We are pleased to announce DLPAl DQ, a quantitative scanner for stock, futures and forex traders operating in discretionary or quasi-systematic mode.

Deep Learning Price Action Lab for Discretionary Quants (DLPAL DQ) is the latest addition to our products after retiring DLPAL PRO, a version that incorporated three main functions: search, scan and feature engineering for long/short strategies.

DLPAL DQ is an end-of-day (EOD) scanner. The program identifies parameter-less strategies in historical price data that fulfill user-defined performance statistics and risk/reward parameters as of the last bar in the input data files. These strategies are also known as price patterns. DLPAL DQ generates code for strategies and systems for the Quantopian platform, Tradestation (EasyLanguage), Multicharts (EasyLanguage), NinjaTrader 7 and Amibroker AFL. The program also offers two validation methods.

Click here for information of how to request a fully functional two-week trial of the program.

An example

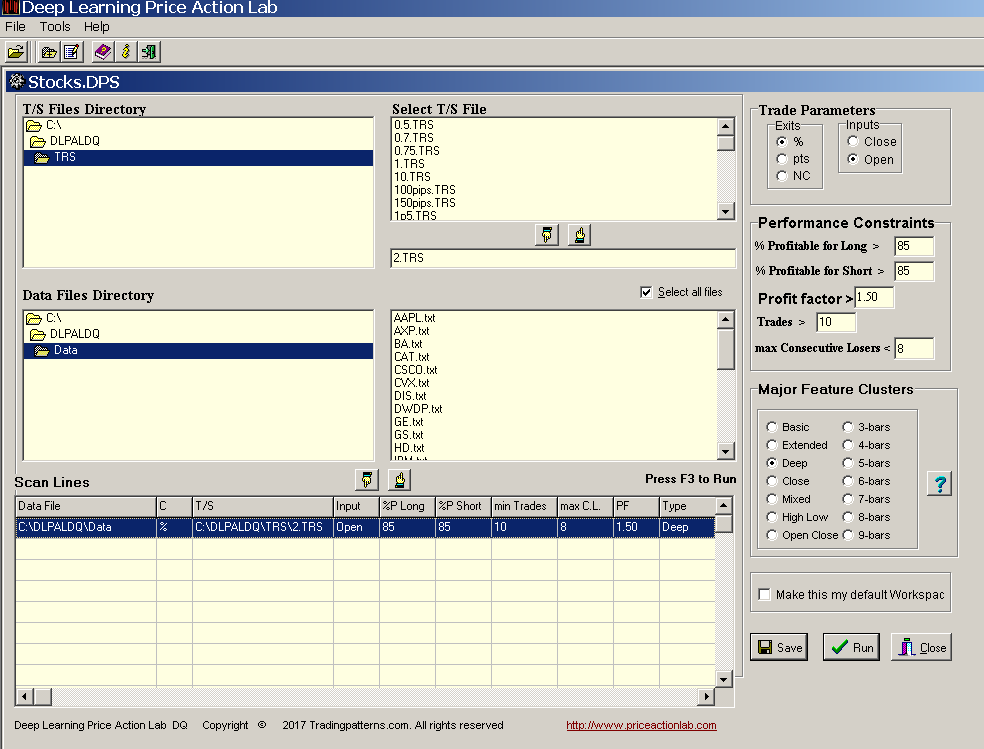

Below is an example of how DLPAL DQ can be used to identify price action anomalies in stocks. We scan all Dow 30 stocks with data from 01/03/2000 to 01/16/2017 for high probability patterns using the most comprehensive feature cluster called Deep. This is the scan workspace:

We set the profit target and stop-loss to 2% because we focus on timing, not trend. We require that each identified anomaly has occurred more than 10 times in the history of a stock and it is more than 85% profitable. Below are the results of the scan:

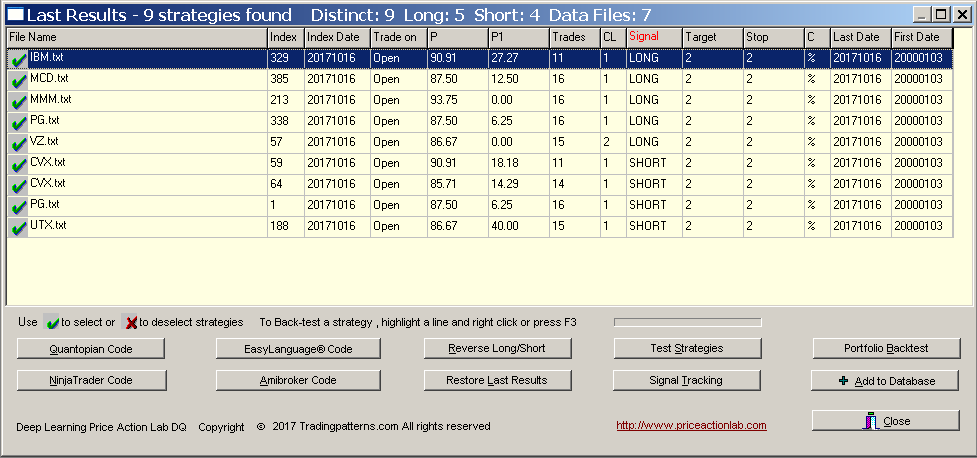

In the scan results above each line corresponds to an exact strategy. P is the pattern win rate, P1 is the 1-Bar win rate, Trades is the number of trades, CL is the maximum number of consecutive losers and Target and Stop the values of the profit target and stop-loss. C indicates the type of target and stop-loss.

DLPAL DQ identified 9 strategies, 5 long and 4 short. However, these strategies may be over-fitted to noise or special market conditions. We use a portfolio backtest in all Dow 30 stocks for each strategy to validate them. The rationale is that if these strategies are genuine they should be profitable in many stocks, not in just one.

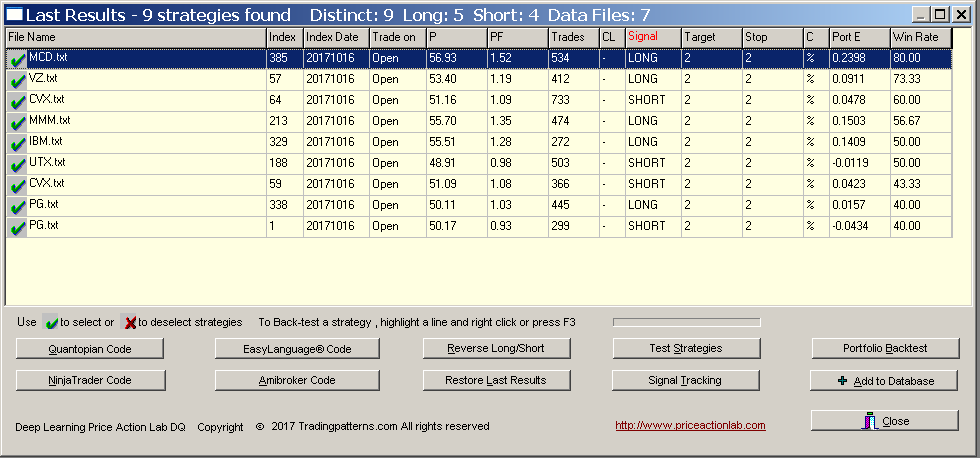

DLPAL DQ allows fast and efficient portfolio backtests. The results are shown below:

P is the pattern win rate, Trades is the number of trades and Target and Stop the values of the profit target and stop-loss. C indicates the type of target and stop-loss (%, points, or next close exit). In the case of portfolio backtests, PF is the portfolio profit factor, PortE is the portfolio expectation and Win Rate is the proportion of securities with positive expectation.

Normally, we would like to have high Win Rate (last column) and high P, portfolio win rate. This would mean that a strategy is profitable in many stocks with a high success rate. We also want Profit Factor greater than 1 and positive portfolio expectancy PortE.

From the above results it may be seen that two strategies have profit factor less than 1, i.e., they immediately failed the test. After sorting for highest Win Rate only one strategy has Win Rate greater than 75%, our subjective criterion for this test. This is a strategy for trading MCD. There are 534 trades in the portfolio backtest for this strategy and the win rate is 56.93%. We can confirm these results by generating code for Amibroker and performing a portfolio backtest in that platform:

Note that MCD has gained 0.84% from the open of 10/17/2017 to the close of 10/20/2017.

In case we decide that this is a significant strategy we can add it to Signal Tracking. It will also show up in the future in the scan results. The scan results are generated daily after updating the data files.

You may have noticed that there are several options for a scan feature cluster. Users can choose the cluster that shows more promising based on tests. This is a tool for traders that are quantitatively oriented and like to do their own analysis. The tool does not make any suggestions of how to use it; it just finds the strategies but those must be validated by the user based on some criteria.

Some more details about this product and general comments

We have determined in the past that most of our customers used only one of the functions of DLPAL PRO. Systematic traders used the search function to develop trading strategies, discretionary quants used the scan function to analyze the markets for opportunities and professionals, such as hedge funds, mainly used the long/short feature engineering function with fixed strategies or machine learning classifiers.

Therefore, we have decided to create separate products for each function that are now available as DLPAL S, DLPAL DQ and DLPAL LS. In this way our customers can get the functionality they want without unneeded options.

Although there is a tendency in the industry to load software with functionality, we have decided to take the opposite route because in any way we are the pioneers in this area: we developed the first product that discovers automatically trading strategies and writes code for major platforms in 2000 and since the competition lags behind because most of the products they offer are not based on sound principles but instead attempt to impress the user with functionality that can cause more harm than good.

An example of unneeded functionally is Monte Carlo simulations and related fancy graphs. Anyone with skin-in-the-game knows that these simulations are not very useful when multiple trials are made to identify trading strategies. As it turns out, over-fitted strategies respond well to these tests. So why is it that some products offer them as the main test of significance along with also unneeded and ineffective out-of-sample testing? The main reason is that the developers are inexperienced in this area although they may be good programmers.

Most strategies identified from the data fail when tested on a portfolio of comparable securities that is determined in advanced, not chosen after the fact to force significance, as it is done by some authors in blogs and articles. Yet, the portfolio backtest is the main test of significance in DLPAL DQ because our intention is providing something of value to traders while at the same time being honest about it.

Click here for information of how to request a fully functional two-week trial of the program.