Some market participants argue tail risk hedging of portfolios tracking the S&P 500 is not necessary because large losses on weekly or monthly timeframes are rare. They are both right and wrong: large losses are indeed rare but when they occur they can cause uncle point.

Tail risk hedging is expensive but cost can be minimized when executed by professionals who have the proper strategy. Cost of buying regularly out-of-the money puts without a proper strategy can add fast and cause wide underperformance in medium to long-term. In my opinion, in the case of individual investors with no skin-in-the-game of options and derivatives in general, any attempt to hedge tail risk could lead to escalating cost. This is a task for professionals and there is a wide range of derivatives they can use besides put options.

Important: Executing a tail risk hedge is as important as removing it. The impact on performance can be significant due to timing. A 3% allocation to put options may generate 1000% during a fast market correction but that may vanish due to volatility crush in a matter of days if the tail risk hedge is not removed. This is not an area for experimentation but of careful analysis and implementation.

Large weekly and monthly losses in S&P 500 have been rare but their probability is much higher than what is predicted by a normal distribution because of left fat tails. Below are some charts and statistics.

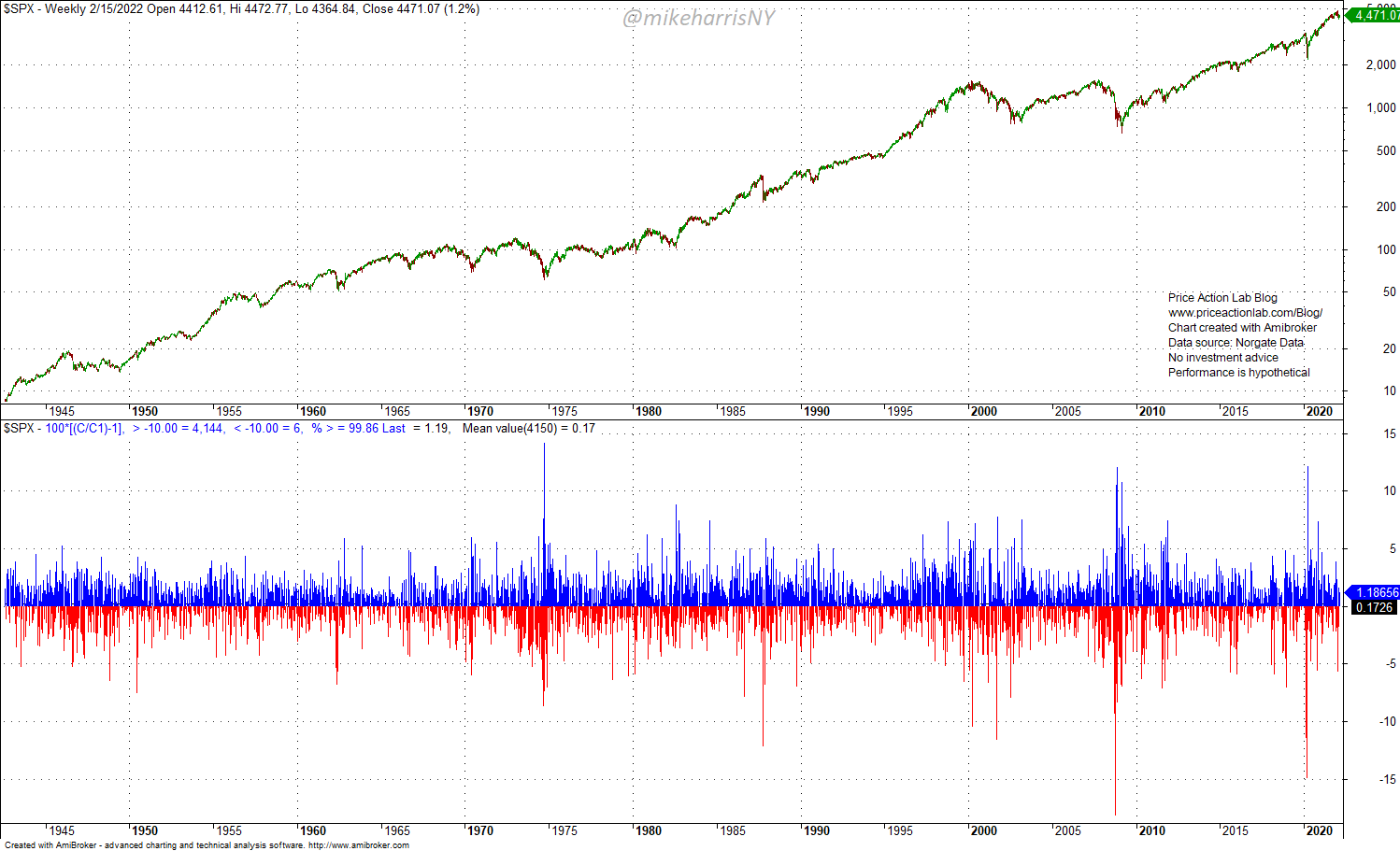

Weekly returns larger than 10%

The chart below shows weekly returns of S&P 500 starting in 1942.

There have been six weekly drops in S&P 500 larger than 10%, as indicated on the chart. However, we also have to look at maximum drops based on weekly lows. Those are summarized in the table below.

It may be seen that although the weekly return due to 1987 crash was -12.2%, the maximum drop was -23.43%. Similarly, in week ending October 10, 2008, the weekly return was -18.2% but the maximum drop was -23.6%. Note the recent back-to-back drops during the stock market crash of 2020. Not only large drops can occur but there may be clusters that could cause panic, redemptions, liquidations due to margin calls and in the best case, a long recovery time.

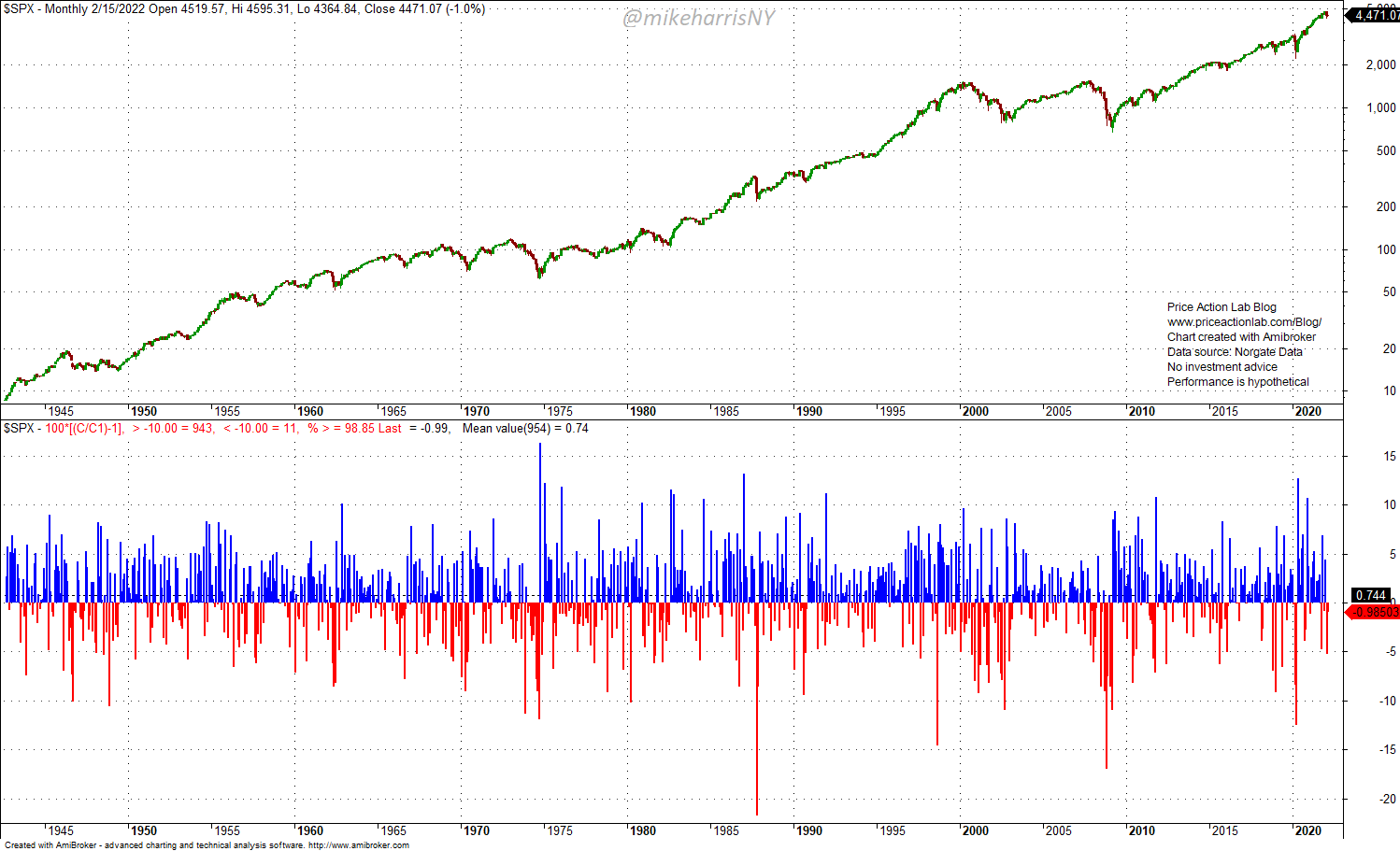

Monthly returns larger than 10%

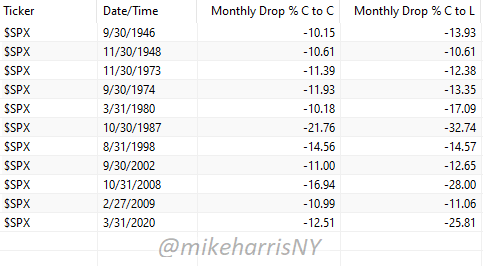

There have been 11 monthly drops in S&P 500 larger than 10%, as indicated on the chart. In this case also we have to look at maximum drops based on monthly lows. Those are summarized in the table below.

The most recent monthly drop in S&P 500 of more than 10% was in March 2020 at -12.5% from the close of the previous month but maximum drop was 25.8%. Any drop of more than 20% can cause uncle point and this is partly the reason diversification and/or tail risk hedging are required. Note that the large drop in March 2020 occurred despite Fed support in the form of asset purchases. If these programs are not active in the future, losses can be larger and recovery time may be in the order of several years.

In October 2008, the S&P 500 fell nearly 17% from the close of the previous month but maximum drop was -28%. Then the index fell again the following month additional 7.5%. We have no idea how many passive investors hit uncle point during the period, exited the market with a loss of about 23% and missed the bull market after 2009.

Large weekly and monthly drops in markets do occur and have higher probability than most investors think. Those not prepared for such events could face uncle point.

Premium Content 10% off for blog readers and Twitter followers with coupon NOW10

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS or Email, or in Twitter.