The most robust equity portfolio hedge is cash, but for this to work, it requires timing the market. However, it is not as complicated as opponents of market timing claim.

Bonds are not a hedge.

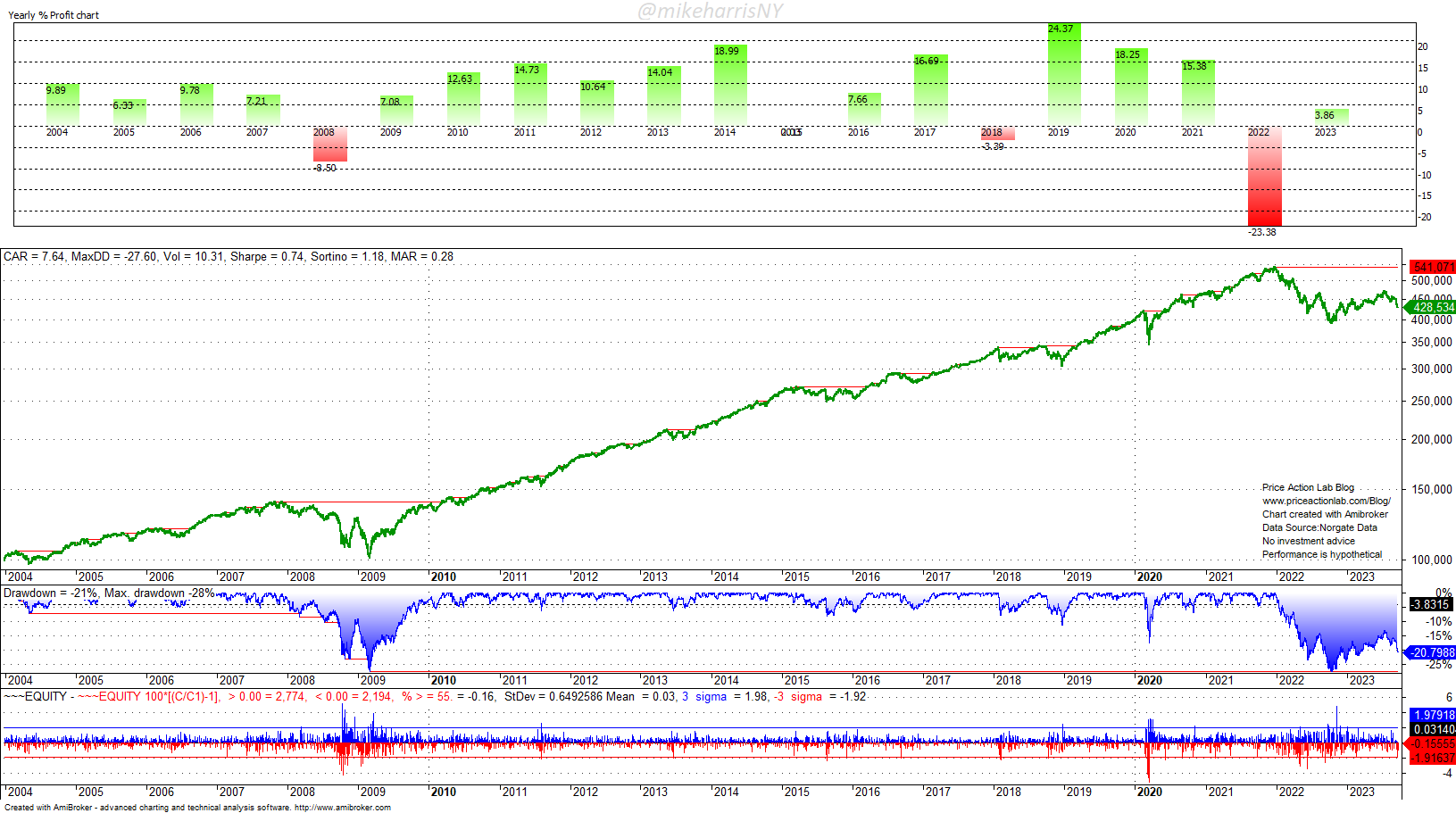

Those who needed proof that bonds are not a good hedge for an equity portfolio found it last year. The 60/40 allocation in SPY and TLT ETFs with annual rebalancing plunged 23.4%. Since 2004, the worst down year was 2008, with a loss of 8.5%. It was a devastating shock to 60/40 investors.

Although allocations with shorter duration bonds did better last year, it is highly likely that the 60/40 portfolio reputation has been permanently damaged.

Gold is not a hedge.

Gold is a catastrophe hedge, subject to several conditions, but not in paper or coins. Gold can be stolen or confiscated by authorities.

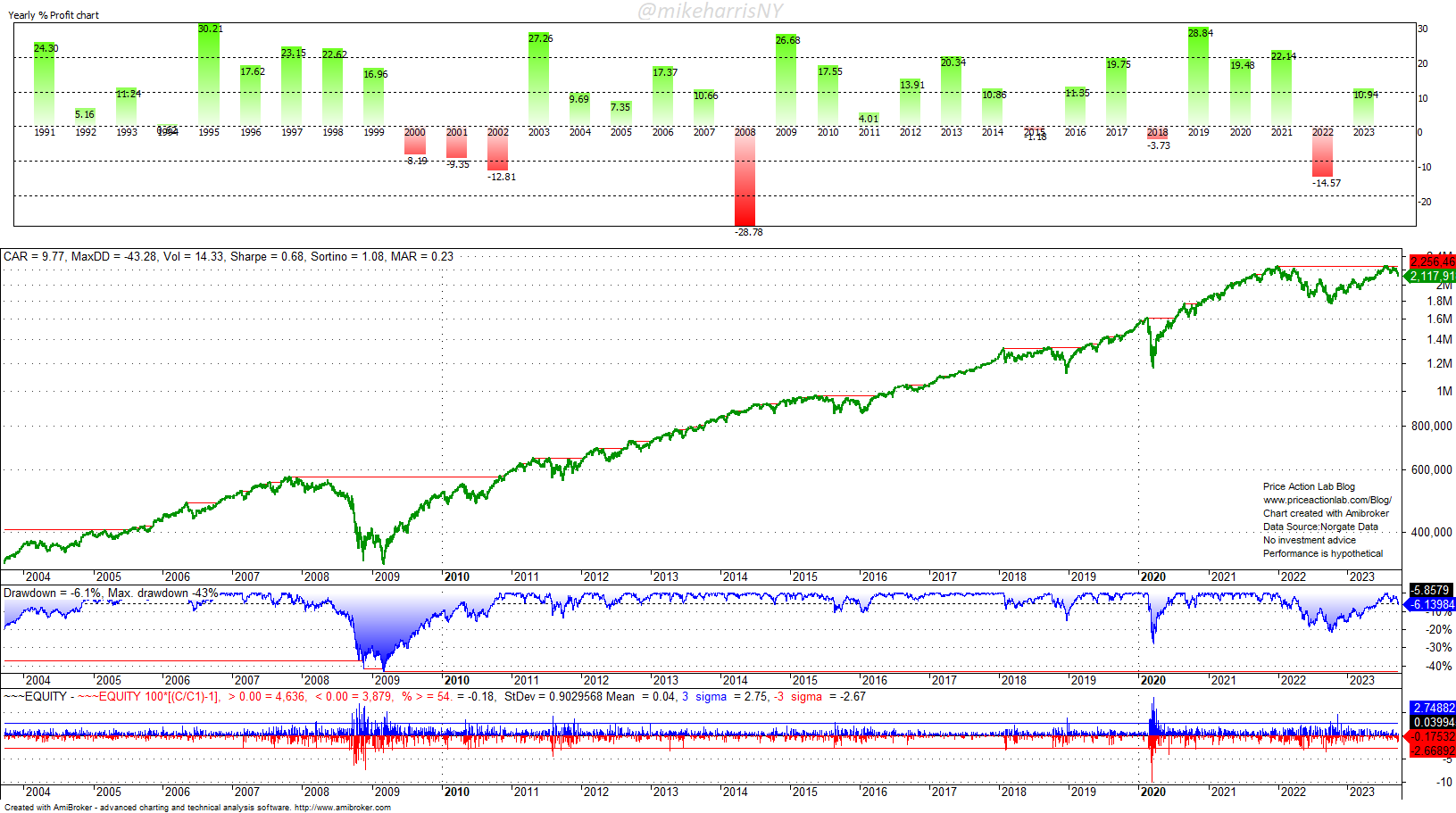

A portfolio with an 80% allocation to the S&P 500 total return and a 20% allocation to gold did not offer a hedge during the dot-com and financial crisis bear markets. Last year, the gold allocation helped reduce equity market losses by about 4%.

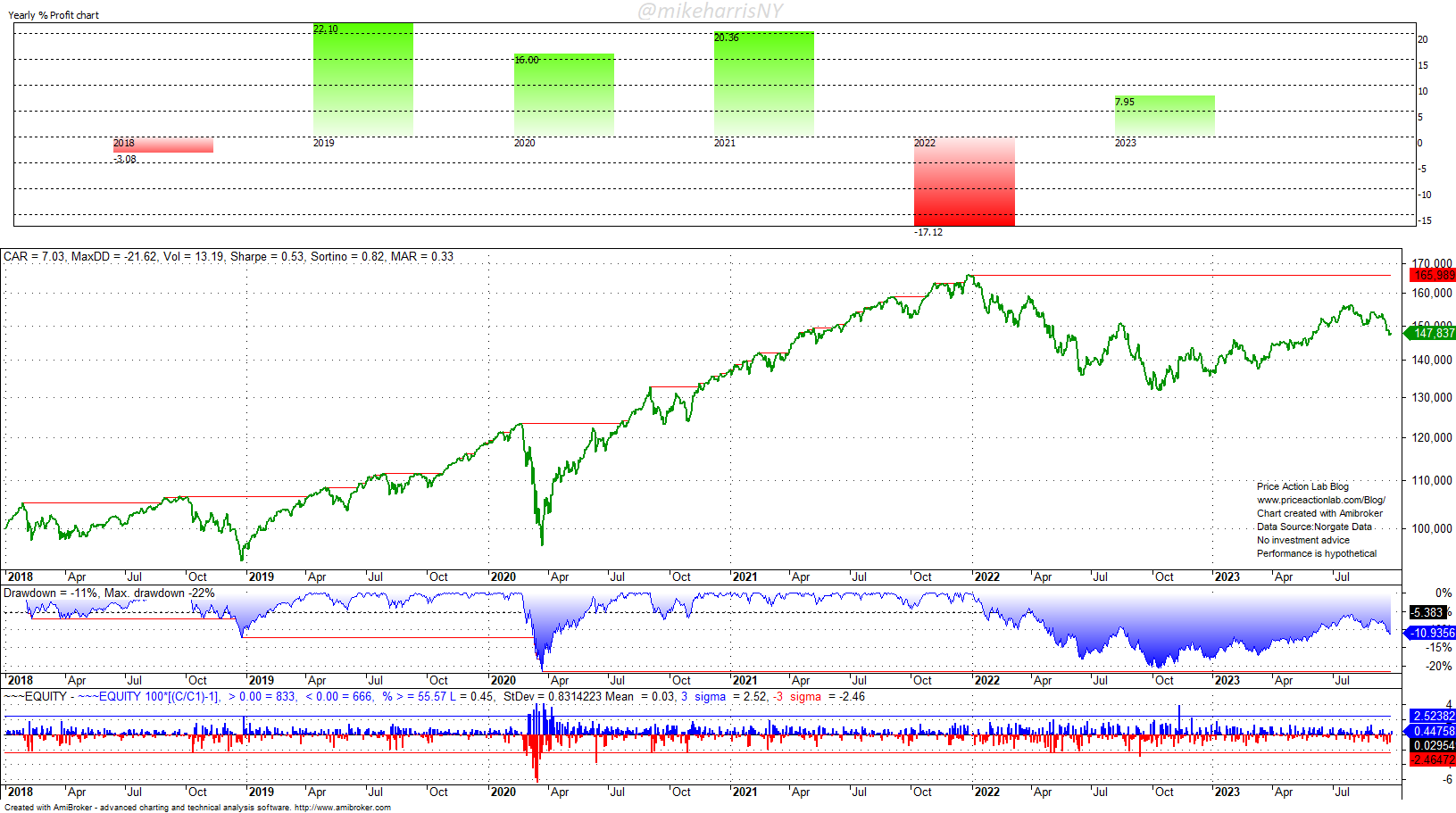

Market diversification is not a hedge.

Diversification can be a wealth preservation scheme as long as the risk-adjusted returns it offers are reasonable. The main objective is to protect purchasing power from inflation. However, during adverse market conditions, diversification may not provide a hedge. The “all-weather” portfolio is an example of what can go wrong.

Investors in “all-weather” thought they had discovered an allocation with superior risk-adjusted returns until 2022 came with a 19% loss.

Managed futures are not a hedge.

There is no law that says managed futures must go up when stocks are falling. It has happened in the past (e.g., 2008, 2022), but as with stocks and bonds and a higher correlation while both were falling last year, the same could occur in the future for managed futures.

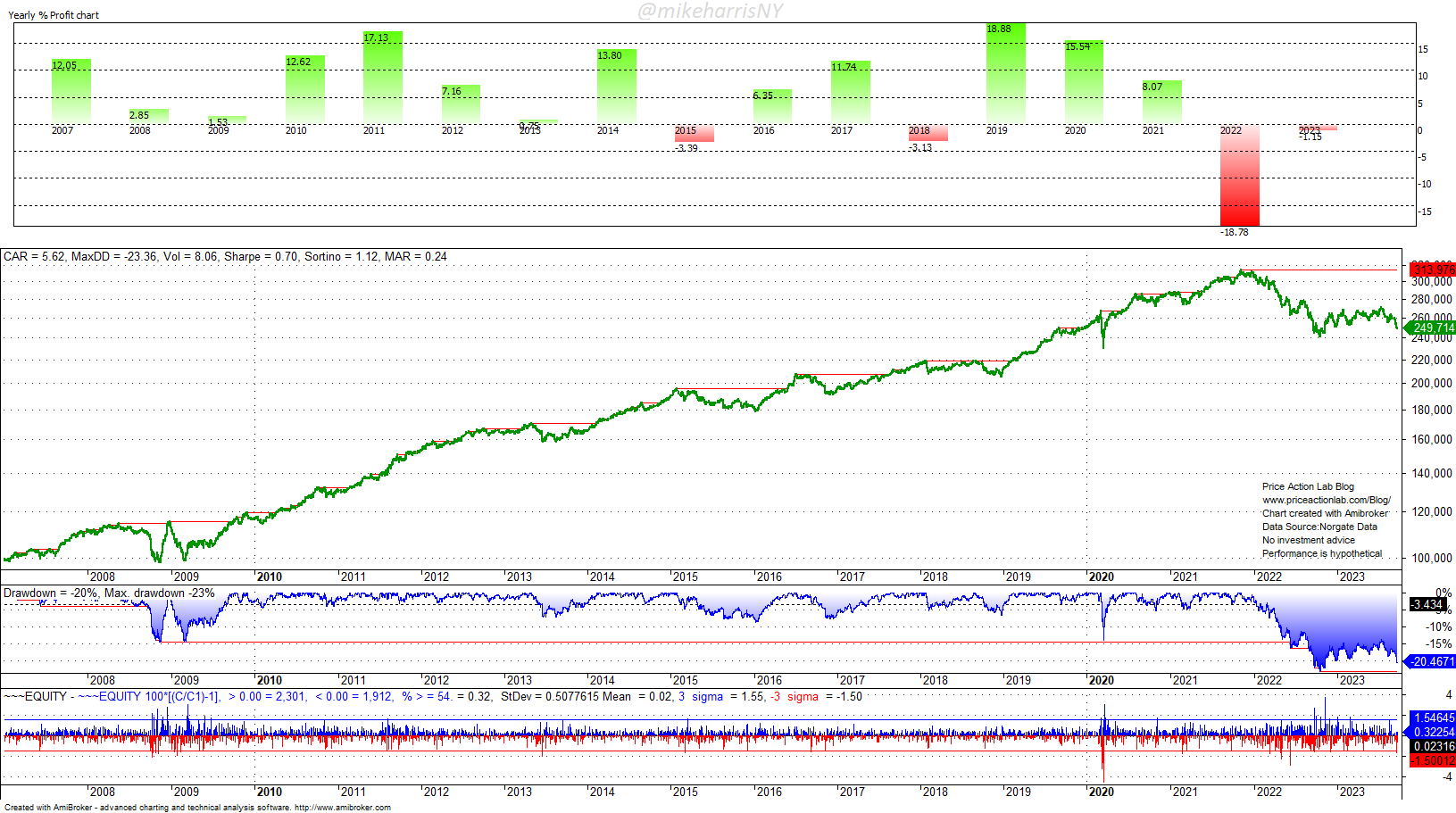

Below is a backtest of a 70/30 allocation in the S&P 500 total return and the SG CTA Index.

In 2008 and 2022, this allocation offered a partial hedge, but a Sharpe of 0.54 is too low to offer hope of a robust performance. The low Sharpe of managed futures, which arises mainly due to the high volatility of returns, is one reason the marketing departments stage attacks on this important measure of risk-adjusted returns and declare it useless.

Put options are an expensive hedge.

Hedging with put options is not trivial and requires a sophisticated timing strategy. If the options are not sold at the right time, theta burn may consume all their benefits, and the cost of the hedge will significantly impact the performance of the portfolio. This is a challenging timing problem with no easy solution. Hedging with options is financial alchemy. Modern alchemists offer promises of a robust hedge, but things can go wrong with the timing.

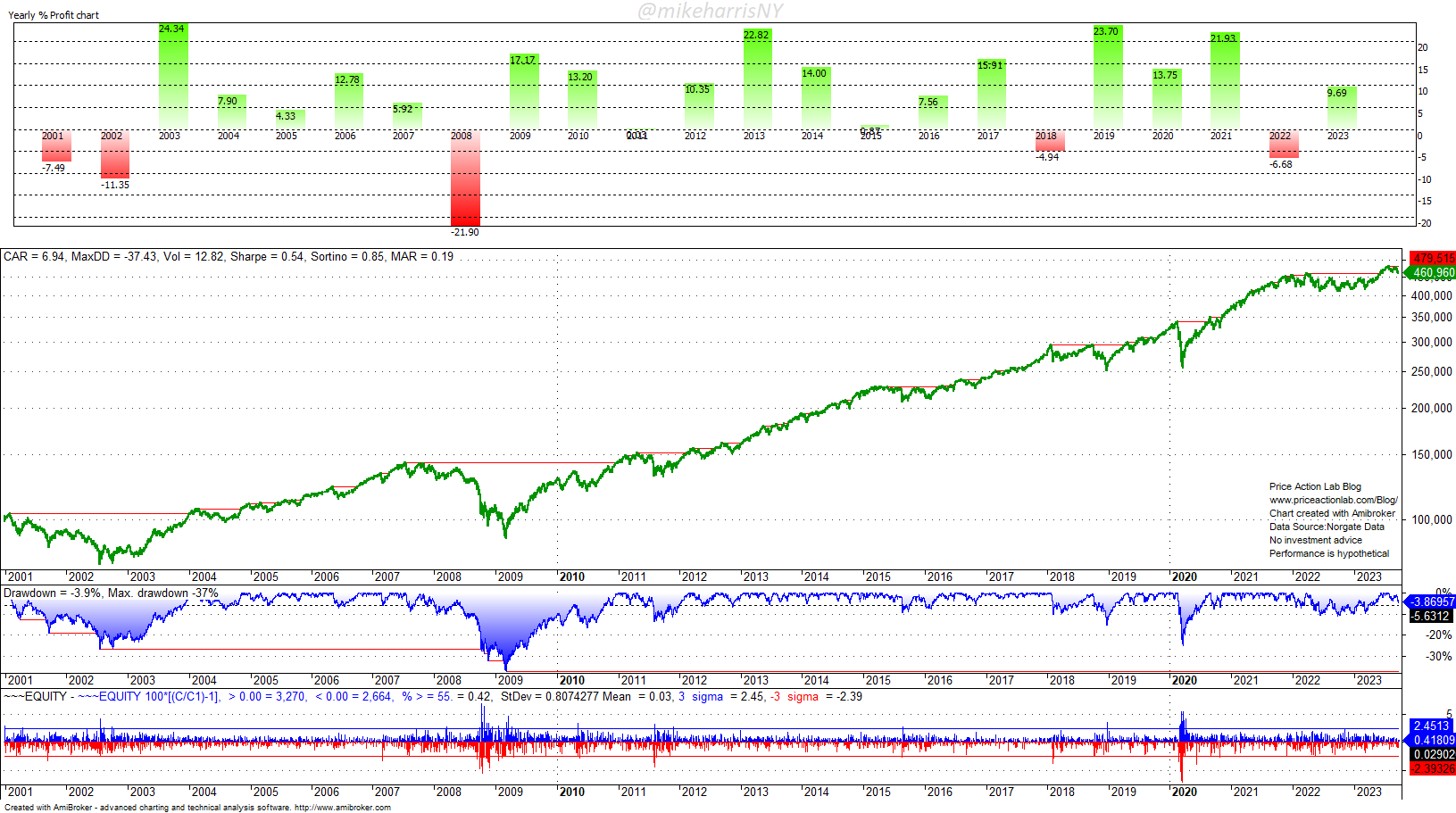

Let us look at a “naïve” 80/20 allocation to SPY and TAIL ETFs.

Last year, the allocation to the tail-risk ETF did little to reduce losses. The main reason was the slow “pain trade” that basically resulted in excessive theta burn for put options. With some sophisticated timing, a tactical allocation could have performed a lot better, but if someone can time the market, the hedge is not even required. This is the main message of this article.

Strategy diversification is not a hedge.

Strategy diversification can provide better risk-adjusted returns, but all strategies are subject to tail risks.

Allocating 50% to two uncorrelated strategies with the same annualized return and volatility will result in the same annualized return but lower volatility by the square root of 2. Therefore, the Sharpe ratio will increase by a factor of about 1.4. This is a good result, provided the strategies are truly uncorrelated. What could go wrong?

Correlation is a random variable that depends on market regimes. The bad scenario is that one of the strategies loses its edge and becomes unprofitable. A worst-case scenario is when one of the strategies hits an absorbing barrier. Many things can go wrong with strategy ensembles. This method of diversification is not a panacea, as some newcomers to ensemble alchemy believe, especially when the strategies have hidden high correlation modes that can be triggered due to extreme market moves.

As a general rule, any attempt to present strategy diversification as a solution to the hedging problem should be met with skepticism. Strategy diversification is a scheme for better risk-adjusted returns, not a hedge.

What is a robust hedge?

The most robust hedge is staying out of a falling market. This is a timing problem. The best investors are also excellent traders. The passive vs. active debate is a false dichotomy.

Especially in a market environment with T-Bills paying a high interest rate, simple market timing methods can produce a superior hedge and performance.

In another article, I will discuss some simple but robust methods of market timing.

Price Action Lab Blog Premium Content

By subscribing you have immediate access to hundreds of articles. Premium Articles subscribers have immediate access to more than two hundred articles and All in One subscribers have access to all premium articles, books, premium insights, and market signals content.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS, Email, or Twitter.