The technology sector is at the edges of unprecedented tail risk after a rally of more than 150% in the last three years. With wishful thinking driving decisions of the investment community and portfolio managers, the odds of a large and prolonged decline have risen dramatically.

Although Wall Street is trying hard to paint a rosy picture about the state of the economy, anyone who takes the time to travel around and talk to people with skin-in-the-game of running a business knows the idea of a recovering economy is only in numbers and not in reality.

Jobless rate remains high despite complex schemes to conceal the actual state of employment. People are not willing to work long hours at present salary levels. At the same time, most companies cannot afford to raise salaries. The local small businesses are facing stiff competition from centralization: on the one hand, large tech companies push schemes for decentralizing payments but on the other hand they keep centralizing economic activity and pushing local small businesses out of the market.

Labor force participation rate has dropped from about 68% in the beginning of the century to less that 62%. More and more people depend on benefits from the output of a shrinking workforce or increase in public debt.

Then, there has been a steady increase in current account deficit, despite an expected decrease after tariffs imposed by previous administration. According to U.S. Bureau of Economic Analysis,

The current account deficit in the US widened to $195.7 billion or 3.6% of the GDP in the first quarter of 2021 from a downwardly revised $175.1 billion in the previous period and compared to forecasts of a $206.8 billion. It is the highest current account deficit since the first quarter of 2007, due to an increased deficit on goods and a reduced surplus on primary income.

Soon we may be looking at an annual current account deficit of nearly one trillion dollars. The current account deficit combined with a public debt of about $27 trillion due to the stress created by the pandemic has formed an explosive mix. At what point will investors consider current bond yields in the US are too low given the risks of prolonged recession coupled with some inflation? The risks for the stock market engine of the US stock market, which is the technology sector, are increasing fast.

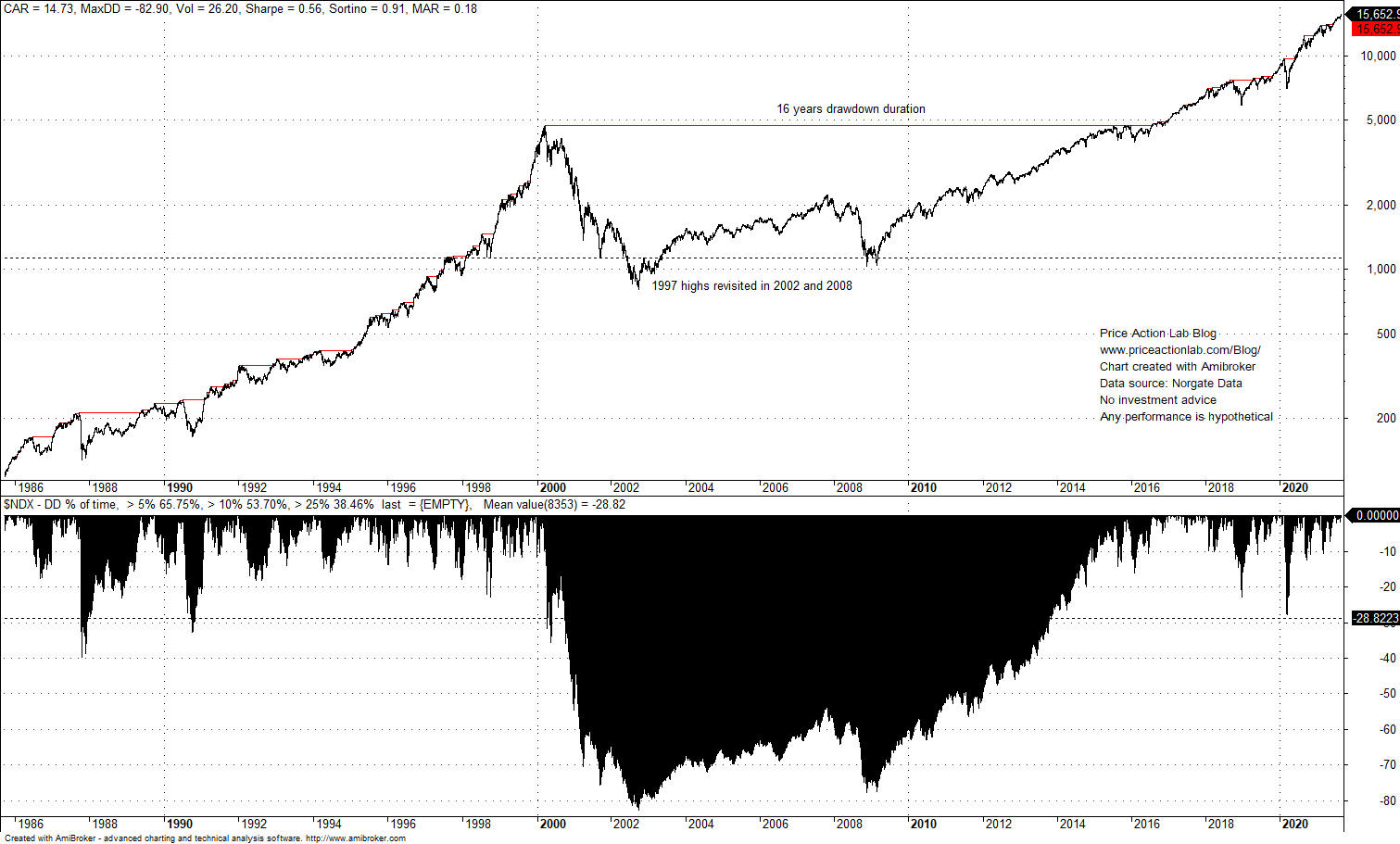

Even if we discount ominous signs from fundamentals, the tech market has been unforgiving to investors in the past while delivering long drawdown periods and revisiting past highs often, as may be seen from the NASDAQ-100 chart below.

After the dot com crash in 2000, it took the index 16 years to recover while maximum drawdown reached below -80%. More importantly, the index revisited 1997 highs in 2002 and 2008. This was not investment for late 90s uptrend participants but a horrible rollercoaster for nerves of steel. Some, if not many, never made it to the 2016 recovery.

The typical response is: “This time is different and the index constituents are strong companies.”

“Strong company” is a relative term. The few trillion dollar cap corporations that drive this index higher, and via coupling the broader market, are susceptible to large losses if the economy enters a recession. Given that a US recession will cause a cascade of recessions on a global scale, revenues from international operations will also be affected. The worst case scenario is a persistent strong US dollar that will also impact profit repatriation. The outlook at this point is not rosy at all despite efforts from portfolio managers acting on wishful thinking.

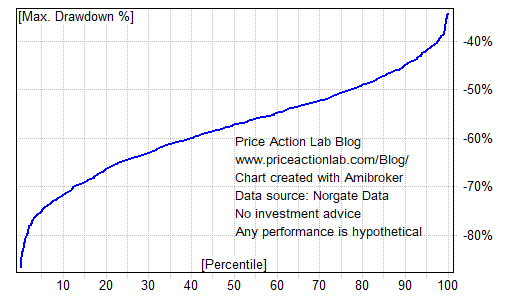

The problem with tail risk is that we can get a sense of it when it grows out of bounds, as in this case with the technology market, but timing of a bear market is impossible to estimate even closely. There is nothing in this article to suggest a timing signal. However, if we assume that “this time is different” is just wishful thinking, then with a Monte Carlo simulation based on past NASDAQ-100 performance we can (very) loosely estimate that the probability of a drawdown of more than 55% is about 50%. That’s close to fair coin toss.

Monte Carlo simulation results based on NASDAQ-100 buy and hold equity curve changes

In fact, investing in technology market at this point without tail risk hedging or some form of diversification (if that is possible) is a fair coin toss disaster but timing of the event is unknown. The plunge can start next week, next month, next year or after a few years. If the plunge occurs, a lot of people will lose a lot of money and depending on timing of their investment. Everyone should do their homework and consult a registered financial adviser for risk analysis. This article is about the author’s opinions only.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS or Email, or in Twitter.

Price Action Lab premium Content: By subscribing you have immediate access to hundreds of articles. Premium Insights subscribers have immediate access to more than a hundred articles, Premium Articles and Market Signals subscribers have immediate access to hundreds of articles that include the trader education section and All in One subscribers have access to all past premium content. Click here for more details.

Price Action Lab Blog Premium Content