According to reports, the average forecast by Wall Street managers is for the S&P 500 to rise 10%. This is a naïve forecast.

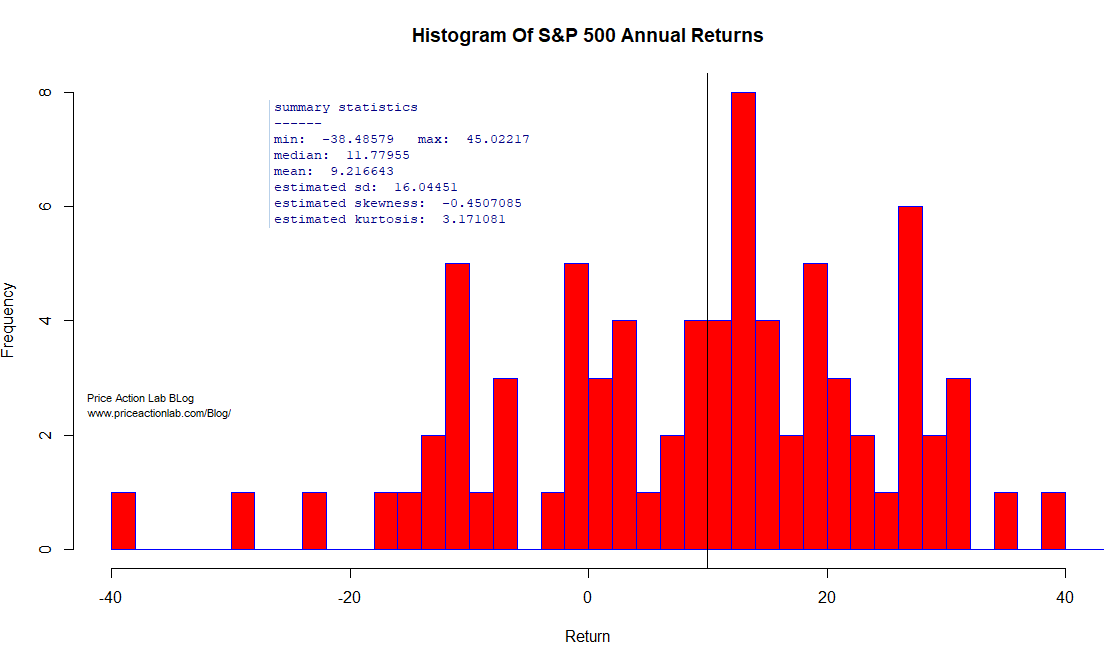

Below is the distribution of annual S&P 500 returns since 1941.

Based on the above sample, the mean annual return is 9.22%, and the standard deviation is 16%. The black vertical line is set at 10%. An empirical distribution fit does not provide any useful conclusion about the population distribution: the actual distribution can be anything, and there is simply not enough information to decide. The distribution may not even exist.

The Cullen and Frey graph shows that, based on bootstrapping (n = 5000), the values have high variability. The observed value does not indicate any particular distribution as a suitable candidate.

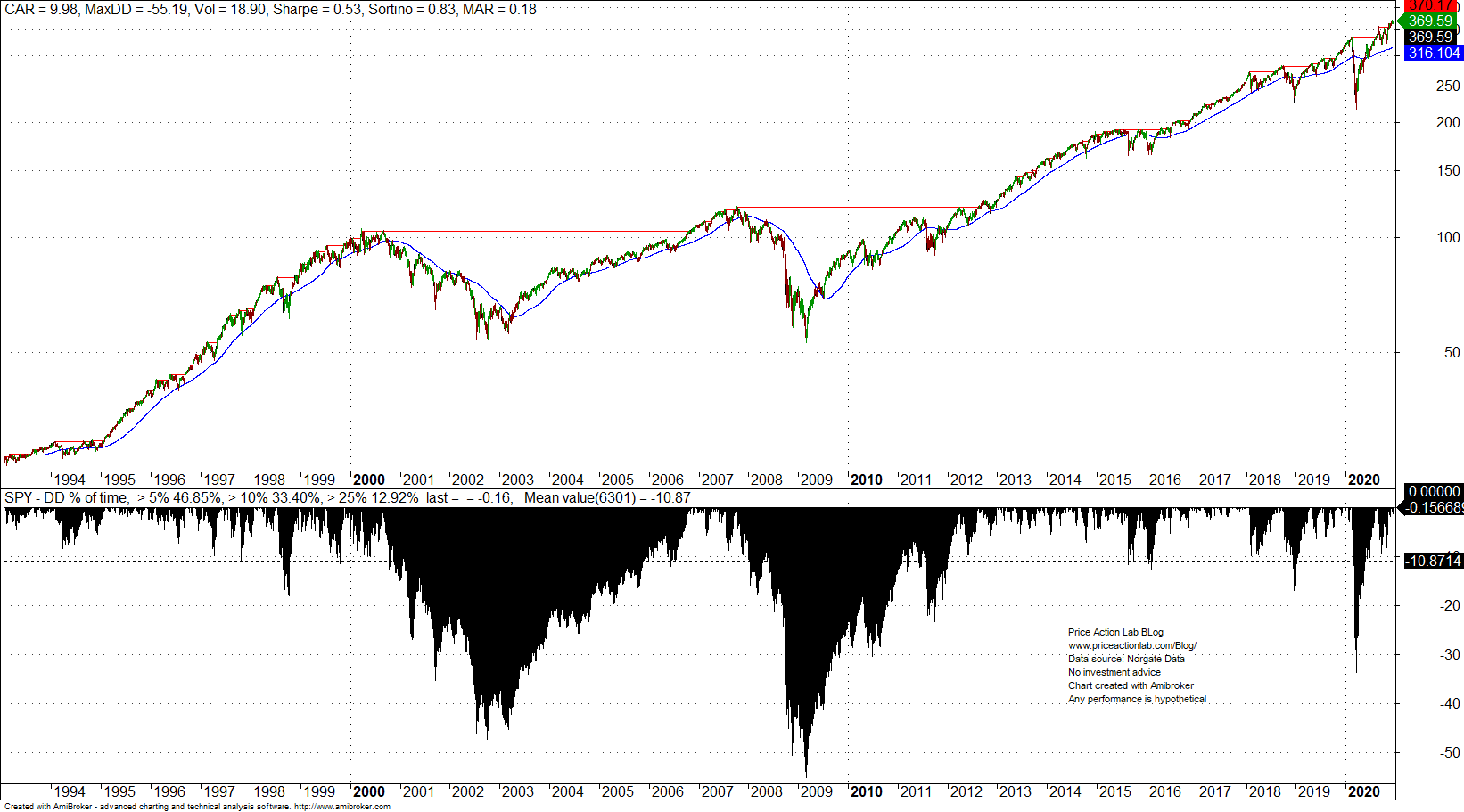

The above analysis offers one reason why (on average) forecasts are naïve. Note that the 10% gain average forecast is the same as the annualized total return of SPY ETF since inception, as shown below.

The point the above chart makes is that those who make forecasts about the market are naïve, and more so if they claim a naïve forecast that is the longer-term annualized return.

Since 1993, there have been two devastating bear markets and numerous large corrections. The naïve forecasters (usually salespeople or “do nothing managers” of the buy and hold type) assume the Fed will continue to support equities as in the past. The Fed also supported markets earlier this year, but a 30%+ drawdown occurred regardless.

The argument is usually that “stocks go up in the long term.” No mention is made of those close to retirement who had to wait 7 years after the dot com bear market to recover their losses. The managers who make naïve forecasts will not lose because, in case of a market crash, their marketing department hopes to attract fresh money by claiming that “stocks are cheap now.”

Investors, and more importantly, those close to retirement, could benefit from forecasts of potential market crashes, but those are hard to make. Even a charlatan can make a naïve forecast without adding real value. Highly paid managers making naïve forecasts is a contradiction; no one should be paid a dime for making a naïve forecast.

Charting and backtesting program: Amibroker Statistical analysis in R

Data provider: Norgate Data

If you found this article interesting, you may follow this blog via push notifications, RSS or Email, or on Twitter