We use a popular trading strategy and one of its variants to demonstrate the high risks of volatility trading.

Most of the hype in financial media about volatility trading and strategies with extraordinary returns is based on gross underestimation of the risks involved by individuals with little or no skin-in-the-game. There are also those who unfortunately know the risks but try to conceal them.

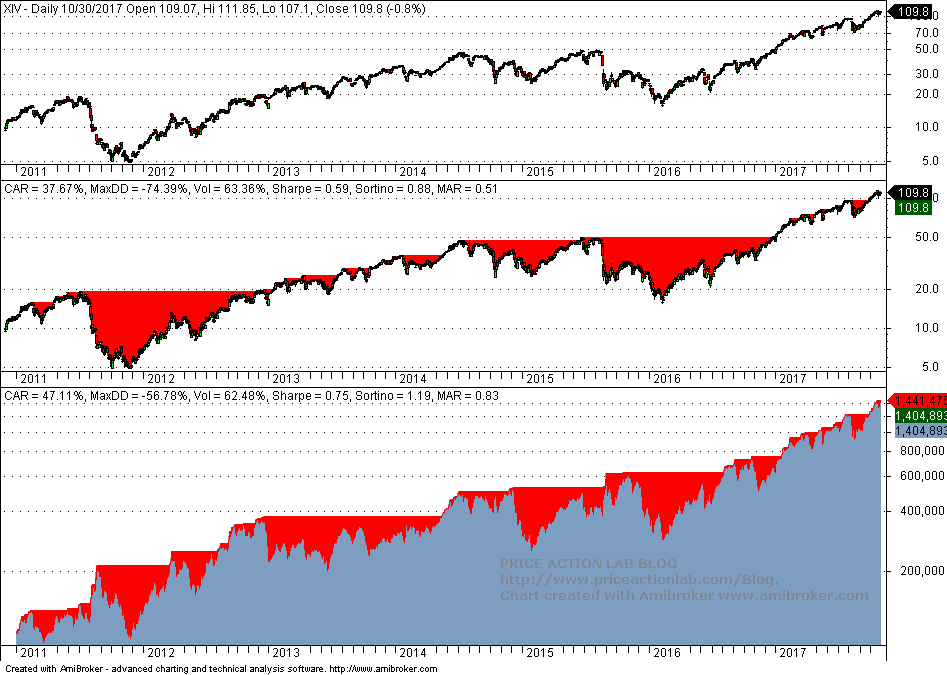

The majority of volatility trading strategies exploit contango and backwardation in VIX futures. A very popular strategy sells VXX and buys XIV when there is contango and then sells XIV and buys VXX when there is backwardation.

Below is a backtest of this strategy since 2011 with fully invested equity and $0.01 per share commission:

Notice the spectacular 47.11% CAGR. This high return is used to impress speculators. However, MAR (CAGR/Max. DD) is below 1. This is already an indication that something is fundamentally wrong with this strategy. This is because MAR below 1 when CAGR is very high means that maximum drawdown is even higher. But most of those who advertise the high returns of volatility strategies rarely report MAR. Actually, some of them do not even understand what that parameter means.

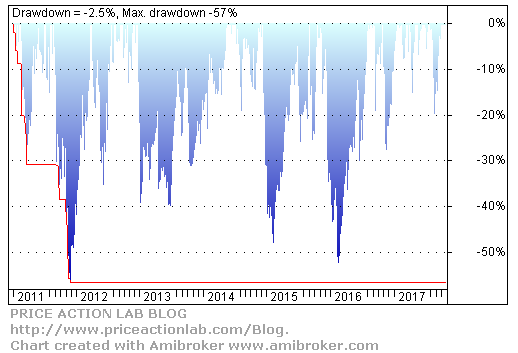

More importantly, when I looked at some sites selling volatility strategies or their signals I could rarely find a drawdown profile chart. Here it is for the above strategy:

This is a horrible drawdown profile. While year-to-date the maximum drawdown is about 25%, the maximum since 2001 was 57% and the minimum 32%. Maximum drawdown was nearly 20% in 2012, 2014 and 2015.

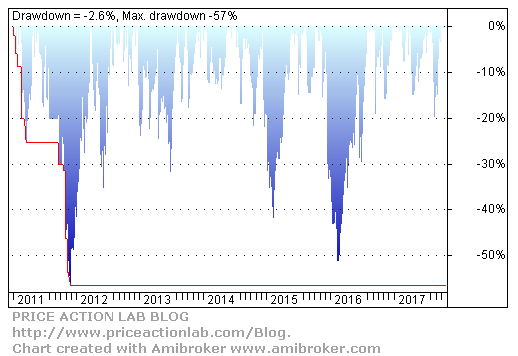

Some try to reduce risk and drawdown by introducing filters and modifying the basic strategy. Yesterday, someone in Twitter proposed buying XIV when the ratio of VXV to VIX is greater than 1.05. However, the drawdown profile of this strategy is as bad, as shown below:

These strategies are very risky and can cause uncle point and ruin. Most of those who are promoting them are either young quants with no or very little skin-in the-game, or reckless speculators. Volatility can spike suddenly causing very large losses.

If you have any questions, you can email us at: premium@priceactionlab.com

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting program: Amibroker

Copyright notice: Any unauthorized copy, reproduction, distribution, publication, display, modification, or transmission of any part of this report is strictly prohibited without prior written permission.