Bonds have not underperformed stocks in the last 20 years. This frequent claim of underperformance of bonds is due to comparing apples and oranges.

There is a widespread notion in finance that bonds have underperformed stocks. The relative performance chart of SPY and TLT since the inception of the latter to 02/22/2021 appears to confirm that.

Total return for SPY is 550.5% while for TLT it is about half of that around 229%. This seems like serious underperformance.

But does it make sense to compare performance of bonds and stocks using just a relative return chart? Doesn’t it make sense to also take into account relative risk?

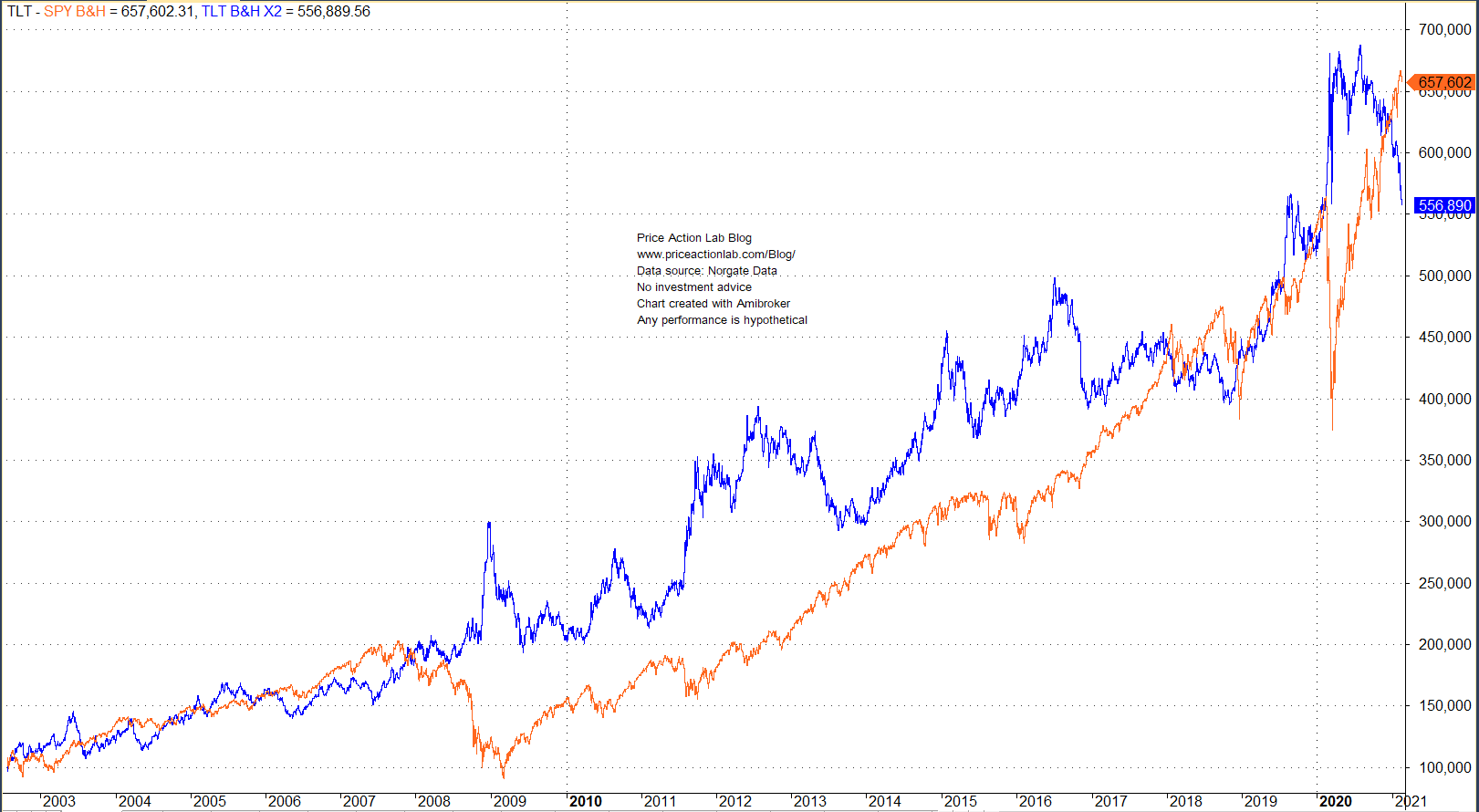

Given the maximum drawdown of SPY in the relative performance period in above chart is 55% but for TLT it is about half of that close to 27%, it makes sense that the total return has also the same ratio of about two. What about if we leverage the investment in bonds time two? Below is a chart of equity performance with $100K starting capital.

Now we see that bonds have mostly outperformed stocks except recently after the unusual rally that followed the crash of last year. Below is a performance table.

| SPY | TLT | TLT X2 | |

| CAGR | 10.7% | 6.6% | 9.7% |

| Total Return | 550.5% | 228.8% | 456.0% |

| MDD | -55% | -27% | -36% |

| Sharpe | 0.55 | 0.48 | 0.50 |

The above results indicate that additional leverage for TLT could even lead to outperformance. However, market regimes matter and forward performance may not agree with these claims. For example, master accounts of CTAs going back to 20 years show high performance on the average but actual customer accounts from the last ten years may show dismal results. Nevertheless, in my opinion, claims of relative performance make sense only when there are adjusted for risk. When that is done in the case of stocks and bonds, the latter take the lead.

Note that leveraging bonds may not work well in the case of 60/40 portfolios since the objective there is to diversify risk. But the leverage may make sense in the case of pension funds and insurance portfolios that seek to match cash flows from bonds to liabilities. Leverage can provide higher total return and increased cashflows while sensitivity to interest rates may be immunized with futures or swaps.

In general, making comparisons in finance is not easy and results may depend on objectives, risk profiles, etc. But in the case of total return performance, it may make sense to consider risk adjustments for the assets involved.

Charting and backtesting program: Amibroker

Data provider: Norgate Data

If you found this article interesting, you may follow this blog via push notifications, RSS or Email, or in Twitter

Click here to subscribe