The battle for irrelevant market statistics reporting in mainstream financial media and blogs adds no value to investors and traders but only generates clicks and website traffic. Most professionals who are humbled by the markets feel embarrassed to report daily statistics of any sort except if they are quite extreme.

There are many financial media sites that rush to report daily changes in the markets and other trivial statistics in ways that appear to be significant.

There are also those who are bit more advanced in working with noise and use backtesting to link some statistics or random patterns to short-term or even medium-term performance although the samples are low.

An example from yesterday is a daily rise of 2.4% in S&P 500. Numerous articles and messages in social media referred to it as follows:

“Largest daily gain in S&P 500 since November of last year.”

This is an irrelevant statistic and only adds noise to a process with an already very low signal to noise ratio. Professionals and other experienced traders ignore these statistics and many even elect to silence the sources. Unfortunately, some astute ones could not take the noise any longer and deleted their social media accounts with the rest of us missing their important market insights.

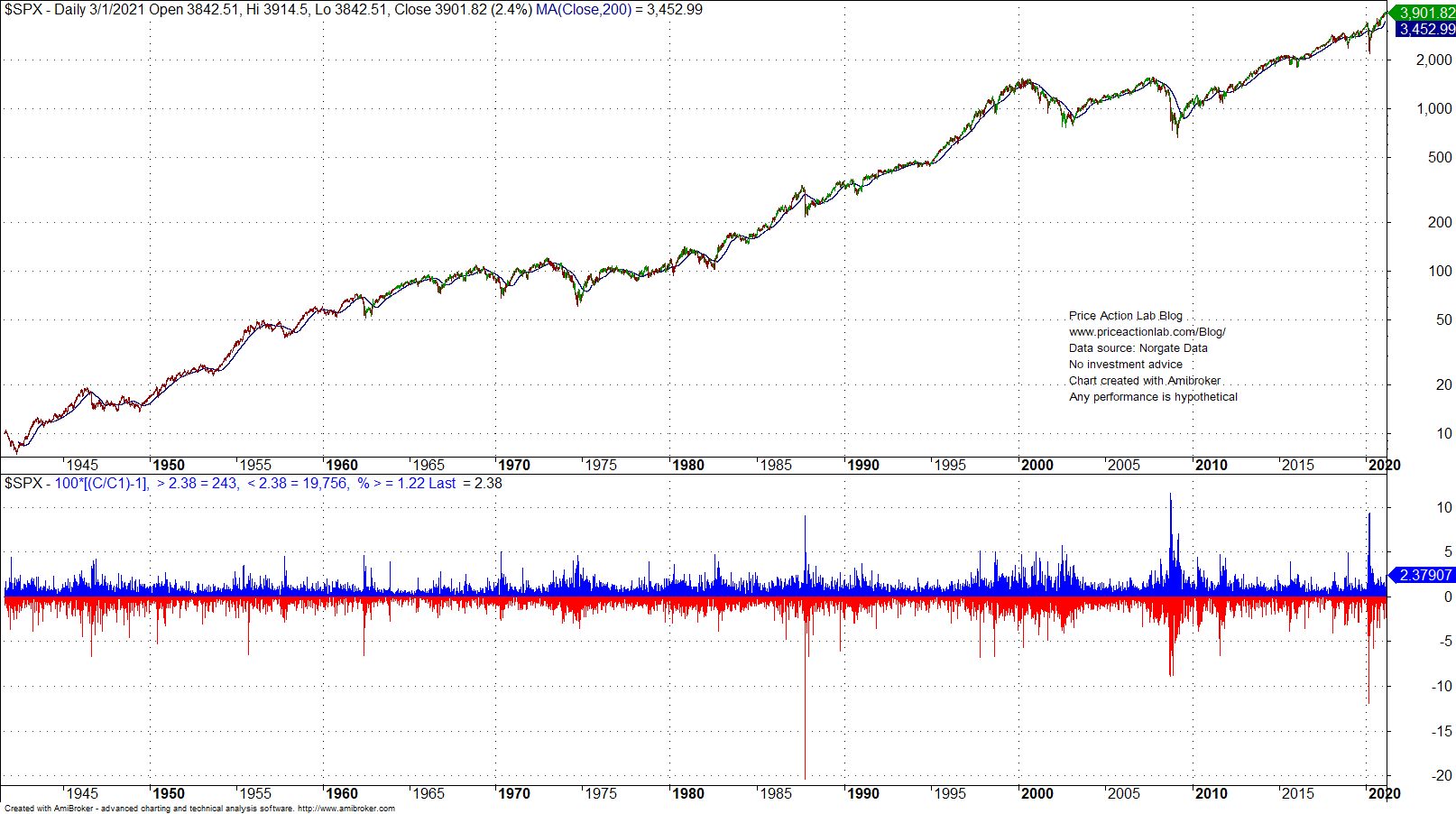

As it may be seen in the chart below, a 2.4% gain in S&P 500 although largest since November of last year has occurred 1.22% of the time since 1941.

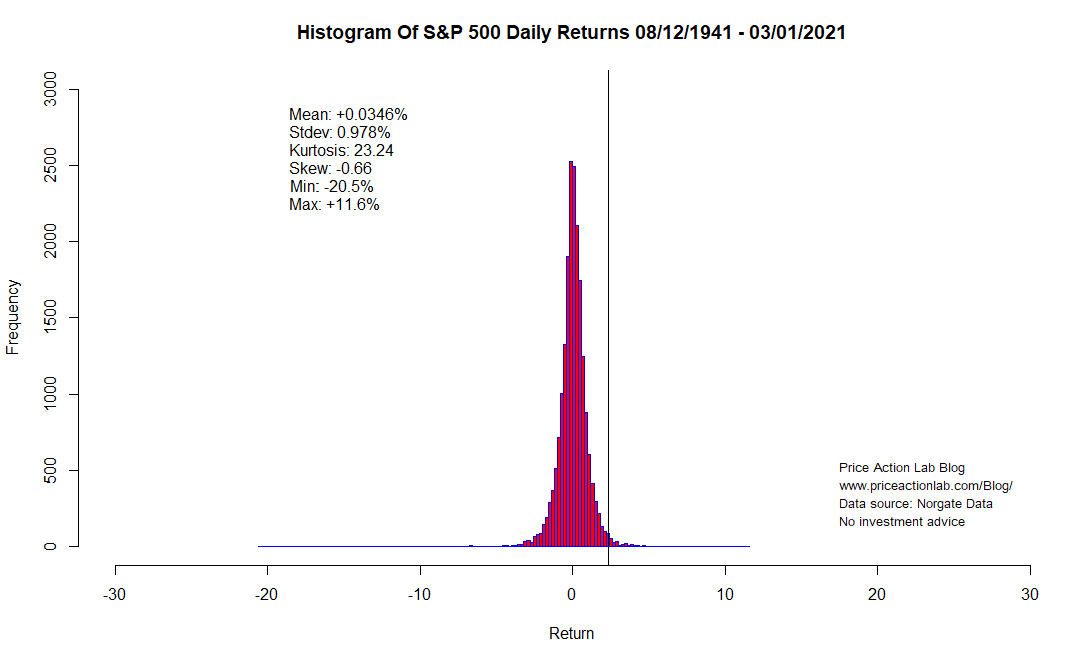

A significant daily gain in a loose statistical sense based on ranking of daily returns would be something like 6% and very far from 2.4%. This may be seen from the histogram of daily returns below.

The vertical line indicates a return of 2.4%. Since the distribution has fat tails, although 2.4% is a large daily return is not significant statistically.

Next, this is an example of naïve backtest:

BUY TLT if it falls more than 1.3 % on a day while SPY rises more than 2.3%

Exit after 20 days.

TLT fell more than 1.3% yesterday while SPY rose more than 2.3%.

Annualized return for this backtest since TLT inception is 2.7% with 63% win rate. But there are only 30 trades and this is far from sufficient sample to determine the probability of a gain for the next trade. In fact, since TLT has been on a longer-term uptrend since inception, a 20-day exit period biases the results. In reality, the backtest reveals the upward bias of TLT in the test period.

If the exit is changed to 3 days, then the annualized return falls to -0.2%. As you may see, this is not a timing system but a longer-term uptrend verification system. Yet, many of these naïve backtests are even presented by some respected blocks as reliable information although they are 100% noise.

Is there a good reason to avoid this kind of noise?

We do not know the longer-term effects of irrelevant information on trader and investor performance. If there is an effect, it will be negative. Therefore, from precautionary principle standpoint, blocking the sources of noise can only be beneficial. Is there possibility of missing some important piece of information then? Actually, by the time information reaches the public it has lost most monetary value. Therefore, blocking sources of noise has no major adverse effects on performance.

Charting and backtesting program: Amibroker

Data provider: Norgate Data

If you found this article interesting, you may follow this blog via push notifications, RSS or Email, or in Twitter

Click here to subscribe