Many articles, papers, and books have been written about trading strategies and portfolio allocations with analysis and backtests based on non-tradable indexes. In many cases, the conclusions are mere illusions caused by non-tradability.

Since short volatility strategies are so popular nowadays, I will start with an example from the volatility landscape.

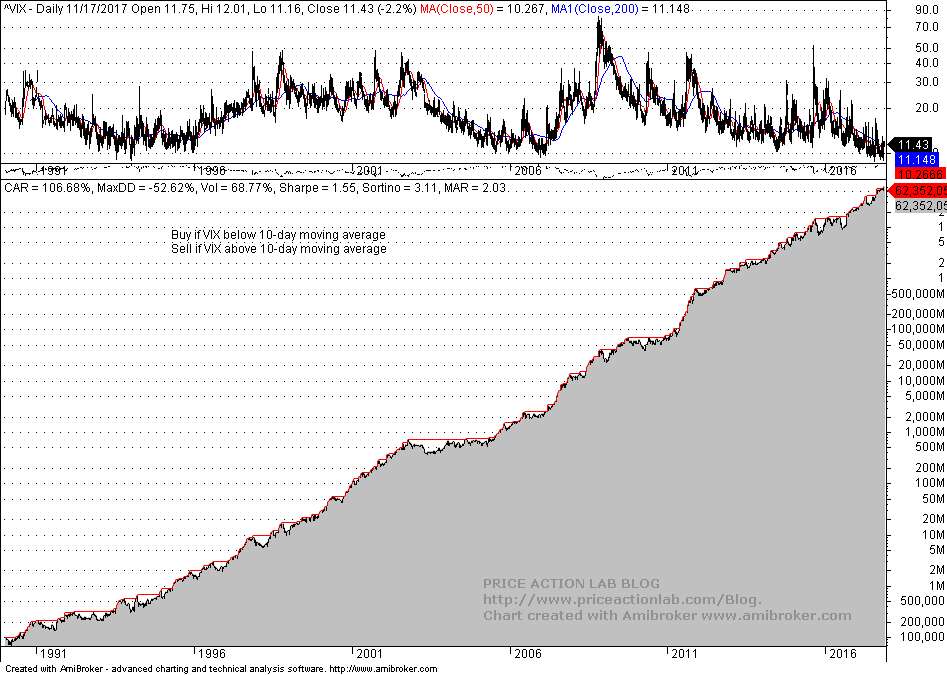

Consider the non-tradable VIX index used along with its term structure as the basis for designing volatility trading strategies. Below is a backtest of a simple strategy that buys VIX at the next open if it falls below its 10-day moving average and sells the position at the next open if it breaks above the 10-day moving average. I have included a commission of $0.01 per hypothetical VIX share. Starting capital is $100K and equity is fully invested.

Holy Cow! Since VIX’s inception CAGR is 106.68%, Sharpe is 1.55 and MAR is 2.03. By the way, who cares about the 52.62% drawdown?

No, this is not how Bezos or Gates became the richest men in the world. This index cannot be traded. But there are products based on this index developed in the last 10 years. In fact, since 2011 CAGR of the above non-tradable strategy is even higher at 168%. Yes, one hundred sixty-eight percent annualized return.

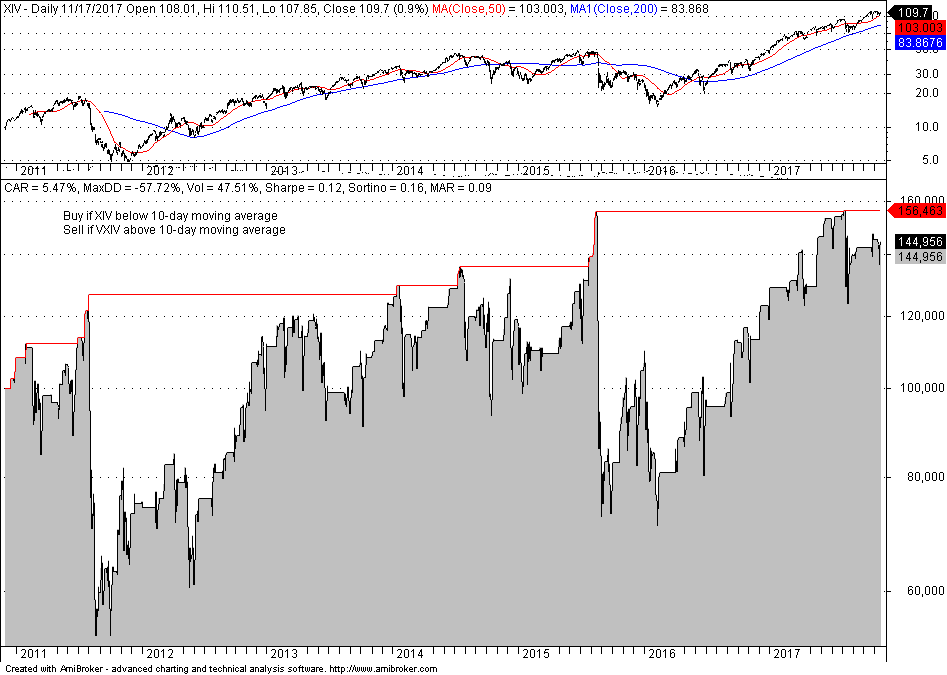

Two of the products are the popular XIV and VXX. The former tracks the inverse performance of the VIX Short-Term Futures index and the latter is supposed to track its performance.

Below is a chart that shows how the strategy that has generated the extraordinary returns in the VIX index has performed in XIV since its inception:

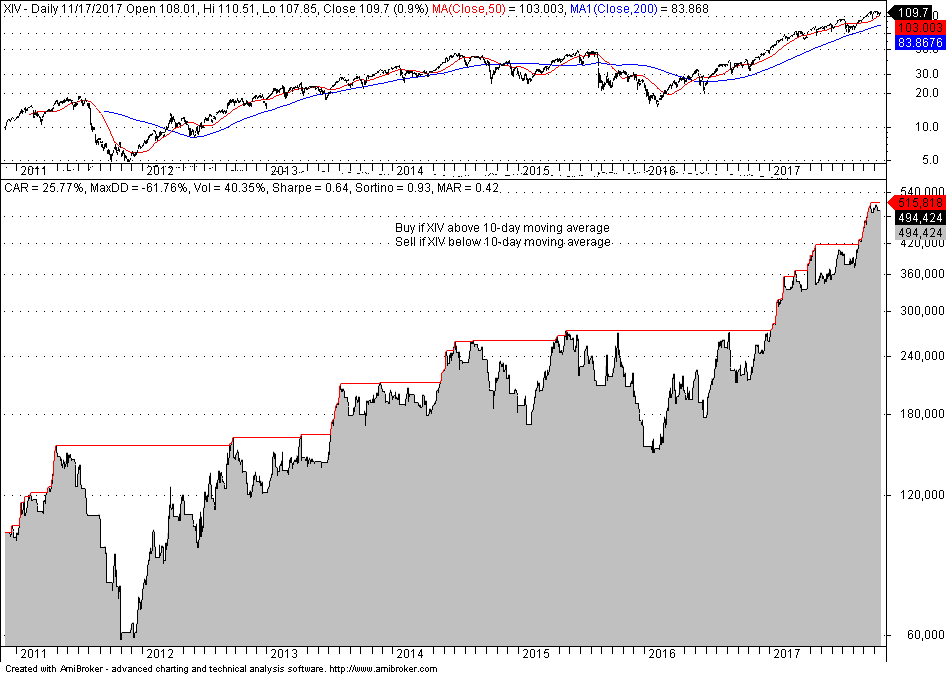

The results are disappointing. CAGR is only 5.74% and MAR is only 0.09. But maybe since XIV is an inverse ETF we should invert the strategy. This is done below:

The results are better than expected with CAGR at 25.77% but 61.75% drawdown. But nothing close to the VIX results with CAGR close to 170% in this period.

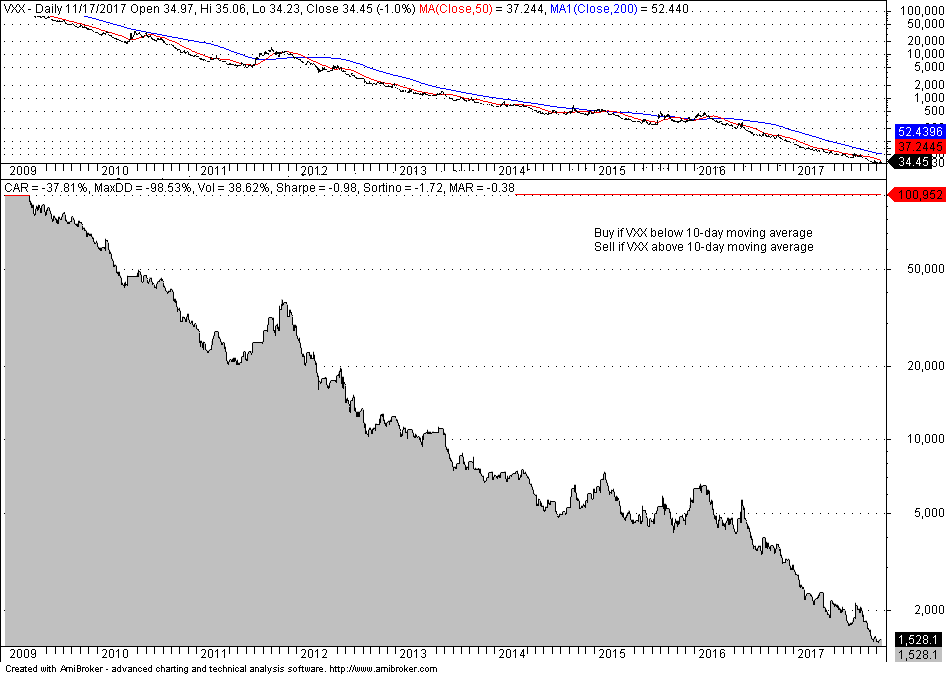

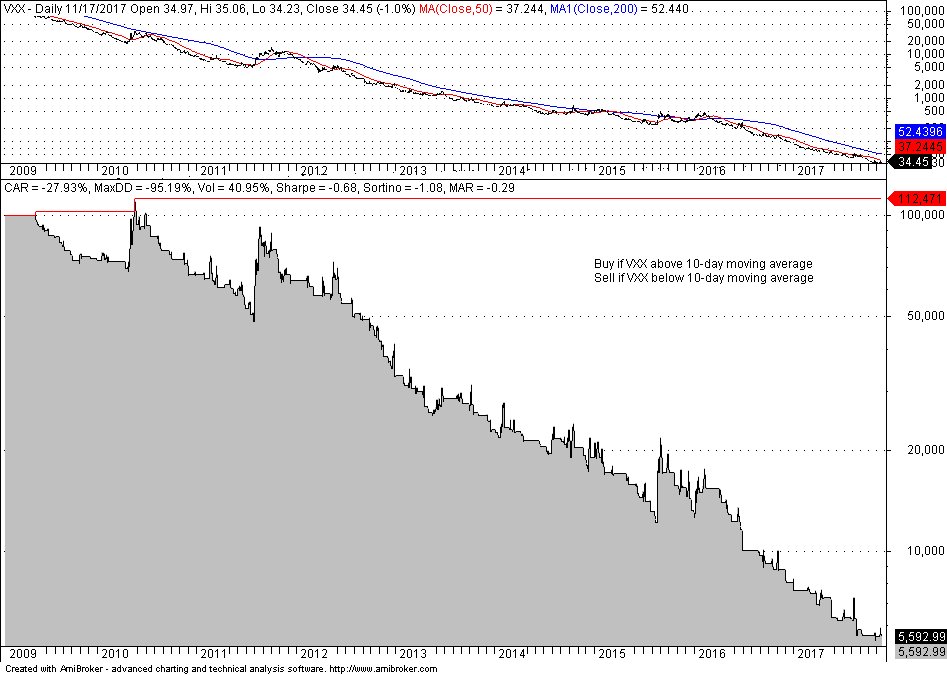

One would expect the original mean-reversion strategy based on the 10-day moving average to work well in VXX since this ETF tracks the short-term futures index. Below are the results of applying the strategy to VXX data since inception.

This is a disaster. Now one starts getting the idea that becoming a Bezos without AMZN or a Gates without MSFT will not be as easy as initially thought.

Well, what about if we reverse the original strategy in VXX. This is the result.

No luck here. Any way you try ruin will be inevitable. These are smart products designed to transfer wealth from naive users to product managers. Of course, one could over-fit some strategy to historical data and think this is the ticket to riches but reality will be merciless.

So the question remains: why the extraordinary performance in the VIX index and the miserable or catastrophic performance in the VIX products?

The answer has several levels.

The first level is that tradable securities do not always preserve all the characteristics of their underline indexes. I have included another simple example of a strategy in an article with a large divergence between S&P 500 and SPY ETF performance.

The second level is that indexes are designed to lure traders and products are designed to profit from them

The third level has to do with volatility drag, rebalancing, and other technical details that are beyond the scope of a brief article.

Backtests based on non-tradable indexes are as naive as they can get. Some have even used in backtests synthetic data of the S&P 500 going back hundreds of years. The results should be dismissed based on absurdity. Usually, authors with no skin-in-the-game do not realize the impact actual trades have and think of the market as abstract passive entities. However, markets are dynamic and paths depend on participation. Deterministic thinking is very dangerous. Markets are adaptive, highly non-linear stochastic processes. Have you taken this into account in your recent backtests?

If you have any questions or comments, happy to connect on Twitter: @mikeharrisNY

Charting and backtesting program: Amibroker

Technical and quantitative analysis of Dow-30 stocks and 30 popular ETFs is included in our Weekly Premium Report. Market signals for longer-term traders are offered by our premium Market Signals service. Mean-reversion signals for short-term SPY traders are provided in our Mean Reversion report.