There are various strategies for equity long/short and some may be more suitable than others depending on market conditions but there are always trade-offs.

On March 5, 2020, when we started our equity long/short daily signal service for S&P 500 stocks that is based on DLPAL LS features, we decided to use a strategy that opens positions at the open of the day and exits at the close of same day. In this way, there would be no positions left open overnight and the risk of a surprise move in a stock would be lower.

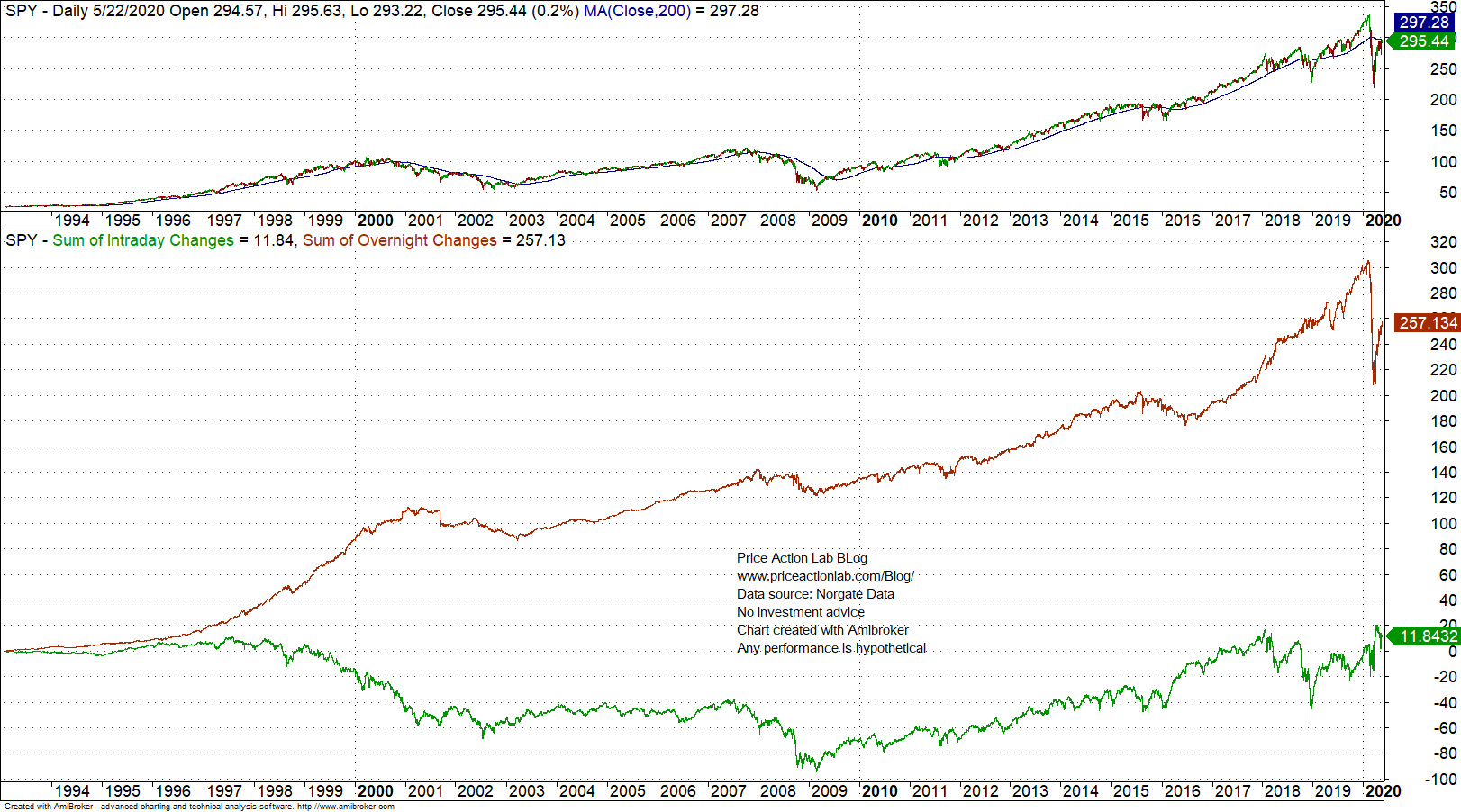

The open-to-close strategy (OC) poses challenges because historically most of the gains in S&P 500 have come from overnight (ON) changes; it is hard to extract consistently profits from regular trading hours (RTH), especially using a long/short strategy. However, during periods of high volatility, the ON-RTH relationship usually reverses and we have seen this occurring recently. The SPY ETF chart below illustrates this change.

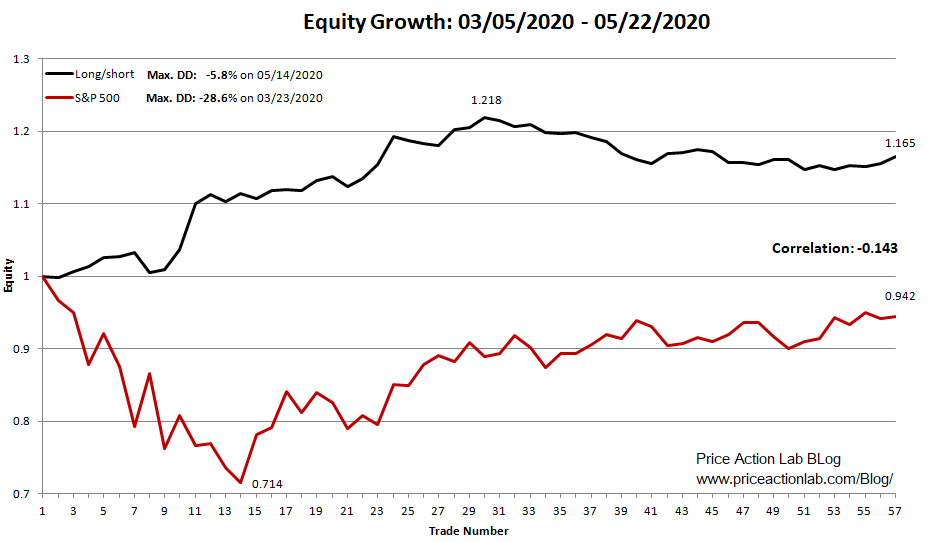

It may be seen that as soon as the market correction began, ON accumulation dropped and RTH accumulation rose. This regime change allowed us to use the OC long/short strategy and below is the performance from 03/05/2020 to 05/22/2020.

Simulated performance shows 16.5% return at 5.8% maximum drawdown vs. 5.6% loss in the same period at 28.6% maximum drawdown for the S&P 500.

The OC strategy worked well since March 5, 2020, but if volatility drops and there is again a switch to the regular ON-RTH relationship, then it may become unprofitable. In case that occurs, we will use the S&P 100 group and consider two other strategies as follows:

OCF: Open to close with bias filter takes long positions if the stock open higher and short if the stock open lower, enters at the open and exits at the close.

OR: Open Rank keeps positions open overnight and all entries and exits are at the open. This strategy is based on the same principles as the one used for weekly Market Signals reports with Dow 30 stocks.

What remains is to determine when to make the switch and this will depend mainly on volatility. We can always switch back to OC strategy if volatility increases.

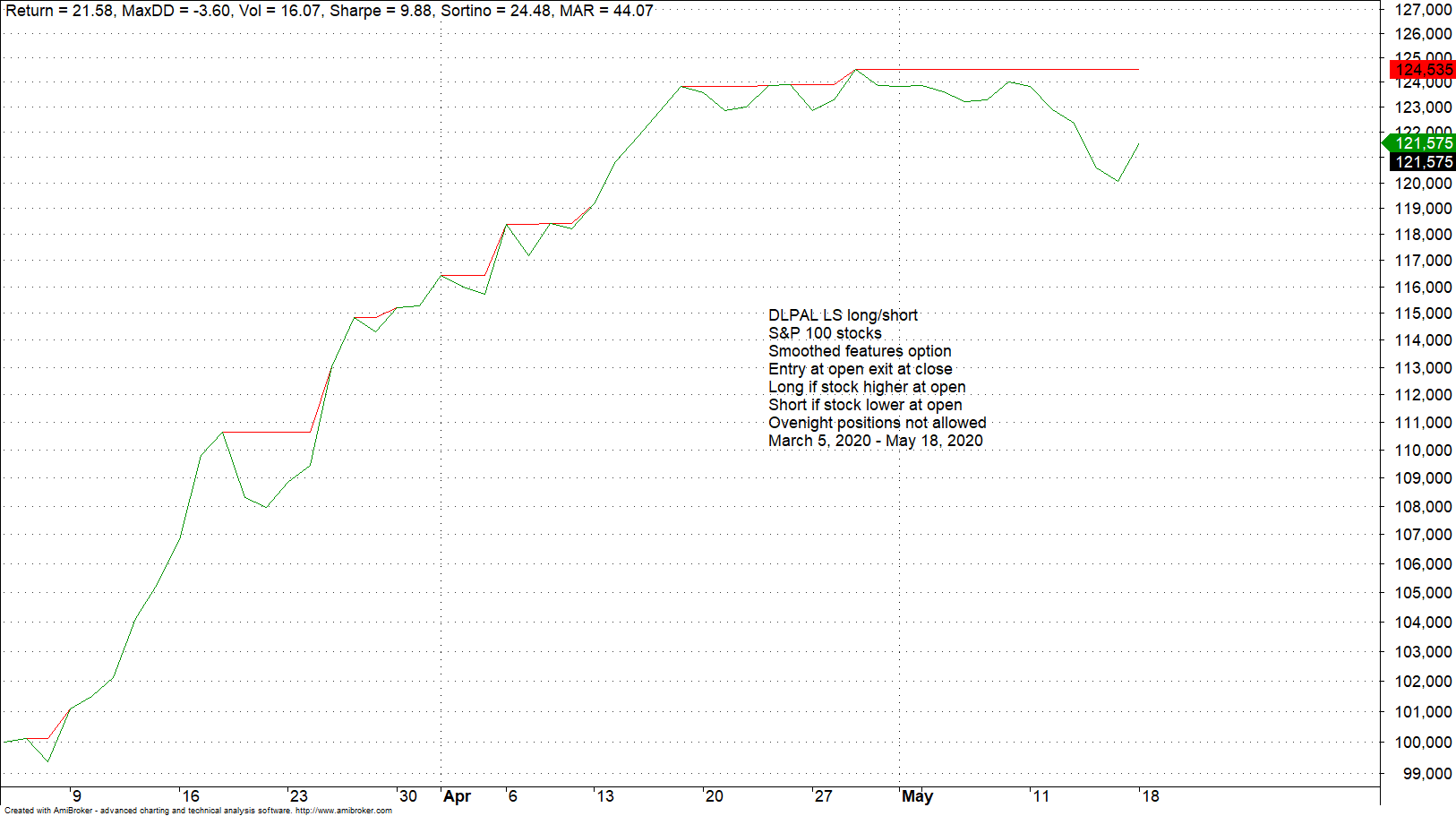

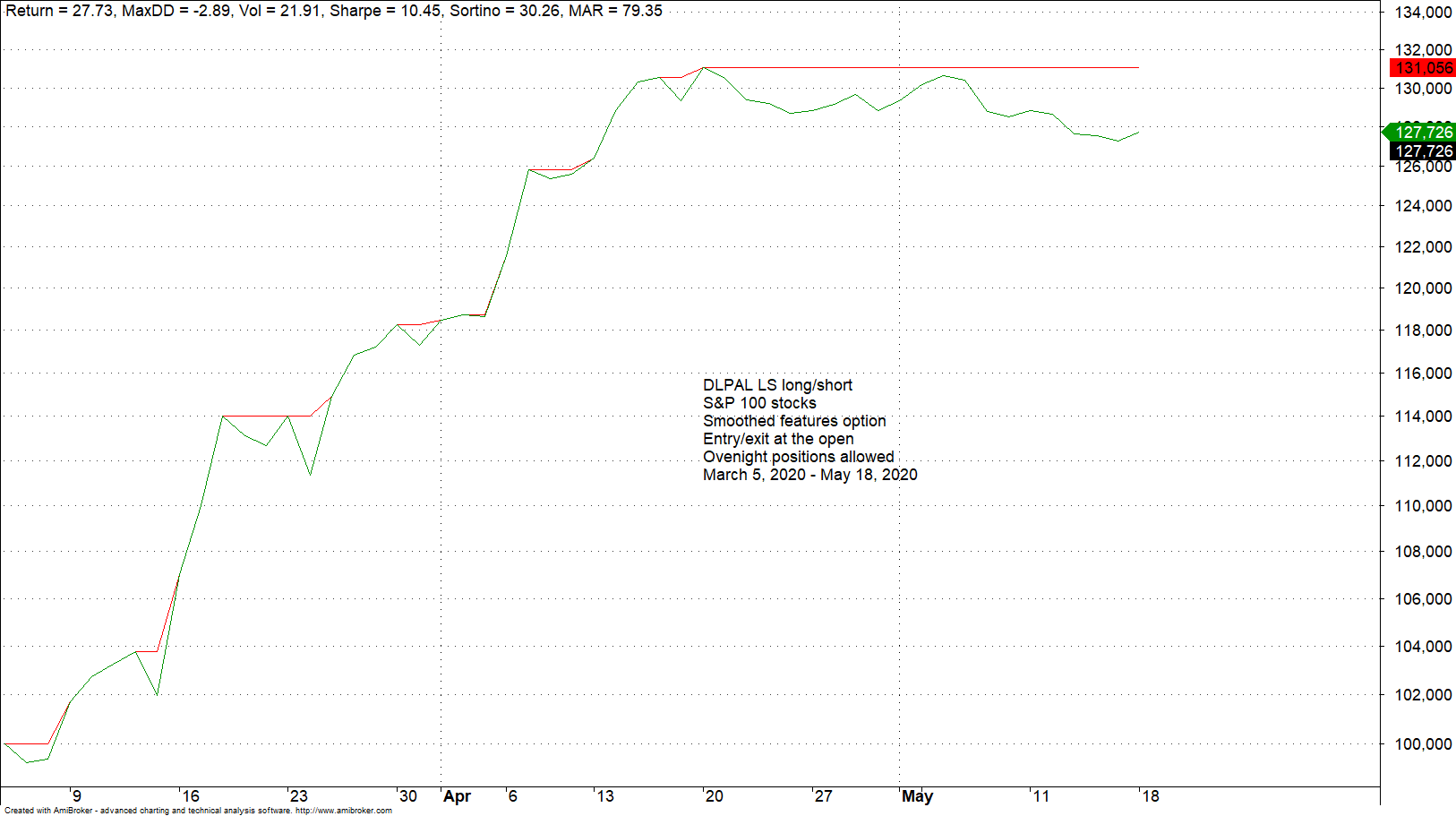

Below is how these strategies compare in simulations when using the S&P 100 group in the period 03/05/2020 to 05/18/2020. All strategies consider the top 5 stocks for long and the bottom 5 stocks for short. OC and OR always have 5 long and 5 short positions while OCF may have up to 5 for each side.

OC strategy. Return: 15.3%, max. DD -3.4%

OCF strategy. Return: 21.6%, max. DD -3.6%

OR strategy. Return: 27.7%, max. DD -2.9%

The strategy we selected, OC, has the lowest return but this was done to avoid overnight risk. OCF has higher return at no overnight risk but it has directional bias and we did not want that. The strategy may reject all short stocks, for example, and remain with 5 long, or vice versa. This worked well in the given period but it is not always the case as detailed simulations have shown.

The OR strategy offered the highest return but at much higher risk due to overnight open positions. Return was higher than OC by a factor of about 1.80.

There are many issues to consider when using a strategy or a variant of a strategy besides historical profitability and one of the most important is the price action regime and the risks present. A strategy for switching strategies, or a meta-strategy, may result in lower returns while minimizing risks significantly.

DLPAL LS offers a different way of developing trading strategies that does not rely on traditional indicators. This software is used by fund managers around the world to develop long-short but also directional strategies in a variety of markets.

More details about DLPAL LS can be found here. For more articles about DLPAL LS click here.

Strategy performance results are hypothetical. Please read the Disclaimer and Terms and Conditions.

Charting program: Amibroker