Market timers often believe index passive investing lacks sophistication. While this is true, the decision to passively track indexes could be the result of risk analysis.

Risk in the market manifests itself in many different forms but the two most important for investors and traders are uncle point risk and risk of ruin. In this article, we are concerned about US equity markets only. When referring the index investing, we mean the S&P 500 total return.

The uncle point is based on the risk profile of an individual or fund and refers to a loss that triggers exit from the market. For some investors and traders, uncle point may equate to a 30% loss, and for others to a 60% loss. In the case of funds, the uncle point also varies. In the past, some funds terminated operations after a 30% loss, others continued operating after a 50% loss. The uncle point could be reached because of a random market drawdown or accumulated trading losses.

Ruin occurs when the investor’s or trader’s capital is practically depleted due to a large drawdown or massive accumulated losses. In theory, ruin means 100% loss but in practice, a 90% loss has the same effect. Note that a 90% loss requires a 900% gain to just break even and in most cases, the recovery is considered impossible.

| Risk of Uncle Point | Risk of Ruin | |

| Passive buy and hold | Yes | No |

| Market Timing | Yes | Yes |

We will start with a table and then provide examples. The table compares passive index investing and market timing for uncle point and ruin risks.

According to the above table, passive buy and hold investors face uncle point risk but no risk of ruin. We assume, that the S&P 500 will never fall 90% or more in an environment where the central bank is willing to provide unlimited liquidity. In addition, for comparison purposes, if passive investing is ruined, then all other investing and trading styles in the equity market will also be ruined, including those relying on shorting the market because of counter-party defaults. Therefore, we exclude the catastrophic scenario that is common to all market participants, and although is highly unlikely, it may have some small but finite probability.

Market timing faces both uncle point and ruin risks due to accumulated losses from bad trades. The bad trades could be the result of adverse market conditions, regime changes, or bad risk and money management.

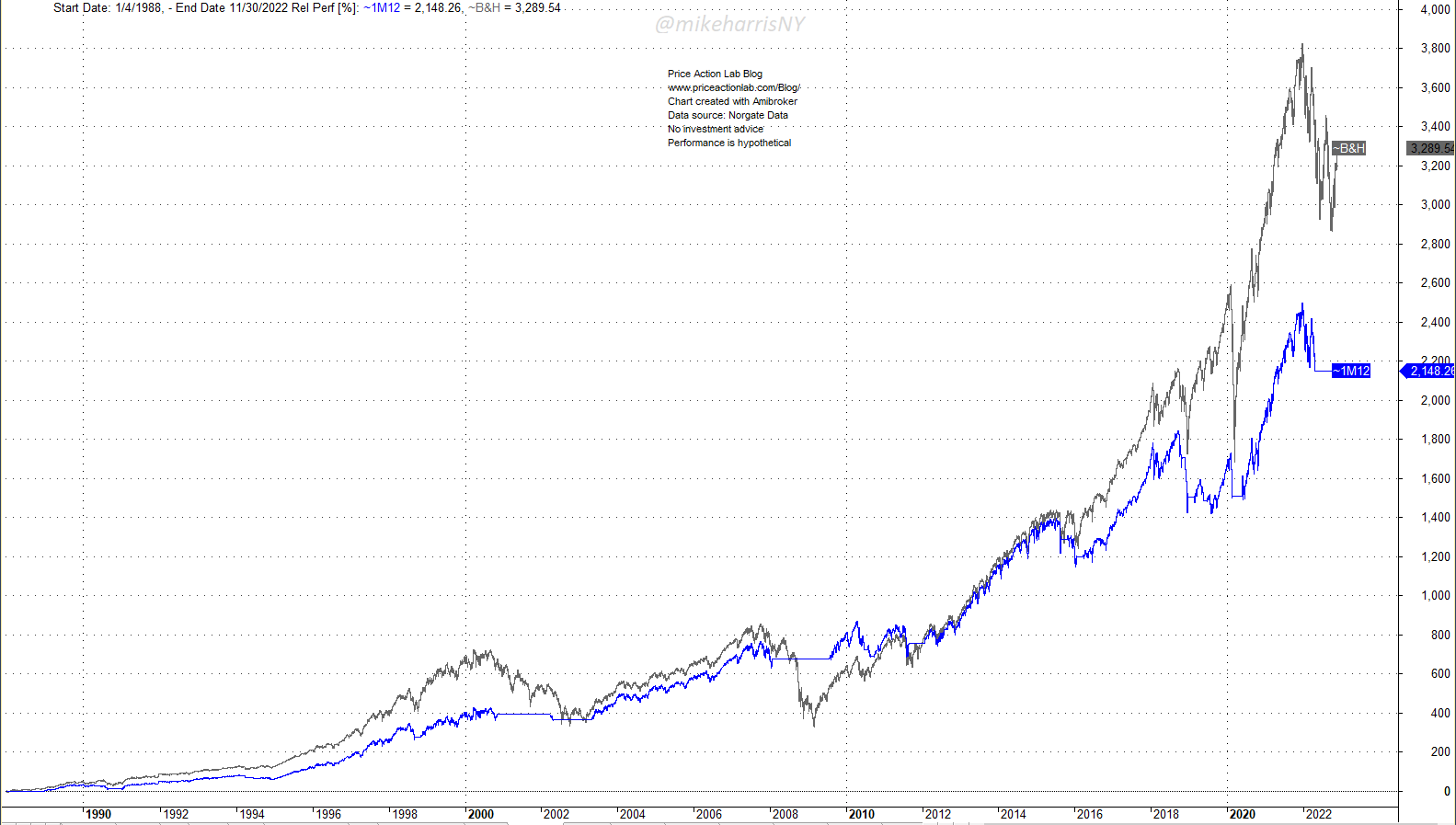

Below we compare the simple price series momentum strategy, which is long the S&P 500 total return when the price is above the 12-month moving average and exits when it falls below the average (1M12), to passive buy and hold (B&H). The period of the relative performance is from 01/04/1988 to 11/30/2022.

The simple market timing strategy (blue line) has limited drawdowns due to bear markets and large corrections but has underperformed passive buy and hold (gray line) by a wide margin. Below are the statistics.

| 1M12 Market Timing | B&H Buy and Hold | |

| Annualized Return | 9.3% | 10.6% |

| Maximum Drawdown | -21.8% | -55.3% |

| Volatility of Equity | 12.5% | 18.1% |

| Sharpe Ratio | 0.74 | 0.59 |

| Number of Trades | 19 | 1 |

| Win Rate | 57.9% | 100% |

The passive buy and hold strategy in S&P 500 total return has outperformed the 1M12 timing strategy annualized return by 130 basis points, but the maximum drawdown is more than double. Some market timers will argue the maximum drawdown reduction and the significant increase in Sharpe ratio from 0.59 to 0.74 for the timing strategy are the justification for abandoning passive buy and hold. However, some important considerations have not been taken into account in papers and blogs. One of those is that market timing, even with simple models such as the1M12, has a risk of ruin due to trading. How can the risk of ruin manifest itself in the US equity markets?

The answer is that in recent times, the US equity markets have not faced an extended period of consolidation or chop. As an example of a possible adverse scenario, we consider what occurred in Emerging Markets from 2010 to 2016. Below is a monthly chart of EEM ETF.

The EEM ETF had a prolonged consolidation in the period marked on the chart. Below is a table that shows how the simple market timing 1M12 long-only strategy and buy and hold have performed.

| 1M12 Market Timing | B&H Buy and Hold | |

| Annualized Return | -4.7% | -0.8% |

| Total Return | -27.4% | -5.6% |

| Sharpe Ratio | -0.31 | -0.04 |

Although passive EEM ETF buy and hold from 2010 to 2016 had a 5.6% loss, the timing strategy lost 27.4%. An even more prolonged consolidation could have caused uncle point or even ruin for market timers using this model. Is this scenario possible in the US stock market?

The scenario is highly unlikely but has a small finite probability. If the probability is small but finite, given enough time, uncle point or even ruin will occur for any timing strategy. However, under this scenario, passive buy and hold will not face large losses.

Any market timing strategy that has a small but finite risk of ruin, will eventually get ruined. The same holds in the case of CTAs who use timing models.

The conclusion is that decision for equity passive index investing may be based on a more sophisticated risk analysis that suggests avoiding timing models. The scenario of a multi-year sideways consolidation in the US stock market that will cause uncle point or even ruin to market timers is extreme but a possibility to consider. Regime switching algos or diversification may not help in avoiding large losses. Passive index investing has risks of uncle point but market timing has in addition risk of ruin, low but finite. Market makers have to deal with the daunting task of eliminating the risk of ruin. The only way to avoid ruin is when the probability of ruin is zero.

Premium Content

Online Books

Premium Articles

Systematic Market Signals

By subscribing you have immediate access to hundreds of articles. Premium Articles subscribers have immediate access to more than two hundred articles and All in One subscribers have access to all premium articles, books, premium insights, and market signals content.

Free Book

Subscribe for free notifications of new posts and updates from the Price Action Lab Blog and receive a PDF of the book “Profitability and Systematic Trading” (Wiley, 2008) free of charge.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data