Passive investing is 100% accurate because it follows price with no error. Anything other that passive investing requires “doing something” rather than “doing nothing.” Actions in markets require defining objectives.

If the forecast is for higher prices, then doing nothing is probably the best action. After all, most known strategies are designed to provide better risk-adjusted returns. For a cash portfolio with no uncle point risk, if the forecast is for higher prices, then going passive is probably an optimum path. Nowadays, this is also called hodling in the crypto space.

I have never seen an annual consensus forecast for lower prices in the stock market. Guess what then: according to these forecasts, “doing nothing” is the optimum path. In fact, most forecasts are of the “naïve” type: the expected return for next year is the average yearly return of the past.

Since 1942 with a total of 79 years, the S&P 500 was up in 58 years and down in 21 years. The average yearly return is 9.4%. Knowing nothing about the future, which sounds rational, the best estimate for next year is the average, or 9.4% plus or minus what your fancy statically analysis indicates.

Note however, there is a misconception. When naïve forecasters say the market will go up and the consensus is for 9% gain for example, what they are essentially saying is that this is the “do nothing” forecast, not that the market will actually gain 9% plus or minus an error depending on how fancy the statistical analysis gets. I wonder how many understand the difference although the crowd seems to get it and go passive as long as the forecast is for above inflation.

Watch out then for inflation rising above 9%. The crowds with maybe around 10 trillion in passive investments may get spooked but this is another story for maybe an article in those permabear sites. The subject of this article is when the “do nothing” forecast clashes with investor objectives. For example, the objective of an investor may be no more than 30% drawdown. In this case, a “do something” forecast is required and this opens the forecasting Pandora’s Box. This is because the difference between “doing nothing” and “doing something” in the markets is the difference between night and day.

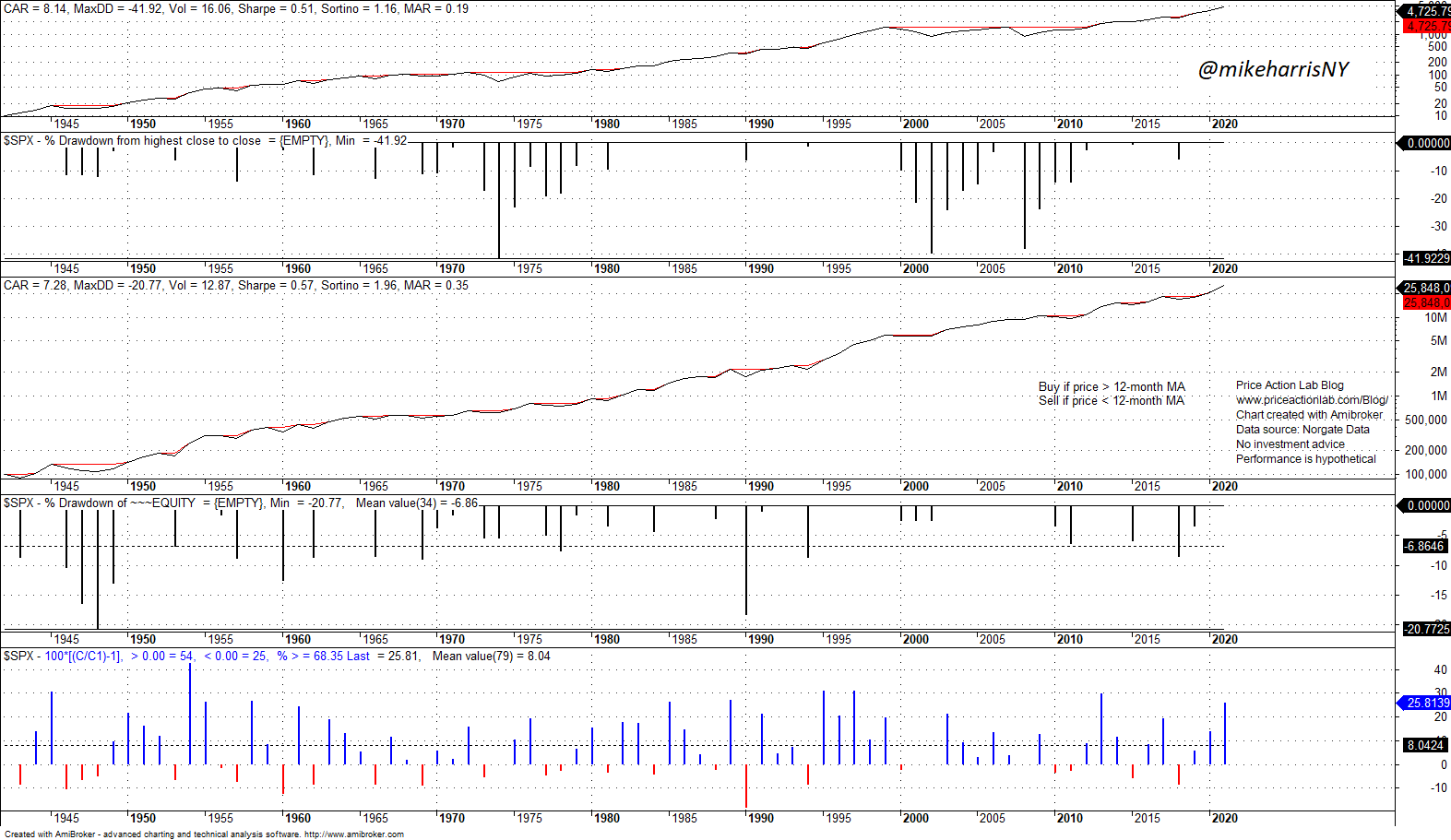

Below are the results of a “do something” forecast.

The objective of this forecasting method is to reduce equity drawdown and volatility. Obviously, there can be many different objectives but this is a popular one. The 12-month moving average cross is used to forecast turning points in the market with a dual purpose

- Follow uptrends as closely as possible.

- Avoid downtrends as much as possible.

This simple forecasting method based on price series momentum succeeds in reducing the maximum drawdown by about a half in monthly timeframe: from 42% for “do nothing” to 21% for “doing something.”

The top chart above shows monthly S&P 500 statistics since 1942. The next chart shows the yearly drawdown profile. The middle chart is the equity after applying the forecasting method. The fourth chart shows the drawdown profile of the equity and the last chart shows the yearly returns of the forecasting method.

The drawdown reduction comes at a price: lower annualized and average returns: 8.1% and 9.4% for buying and holding versus 7.3% and 8% for the strategy, respectively.

However, the objective has been achieved only historically. In fact, we don’t know if “doing something” along the lines of the above forecasting method will continue to work well in the future. For example, a prolonged sideways market for several years could render the forecasting method unprofitable.

For an investor without any leverage of the “do nothing” type, a loss of about 1% per annum may be substantial. But for an investor sensitive to volatility, the loss may be acceptable and “doing something” at the cost of lower total return is desirable.

Conclusion: “Do nothing” versus “do something” forecasting depends on objectives, risk aversion, risk management and on a host of other things. “Doing nothing” is a forecast of some sort while “doing something” requires a more sophisticated approach to forecasting. But at the end of the day, even passive investors are forecasters.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS or Email, or in Twitter.