a low in prices after a substantial correction and bear market and that was also a time of high volatility. It is also clear that the 2008 bear market started with very low volatility. Thus, the relationship between volatility and risk is only temporal and is not related to longer-term expected gains or losses. Actually, the notion that high risk is often, but not necessarily, associated with high reward is confirmed from the above chart and this is the only notion of risk that investors should embrace. Anything else can be very misleading and may turn out to be costly.

Disclosure: no relevant positions

Charting program: Amibroker

Disclaimer