Random long trades have generated a mean return of about 4.7% year-to-date in SPY ETF with close to 95% of these random traders showing a profit and in UPRO ETF, a mean return of about 22% with more than 94% of random traders showing a profit. This is the most generous casino possible at a very low market volatility.

Based on risk-adjusted retruns, the best opportunities are not in cryptocurrencies but still in the stock market. Cryptocurrencies offer high potential but at exorbitant levels of volatility of about 100% or even more in terms of annualized standard deviation of daily returns. On the other hand, volatility in the stock market has been at low levels with annualized standard deviation is SPY at about 6.9%.

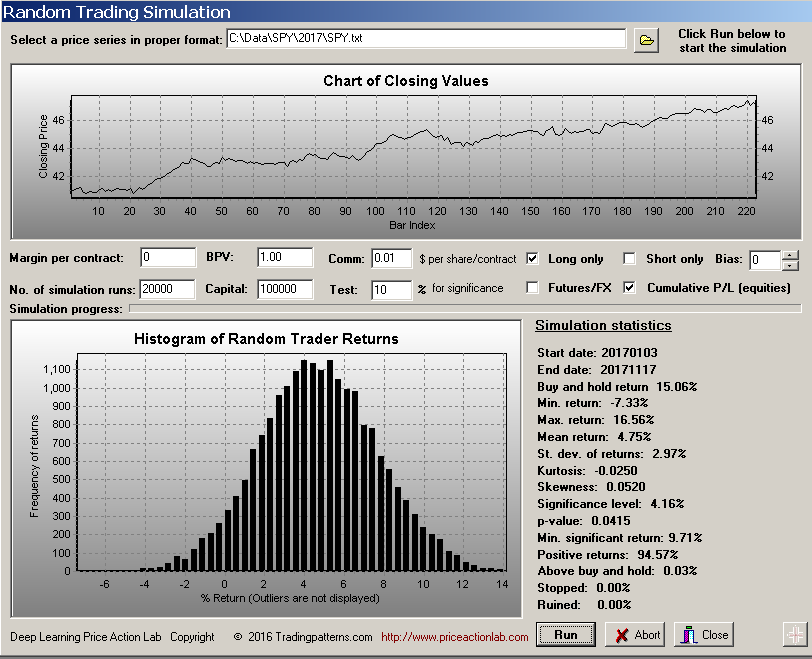

Below is a simulation of 20,000 random traders who use a fair coin to generate long positions near market close. The traders buy SPY at the close if heads show up and exit an open long position at the close if tails show up. The traders start with $100K capital and fully invest it. Profits are reinvested and commission is $0.01 per share.

Based on the distribution of net returns of the random traders we conclude that the mean return is 4.75% at a standard deviation of about 3%, kurtosis is slightly negative and skeweness is positive. About 95% of the random traders profited but only o.03% made more than 15.06%, the buy and hold return.

The high mean return shows that this random process is biased towards winning. A 10% test return is significant with a p-value equal to 0.0415. This mean that given that the null hypothesis is true and returns are random, the probability that some arbitrary strategy generates at least 9.71% total return (minimum significant return) is as extreme as the p-value. However, as it may be seen, only 0.03% of the random traders managed to full the significance test.

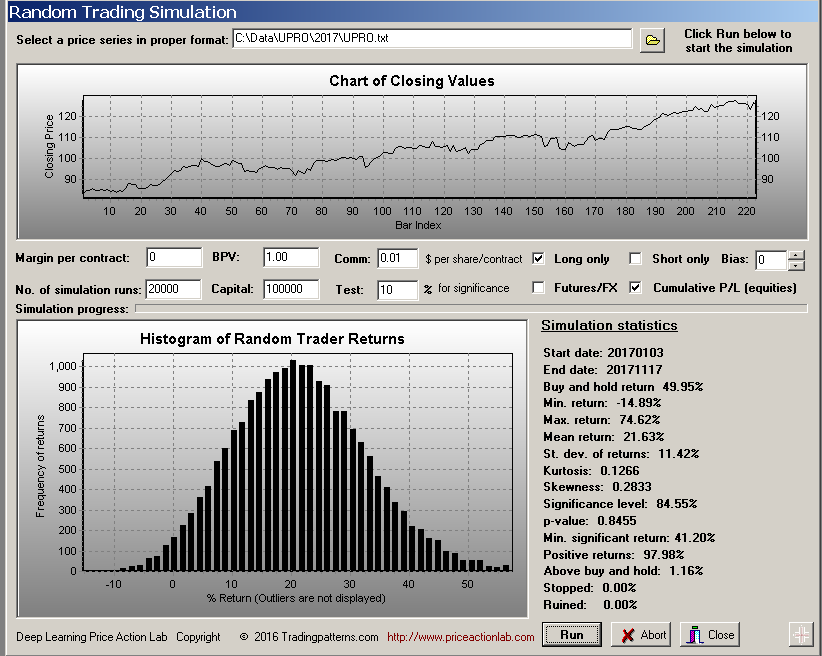

Below is the same simulation repeated with UPRO, a leveraged ETF that tracks S&P 500 total return.

In this case the mean return of the 20,000 random traders is 21.63% and nearly 98% show a profit. More traders, close to 1.2%, manage to make more than then buy and hold of about 50%. Therefore, the combination of high leverage and low volatility offers profit opportunities at relatively low risk levels.

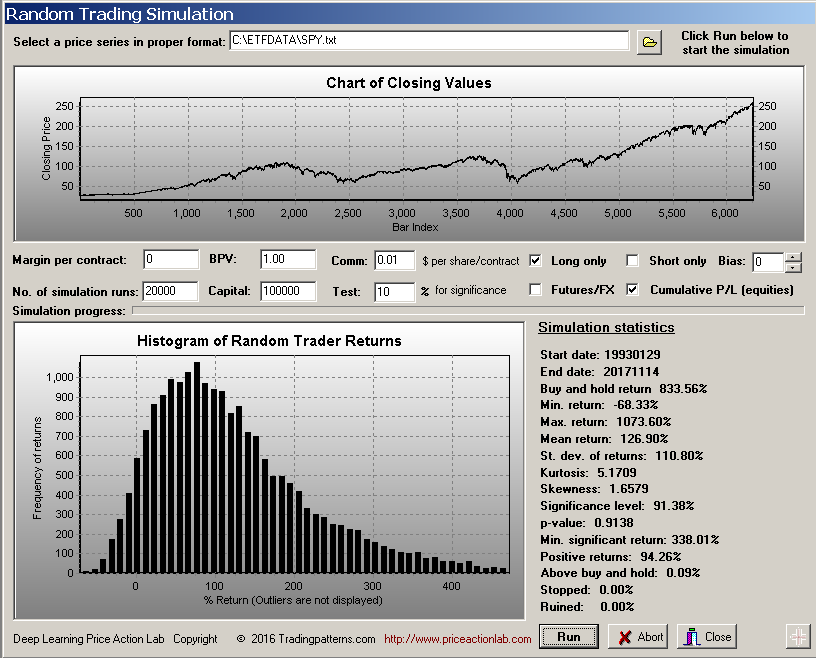

Given the above results, it may be seen that the stock markets has remained the most generous casino for random traders also in 2017. This has been true since SPY inception at least. Below is a simulation that illustrates this.

Since inception, mean return is about 127% versus 834% for buy and hold. More than 94% of random long-only traders have made profits. This is the most generous casino around. I wonder why traders waste time with other markets that pose high risks.

Where do the profits of the random long-only traders come from? They come from passive investors that reinforce the trend, dividend drift and worse-than-random-traders. Actually, there are many traders that are worse than coin toss traders. But this is another topic for another article.

If you found this article interesting, I invite you follow this blog via any of these methods: RSS or Email, or follow us on Twitter

If you have any questions or comments, happy to connect on Twitter: @mikeharrisNY

Charting and backtesting program: Amibroker

Technical and quantitative analysis of Dow-30 stocks and 30 popular ETFs is included in our Weekly Premium Report. Market signals for longer-term traders are offered by our premium Market Signals service. Mean-reversion signals for short-term SPY traders are provided in our Mean Reversion report.