Where can we draw a line between hype and reality in managed futures? A few thoughts.

After a lost decade, from 2009 to 2018, managed futures trend-following delivered solid gains and the best performance since 2000 last year.

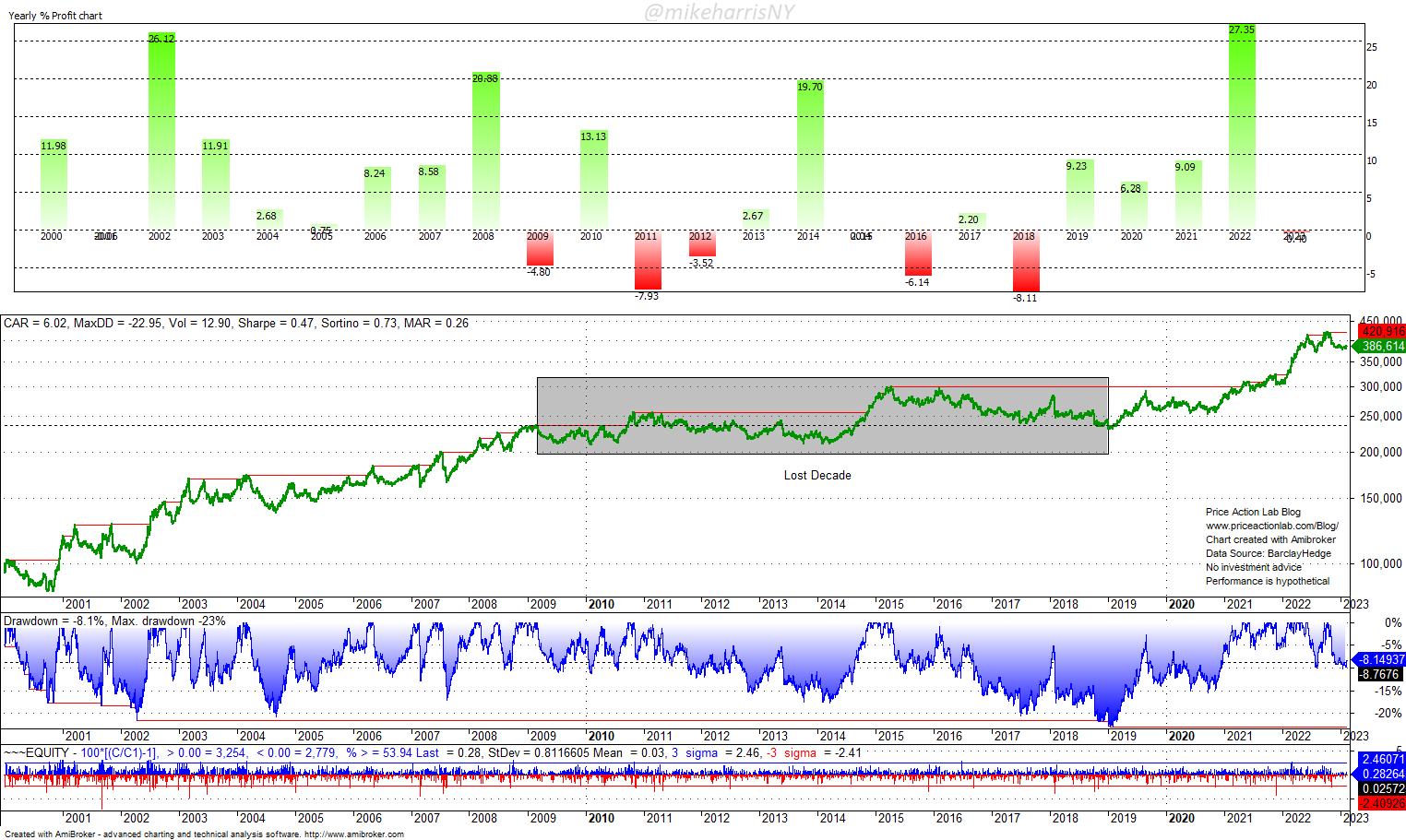

SG Trend Index Performance 01/03/2000 – 02/16/2023

The SG Trend Index ( Société Générale) had a 0.4% annualized return in the lost decade, at 21.8% maximum drawdown, or MAR of 0.02 and barely above 0.

Then, in the last four years, the annualized return jumped to 12.7% with a maximum drawdown of just 13% and MAR of nearly 1.

Last year, the trend-following CTAs included in the index returned 27.4% on average, which is the best annual performance since the index’s inception in January of 2000.

Naturally then, the industry rushed to capitalize on managed futures comeback after a lost decade, with offerings of ETFs and new funds. The financial media was flooded by articles and podcasts predicting a dynamic return of managed futures trend-following, focusing on the diversification and hedging potential.

How much of what has been said and done is due to reality and how much is due to hype?

Undoubtedly, managed futures trend-following plays an important role in portfolio allocation. One key question is whether the protection provided last year was random or due to structural convexity.

There may be several causes of CTA underperformance, but the main two are the financialization of commodities and growing competition at lower liquidity. CTAs were forced to diversify even more to deal with lower liquidity and some have increased exposure to equities to boost performance.

The pandemic and what followed, i.e., the increase in money circulation and the supply shock that drove inflation, were random events. During the lost decade, similar random events were absent. The trend-following systems failed to provide performance despite a constant search for “outlier” trades, and especially despite a growing exposure to rallying equities.

Although trends in commodities, rates, and forex usually last long, this is not the same as trends in equities, and the volatility is higher. Increasing exposure to equities may decrease the beta but at the cost of a lower or no alpha. In essence, by increasing exposure to equities and even targeting volatility, managed futures trend-followers become more of capital preservation programs than investments providing absolute alpha. However, this move is made for survival purposes in an industry with no barrier to entry that uses relatively simple strategies to search for “outliers”, which is a fancy word for large trade gains.

In my June 2021 article, I also wrote:

There is still a good probability that CTAs may provide some convexity in case of a bear market in equities and a small allocation may contribute to portfolio diversification. However, a failure to provide convexity may be viewed as a regime change for those programs.

As it happened, in 2022 trend-following CTAs had their best year since 2020 and provided solid convexity and protection to crashing equities. However, as I noted above, the outcome was due to random events, and similar conditions that benefit trends may not appear again for many years. Therefore, the next two years will serve as a critical test for the trend-following industry and the new products developed. It will be a tough challenge. I find trend-following an intriguing subject that poses many challenges, and I wish those CTAs and product developers best of luck going forward.

10% off all premium content with Discount Code NOW10

By subscribing you have immediate access to hundreds of articles. Premium Insights subscribers have immediate access to more than a hundred articles and All in One subscribers have access to all premium articles, books, premium insights, and market signals content.

Free Book

Subscribe for free notifications of new posts and updates from the Price Action Lab Blog and receive a PDF of the book “Profitability and Systematic Trading” (Wiley, 2008) free of charge.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS, Email, or Twitter.