This trend-following trading system is based on an algorithm that adapts to market conditions and it is significant at the 99.86% level in the case of SPY based on the performance results obtained from 20,000 simulations of a random system. There are only two parameters in the system and it is profitable in several tickers without any adjustments. Since inception of SPY the win rate is 100% and the CAR is 10.66%.

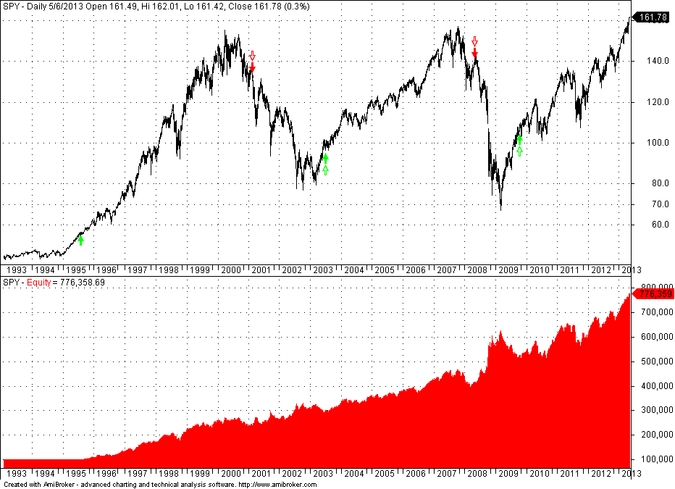

One way of surviving in a constantly changing market environment is by employing truly adaptive trading systems. I make a distinction between “truly adaptive” and “pseudo adaptive” systems in the sense that adaptation of the former kind is proactive rather than reactive. The SPY system with proactive adaptation has generated 5 trades since SPY inception that have tracked the major trends of the market quite well as shown in the chart below:

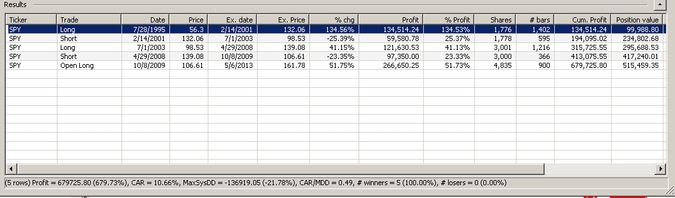

The green and red arrows show the entry and exit points of this system. This is a stop and reverse system, i.e. when a short signal is generated it closes an already open long signal and the other way around. Below is a trade list table:

The entry and exit dates are shown on the above table along with the CAR value of 10.66%, the maximum system drawdown of -21.78% and the 100% win rate. These results are for a fully invested system with 100K initial equity.

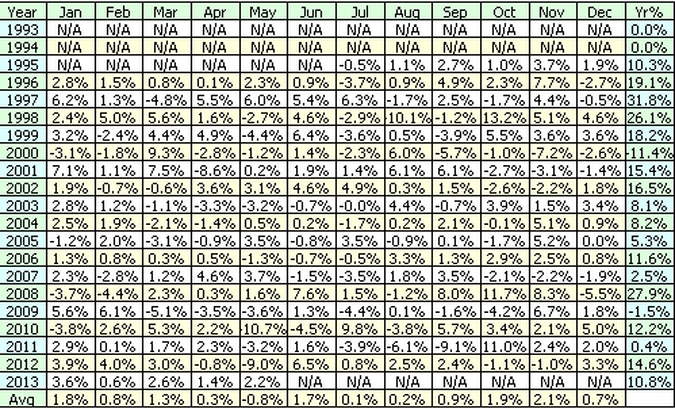

The trading system had only two losing years since SPY inception, -11.4% in 2000 and -1.5% in 2009. Since this is a long/.short system, its performance in 2008 was 27.9%:

Analysis

There are two basic issues to be investigated and concern whether this could be a random system and the fact of a small trade sample. The first issue is considered below and a detailed answer to the second will be provided in another post. The short answer for now is that this system has been profitable in a good number of related symbols and markets and that can be used to increase the trade sample.

Randomness issue

The randomness issue is about the possibility that this is a random system with an algorithm that possesses no intelligence in matching market returns with its signals. In a post two days ago I presented the results of the simulation of 20,000 runs of a random SPY trading system. Given those results, the system in this post turns out to be significant at the 99.86% level. This means that only 0.14% of the random systems managed to exceed its performance. It also allows as to reject the null hypothesis that the system possesses no intelligence. Nevertheless, nothing in this analysis precludes the possibility that the system may generate losses in the future. Unfortunately, this is the nature of trading and statistics. However, the numbers look very good for this long-term trend-following system that can be used by “quasi passive funds” to manage money for the longer term.

As a final note, the system in this post is not equivalent to some optimized moving average crossover. Those systems tend to have much lower significance as discussed in another post and also generate significantly higher drawdown.

Disclosure: no relevant position at the time of this post and no plans to initiate any positions within the next 72 hours..

Charts created with AmiBroker – advanced charting and technical analysis software. http://www.amibroker.com/”

{kind=link}