Six months are not responsible for all gains in stock market since 2000. This conclusion in some articles was based on the wrong choice of returns. The correct number is about 32.

Brief review of basic concepts

where Ri are the arithmetic returns. Now suppose we rank the returns because we want to determine the number of returns g that has contributed to net gain, with g ≤ n.

The claim is that the overwhelming majority of the returns in the equation above cancel out. This is what is done in those articles after ranking returns from highest to lowest and obtaining the result that only 6 months have contributed to gains since 2000.

The second term in the above equation, the product from g+1 to n, comes out to 1 and we are left with g returns contributing to gains. For SPY since 2000 g is about 6.

However, the above approach focusses on total return and ignores time ordering of returns and their contributions to actual equity growth in time domain. One can see why this approach is wrong after using first differences (difference of two consecutive monthly closing prices) that allow computing the net change in the period under consideration, as follows

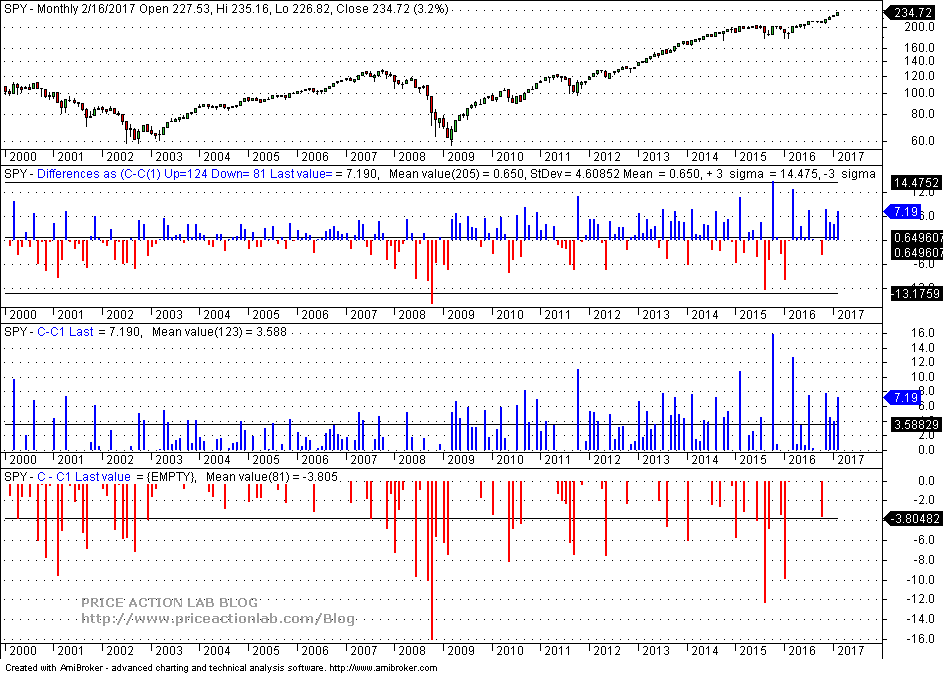

where Di are the first differences. Below is a monthly chart of adjusted SPY prices since 01/2000.

The above chart shows first differences in first pane and then positive and negative first differences in the next two panes. The mean of positive first differences is 3.588 points. If we divide the net change since 2000, which is 133.17 points, by this number we get 31.6 as the approximate number of months on the average that have contributed to the gain in net change.

The difference between the wrong result of 6 months and 31.6 is huge. Note that the wrong result was used in arguments in support of passive investing since it is hard to time gains of just 6 months in a total of 205 months. However, this is not so because the result was totally off. The correct result of about 32 months leaves plenty of room for a good timing model to maneuver.

If you have any questions or comments, happy to connect on Twitter: @mikeharrisNY

Subscribe via RSS or Email, or follow us on Twitter.

Charting and backtesting program: Amibroker

Disclaimer

Technical and quantitative analysis of Dow-30 stocks and 30 popular ETFs is included in our Weekly Premium Report. Market signals for longer-term traders are offered by our premium Market Signals service.