Predicting economic downtrends is hard due to reflexivity.

Last December I received an invitation to give a presentation at the M4 conference in New York alongside some heavy names such as N. N. Taleb, Scott Armstrong, and Peter Carr, just to name a few. My talk was about reflexivity in financial market forecasting.

In a nutshell, my opinion is that the major causes of failure of economic forecasts are not noisy data, bias-variance trade-off, non-stationarity, or weak models. The models are good and have worked well in dealing with a variety of other problems. The main cause of uncertainty in economic forecasting is reflexivity.

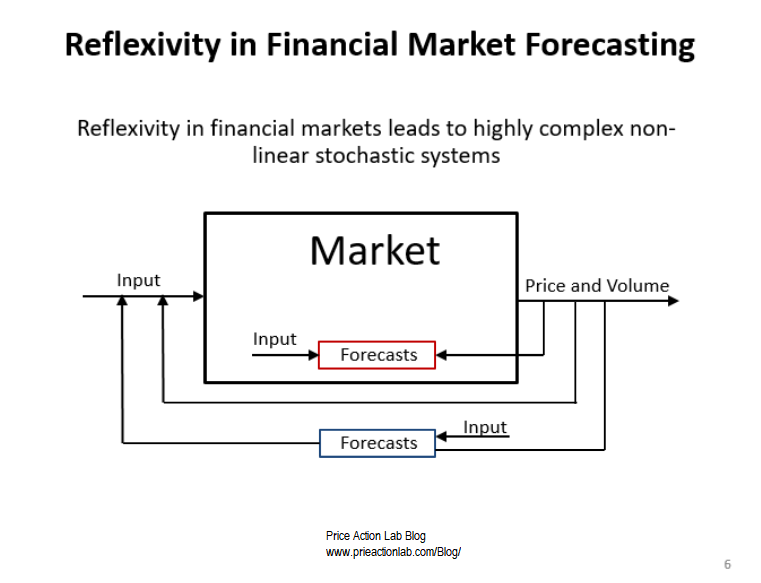

This is how reflexivity works in financial trading as depicted in one of the slides I used in the M4 conference. You can find the presentation here.

Forecasts are essentially active participants in the market and affect price and volume. In turn, price and volume changes affect forecasts. This is a reflexive relationship. This is not the same as weather forecasting where forecasts cannot affect the outcome. Therefore:

Forecasting + Reflexivity = Highly Complex System

We should not blame the models, the data, or at the end of the day the forecasters. Financial and economic systems are complex due to reflexivity. Here is what happens:

- The central bank, investment banks, economists, etc., issue forecasts.

- These forecasts are used in turn to tune economic policy and decisions.

- Therefore, the forecasts influence the future course of the system.

Is there a better way to predict the next economic downturn?

The answer is no since we have no way of modeling reflexivity effects.

However, here is the interesting part in my opinion:

Traders (individuals, fund managers, etc.) care more about what to do when the next downturn occurs rather than predicting it. Usually, people with skin-in-the-game know such predictions are impossible and can even be costly when wrong. Therefore, using past market data they simulate various models and their reaction to downturns to determine the best action. In my opinion, this is what separates practitioners from academics. Of course, academics are interested in solving the problem in some general way if possible but practitioners care about empirical ways of dealing with it.

If you found this article interesting, I invite you to follow this blog via any of the methods below.

Subscribe via RSS or Email, or follow us on Twitter

If you have any questions or comments, happy to connect on Twitter: @mikeharrisNY