There are a few issues when calculating correlations between bitcoin and traditional markets for use in asset allocation. Two examples are included below.

A few days ago I saw a tweet by a”bitcoin investor” recommending that investors should include the cryptocurrency in their portfolio because its correlation to stocks is very low.

To start with, correlation is not the only factor when deciding which assets to include in a diversified portfolio. Investors must also look at expected returns and their variance. Suggesting to investors to diversify into bitcoin because it has low correlation to stocks is naive, to say the least, without the additional details of how this diversification will impact portfolio performance. If the longer-term expected return from an investment in bitcoin may be low or even negative, why investing in it in the first place?

When calculating the correlation between bitcoin and traditional assets we must take into account the following issues:

- The history of bitcoin is relatively short

- The volatility of bitcoin is an order of magnitude larger than that of stocks

- Bitcoin trades every day of the week while stocks do not trade during the weekend

We will focus on the last issue in this article. There are at least two ways of dealing with the issue of trading frequency when calculating the correlation between bitcoin and stocks:

- Synchronize bitcoin to stocks by removing weekend trading

- Synchronize stocks to bitcoin by assuming flat prices during the weekend

- Synchronize bitcoin to stocks by removing weekend trading

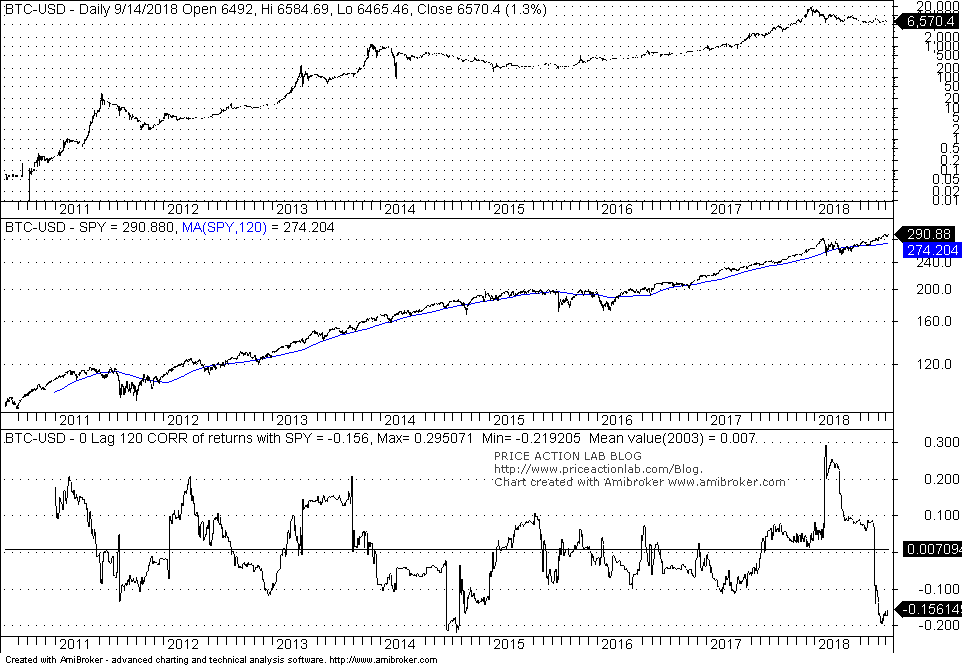

The 0-lag, 120-day correlation of simple returns between SPY ETF and bitcoin after removing price changes during the weekend is shown below:

Figure 1. 0-lag, 120-day correlation of simple returns between SPY ETF and bitcoin after removing price changes during the weekend

Note that although the average 120-day correlation according to this method is closer to 0, since 2011 the 120-day correlation has varied from a maximum of +0.295 to a minimum of -0.219. For example, near the start of this year the 120-day correlation was at the maximum level only to turn negative recently. Also note that the 120-day moving average last price for SPY is 271.204.

The last value of the 120-day correlation is -0.15 and close to the minimum value.

2. Synchronize stocks to bitcoin by assuming flat prices during the weekend

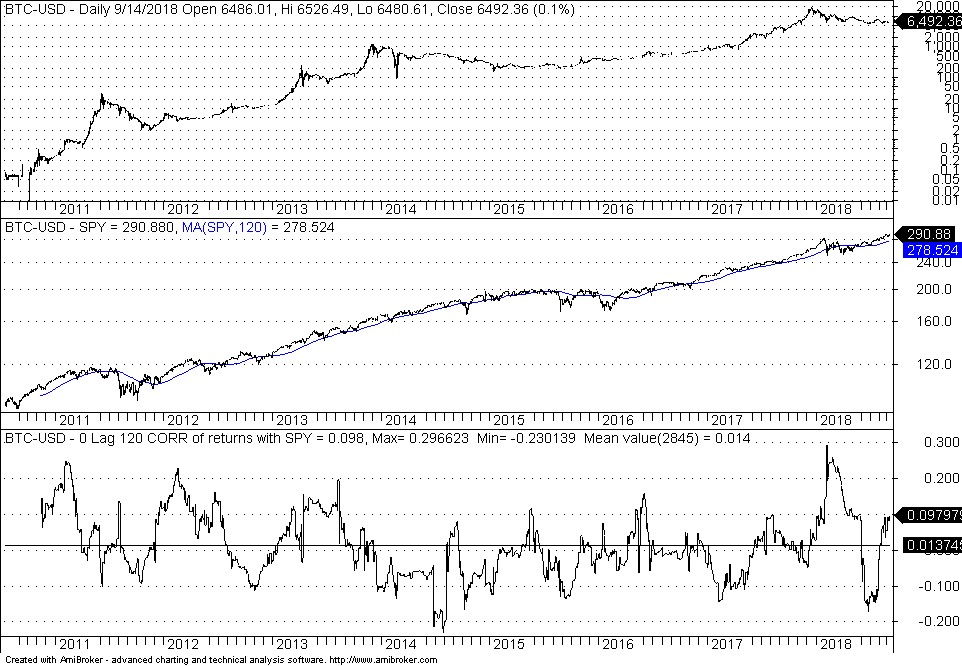

The 0-lag, 120-day correlation of simple returns between SPY ETF and bitcoin after assuming flat price changes for the latter during the weekend is shown below:

Figure 2. 0-lag, 120-day correlation of simple returns between SPY ETF and bitcoin after assuming flat price changes for the latter during the weekend

We first notice that, as expected, the 120-day moving average price of SPY ETF changed from 274.204 to 278.524 due to the inclusion of flat weekend days. Then we also notice that the last value of the correlation is positive and close to +0.1 as opposed to near -0.15 in the previous case. The average 120-day correlation is close to 0.

The minimum and maximum 120-day correlation did not change much with the latter also occurring in the beginning of this year.

Next we look at a different example, the correlation between GLD ETF and bitcoin:

- Synchronize bitcoin to GLD by removing weekend trading

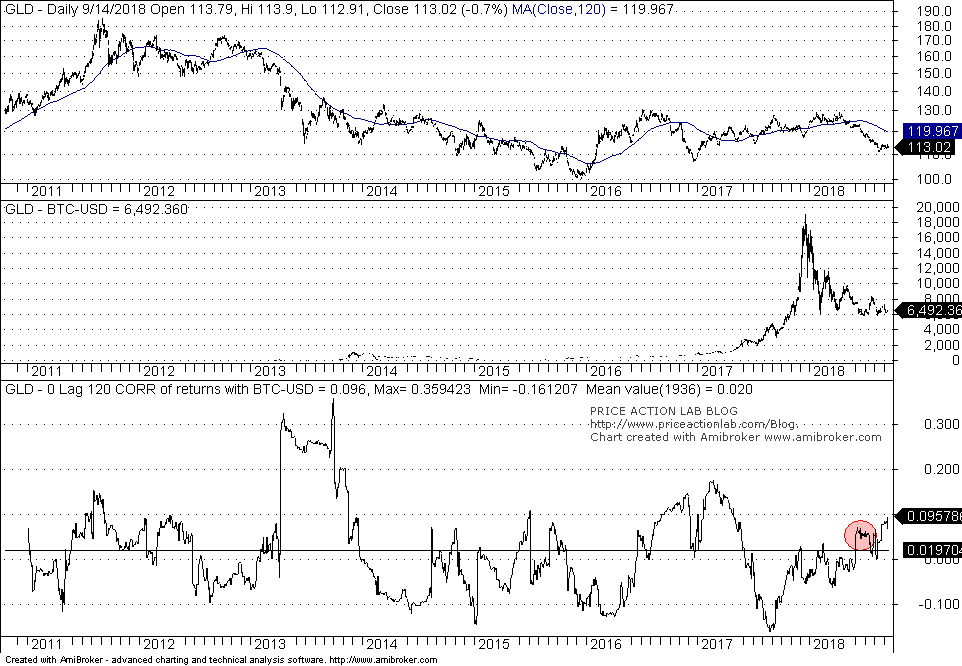

The 0-lag, 120-day correlation of simple returns between GLD ETF and bitcoin after removing price changes during the weekend is shown below:

Figure 3. 0-lag, 120-day correlation of simple returns between GLD ETF and bitcoin after removing price changes during the weekend

Note that the correlation during July of this year was about +0.06, as marked on the above chart. Also, the 120-day moving average of GLD is 119.967.

2. Synchronize GLD to bitcoin by assuming flat prices during the weekend

The 0-lag, 120-day correlation of simple returns between GLD ETF and bitcoin after assuming flat price changes for the latter during the weekend is shown below:

Figure 4. 0-lag, 120-day correlation of simple returns between GLD ETF and bitcoin after assuming flat price changes for the latter during the weekend

As expected the 120-day moving average of GLD changed due to inclusion of weekend flat prices from 119.967 to 118.38. The correlation during July of this year rose near about +0.2. This is different from the near 0 correlation obtained when adjusting bitcoin prices by removing weekend trading.

Conclusion

With two examples we demonstrated how correlations change depending on how one treats the synchronization problem between bitcoin that trades 7 days a week and traditional markets that are closed during the weekend. It is naive to talk about correlations between the new cryptocurrency markets and traditional assets without considering this and other issues discussed in the article that include limited samples and high volatility. If fact, due to these issues we are compelled to conclude that these traditional statistical measures have limited significance in the case of cryptocurrency markets and any decision to invest in them is purely based on instinct and subjective probabilities rather than on quantitative analysis. In other words, when speculation becomes extreme, the usefulness of statistics under small samples is very limited.

If you found this article interesting, I invite you follow this blog via any of the methods below.

Subscribe via RSS or Email, or follow us on Twitter

If you have any questions or comments, happy to connect on Twitter: @mikeharrisNY

Charting and backtesting program: Amibroker

Technical and quantitative analysis of Dow-30 stocks and 30 popular ETFs is included in our Weekly Premium Report. Market signals from systematic strategies are offered in our premium Market Signals service.