The difference between the old alchemists and the modern financial alchemists is that the actions of the latter group endanger the stability of an already fragile financial system.

Options contracts are derivatives instruments. The VIX index futures contracts are derivative instruments based on options contracts. In turn, volatility ETNs, such as XIV and ZIV, are derivative instruments that offer exposure to VIX futures contracts, essentially these ETNs are:

derivatives of derivatives of derivatives

or called D^3 derivatives in this article.

Alchemists of the past, among other things, aimed at transmuting base metals, such as lead, to gold and in this way creating wealth. That was an exercise in futility that impacted only the fate of the individuals involved and did not pose any significant risks to the financial systems of that time.

Modern alchemists are finance professionals that build derivatives on top of derivatives to create wealth for their firm and users of these products. They satisfy a huge demand for high returns but are unavoidably at higher risks since there is no free lunch.

But in essence, these products act as (financial) amplifiers of risk when moving from one derivative level to the next. The amplified risk comes with amplified expected returns in accordance to finance theory.

The idea is in principle simple then: If one wants to create a product with higher expected returns, then one must create a new derivative level.

Examples of the new alchemy of D^3 derivatives are volatility ETNs such as XIV and ZIV.

Unlike old alchemy which did not pose systemic risks, these financial products amplify systematic risk and increase the probability of financial instability. This was confirmed in the last two weeks with the unwinding of the short volatility trade. Traders got ruined and funds risk liquidation while at the same time regulators appear ignorant of the risks or unwilling to deal with them.

In the stock market, a large percentage of participants invest their hard-earned pension money but there are also a few reckless speculators who play with D^3 products and endanger the stability of not only equities but of the global financial system and maybe the world.

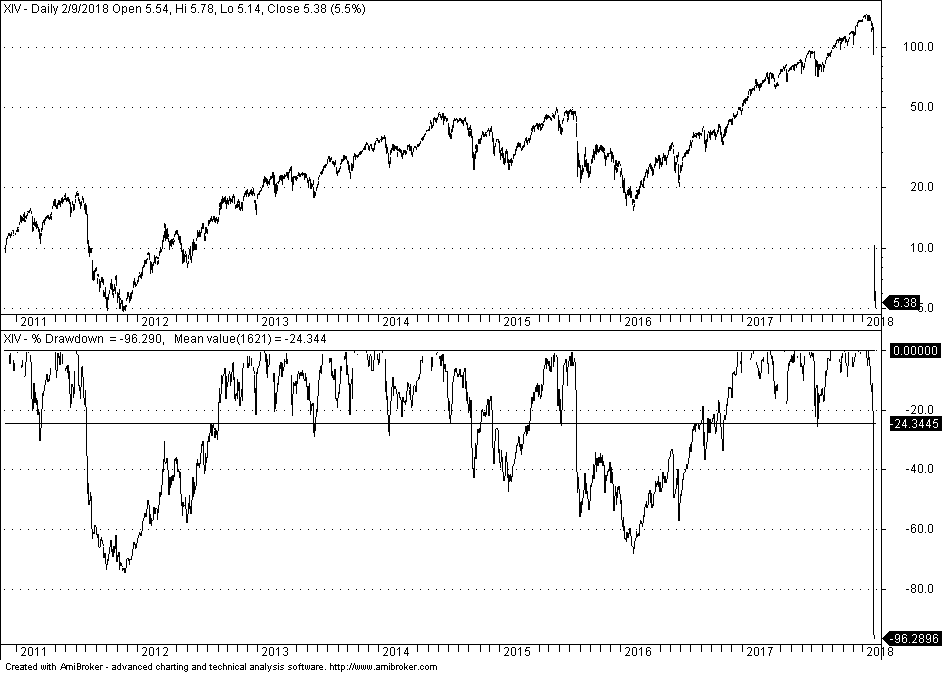

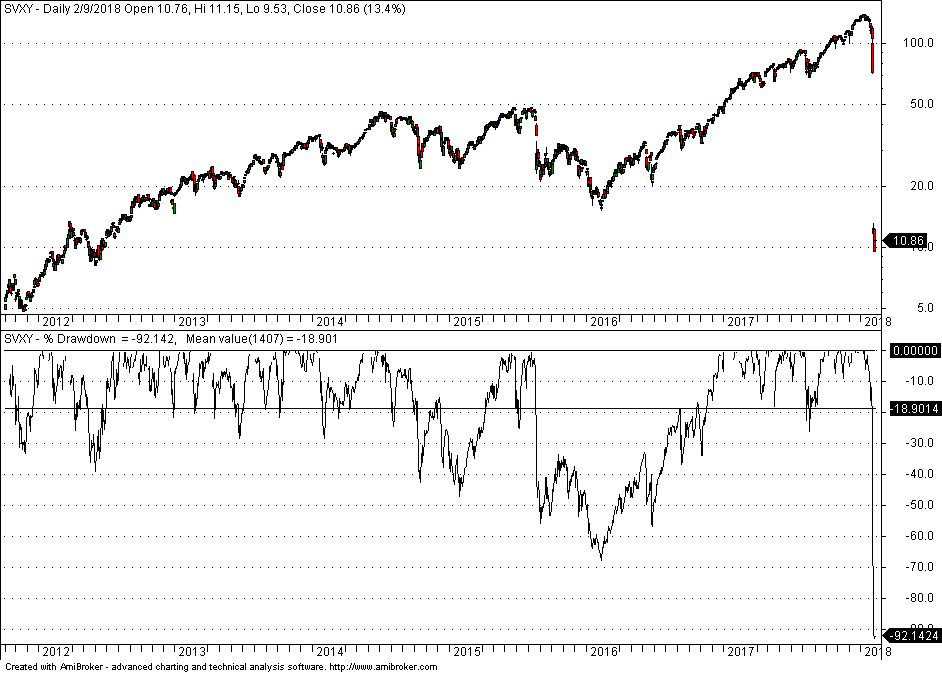

Below are XIV, SVXV, and ZIV charts with maximum drawdown on a closing basis from all-time highs. Click on the images to enlarge them.

|  |  |

In the last two weeks since the start of the unwinding of the short volatility trade, XIV has dropped 98.28% causing a termination event for this product, SVXY lost 92.14% and ZIV is down 30.06%.

The systemic risks from these events arise from the fact that at the end of the day (also literally) the managers of these products must hedge exposure and this is ultimately done by selling individual stocks because only stocks are not derivative products. This is the reason this stock market drop was the fastest ever since at least 1960.

It is quite interesting that Credit Suisse states in the XIV prospectus that the longer-term expected value of XIV is zero. Specifically in the Credit Suisse XIV prospectus, the following is stated

The long-term expected value of your ETNs is zero. If you hold your ETNs as a long-term investment, you will likely lose all or a substantial portion of your investment

However, many investors treated those D^3 products as longer-term investments and thought they were printing money. A vicious circle developed, with volatility going lower as hedging of the products by the issuers essentially pushed the market up. When some of the investors in these products started selling, issuers started selling stocks to adjust their hedged positions.

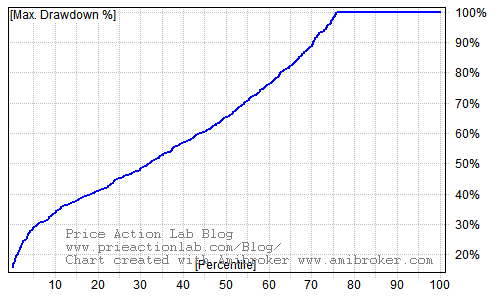

Under the assumption of independent and identically distributed daily returns, a Monte Carlo simulation reveals the risks. Below is the cumulative maximum drawdown distribution for XIV:

It may be seen that the maximum drawdown for 75% of the realizations is 100%! We can loosely say then that there is a 75% probability of total ruin when someone holds XIV long enough. In the same sense, the probability of a 90% or higher loss is about 85%!

In the case of ZIV, the probability of a 90% maximum drawdown or higher falls to 30%, as shown by the cumulative distribution chart below.

It is also interesting to compare to other popular ETFs. Below is a relevant table:

| ETF/ETN | P(Max. DD > 90%) |

| XIV | 85% |

| EEM | 60% |

| ZIV, GLD | 30% |

| SPY, EZU | 25% |

| QQQ | 15% |

| TLT | 5% |

The surprise in the above table is EEM with a 60% probability of a 90% or higher maximum drawdown. It is also interesting that ZIV and GLD have the same 30% probability for a 90% or higher maximum drawdown. SPY and EZU are at 25%. Another interesting result is that the probability for QQQ is lower than that of SPY although QQQ lost more than 80% of its value in the dot com crash. It is finally of no surprise that TLT is at the bottom with a 5% probability of a 90% or higher drawdown. The results are conditioned on the historical returns samples.

The development of D^3 products, or derivatives of derivatives of derivatives, fulfills an appetite for high returns at high risks but poses a significant risk to the financial system and maybe to the global stability of economic and even social systems. We all saw the results of the derivatives on real estate loans and their role in the financial crisis with whole countries driven to bankruptcy. There may be also unknown consequences from using these products in the form of black swans. Maybe it is time to reconsider products built on multiple layers of derivatives.

If you found this article interesting, I invite you to follow this blog via any of these methods: RSS or Email, or follow us on Twitter

Charting and backtesting program: Amibroker