More gamblers are realizing this year that the stock market is a better casino because it offers higher odds of winning than traditional gambling. This may be one reason for the large influx of new speculators to the stock market this year.

Odds of winning in traditional casinos are very low although payouts may be high in case of win. For example, in American roulette, single number player winning odds are 2.6% and payout is 35 to 1. Highest odds are 47.4% for even bets and payout is 1 to 1. Expectation is negative for most games that do not involve skill and as a result a player goes broke after a sufficiently long period of time and depending on the game played.

The stock market can offer higher odds of winning although pay-offs may be smaller. There is also the perception that it is possible in the market to have positive expectation if there is an edge, which is something that may be impossible, or even prohibited in traditional gambling establishments. For these and other reasons, more and more gamblers are converting to traders, especially after Robinhood brokerage started offering commission-free trading. There are of course risks and misconceptions in this area but these are not the subject of this brief article. The subject here is that the idea that the markets are better casinos is in principle correct in the case of some particular liquid securities.

We will demonstrate this point with simulations of random traders that toss a fair coin before the market close (given enough time to place an MOC order) to decide whether to go long or short. If heads show up, the random trader goes long. Then next day before the close, the coin is tossed again. If heads show up again, the position is kept open but if tails show up it is reversed to short, and so on.

In all simulations below I have included $0.01/share commission/slippage. There is no reinvestment of profits. The simulation is performed for 20,000 traders and the initial capital of every trader is $100K. There is no use of margin.

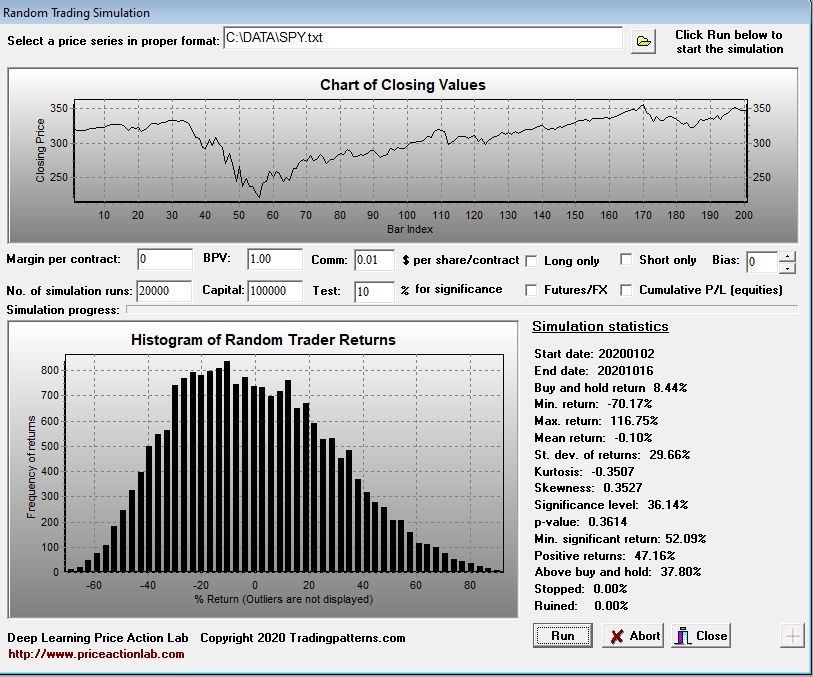

Case 1: Random SPY trading from 01/02/2020 – 10/16/2020

Buy and hold in the period considered for SPY is 8.44%. About 47.2% of the random traders profited and a little more than 36% made more than 10%. The lowest return is about -70% but the highest return is around 117%. No traders were ruined. The distribution of returns for the random traders has -0.35 excess kurtosis and nearly 0% mean. However, standard deviation is large, about 30%. This is an excellent casino for gamblers that think they are traders; the odds of winning are high while there is a perception of use of skill and possibility of a positive expectation (edge.) Also, note that about 38% of the random traders made more than the buy and hold return! If they are lucky to repeat this for a few years they can even raise money to start a fund…

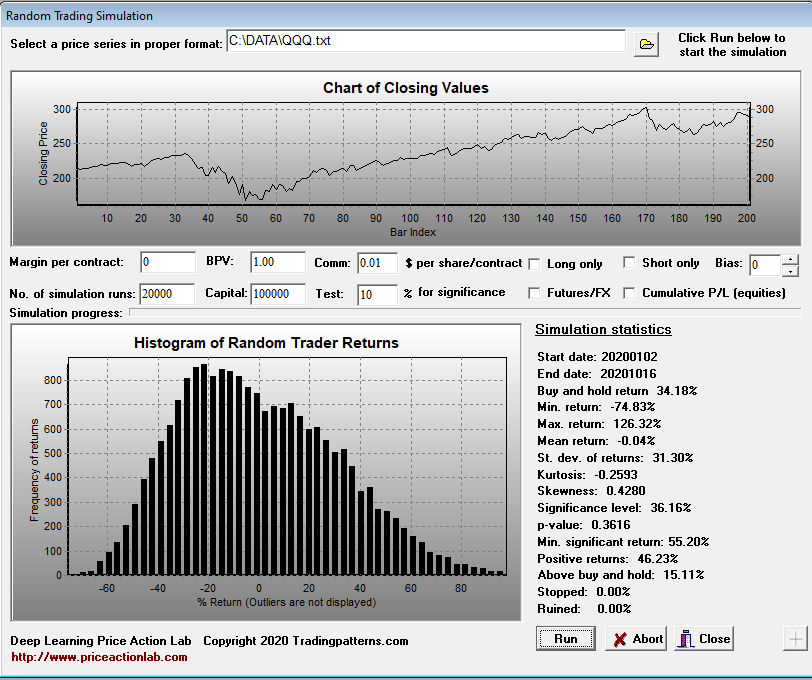

Let us look at QQQ random trading below.

Case 2: Random QQQ trading from 01/02/2020 – 10/16/2020

In this case more than 46% of the random traders profited and 15% made more than the buy and hold of 34.2% in the period considered! About 36% of the random traders made more than 10%. This is another good casino that offers high odds of winning.

Let us look at AAPL stock next.

Case 3: Random AAPL trading from 01/02/2020 – 10/16/2020

In this case more than 44% of the random traders profited and close to 37% made more than 10%. However, only 8% made more than the buy and hold return of 56.6%. Lowest return is about -84% but highest return is close to 159%.

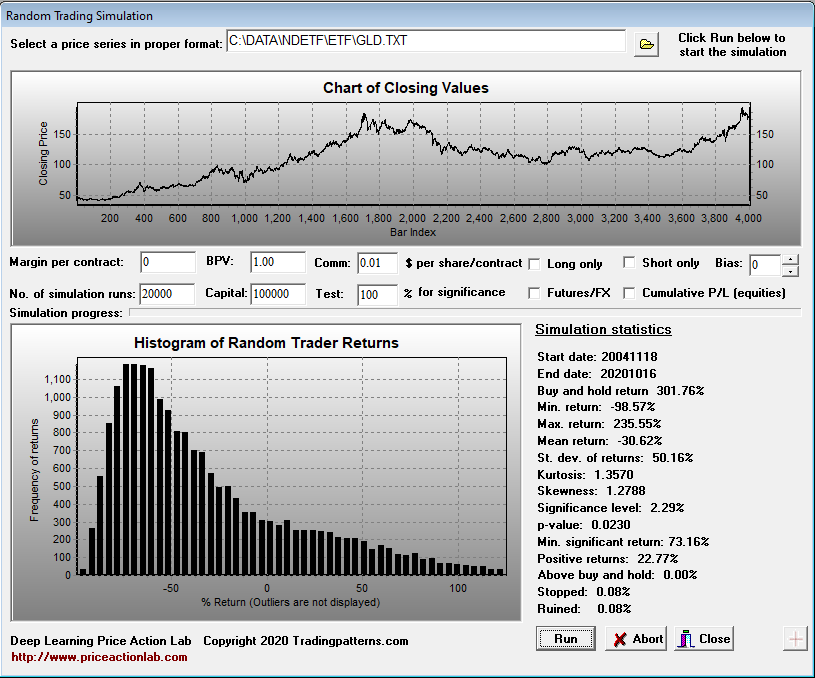

Let us look at the gold ETF GLD next since inception.

Case 3: Random GLD trading from 11/18/2004 – 10/16/2020

In a period of about 16 years, close to 23% of the random traders profited although about 2.3% made more than 100% but the fraction of winners is high.

Therefore, chances of profiting in the market casino for random traders are much higher than the chances of casino gamblers. In fact, if the random traders choose the proper market, they may have higher chances of making money than some quants because the methods of these sophisticated market participants use often turn out to be worse than random.

Caveat emptor: The above simulations assume the actions of random participants do not impact price action. In case the number of random market participants increases significantly there will be impact on price action and a likely result will be the inability to profit in the longer-term due to lower odds of winning. In addition, the longer a random trader stays in the market, the higher the probability of ruin due to random periods of persisting negative expectation.

Simulation program: DLPAL S

Data provider: Norgate Data

If you found this article interesting, you may follow this blog via push notifications, RSS or Email, or in Twitter

Price Action Lab Blog Premium Content