As the number of markets increases, the Sharpe ratio of profitable trend-following strategies tends to increase due to decreasing volatility. Trading in many markets is essentially a Sharpe maximization strategy.

Some trend-followers argue that trading many markets allows them to catch many more outlier trades. While this is true, increasing the number of markets comes at the price of lowering the impact of outliers on equity growth due to the spreading of risk.

Although it seems obvious, many people contest the fact that trading more markets with a profitable strategy under capitalization constraints frequently results in higher risk-adjusted returns.

In essence, trading many markets is a Sharpe maximization strategy, although some trend-followers question the importance of this performance metric. In some cases, this is done for marketing reasons, since the Sharpe ratio of typical trend-following programs is about the same as that of equity indexes. For example, since 2000, the Sharpe ratio of the SG Trend index is 0.45 versus 0.34 for the S&P 500 total return. While the SG Trend Index has a higher Sharpe in this period, it is nevertheless quite low. At the same time, the total return in the period considered (01/03/2000–09/15/2023) is 290% for the SG Trend Index and 372% for the S&P 500 total return, which translates to a substantial difference.

It may be best to illustrate how adding more markets to trade impacts performance with a simple trend-following strategy. We consider a long-only 100-day breakout strategy for entry and exit for trading S&P 500 stocks. The positions are sized based on ATR, and position risk is allocated equally among the stocks at the time of entry. Our objective is not to evaluate the merits of the strategy but to study how increasing the number of traded stocks impacts its performance. We will vary the number of traded stocks from 10 to 400 in increments of 10. The backtest range is from January 3, 2000, to September 15, 2023. We did not include transaction costs or the impact of slippage.

For the backtests in this article, we used Norgate EOD data that includes current and past constituents (delisted series). We recommend this data service for analysis when the impact of index rebalancing must be taken into account to remove survivorship bias. (We do not have a referral arrangement with the company.)

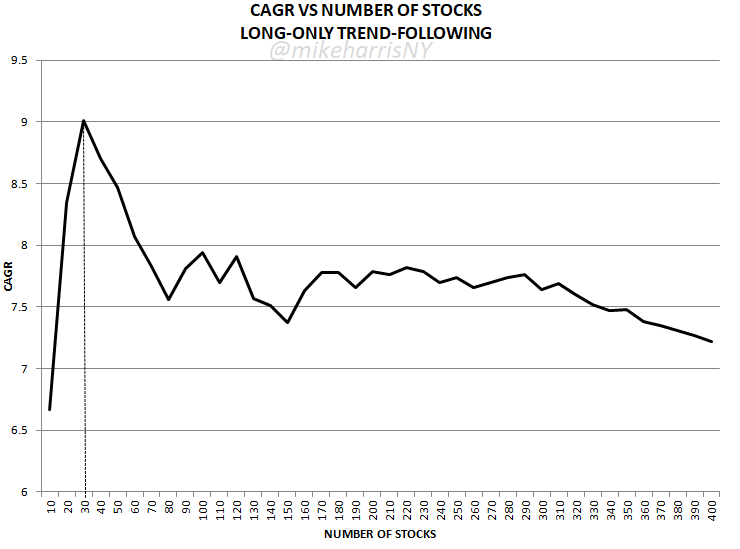

The CAGR peaks at around 9% for 30 stocks and then falls sharply and remains between 8 and 7.5% up to 350 stocks, while afterward, it starts decreasing again. This behavior is what we expected for the classical trend-following with one entry and one exit. As the number of stocks increases, the impact of outliers becomes more uniform, and equity growth is reduced.

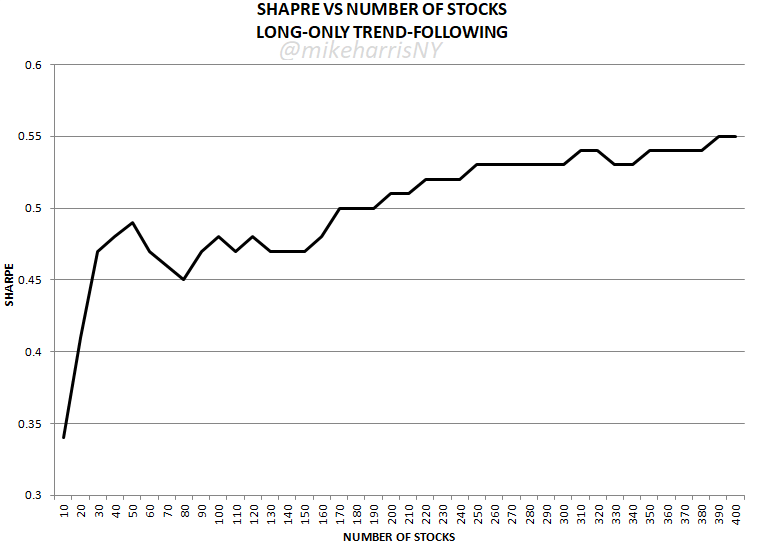

Sharpe Vs. Number of Stocks

The Sharpe ratio makes a local peak near 0.5 at around 50 stocks, then fluctuates between 0.5 and 0.45 between 60 and 170 stocks, and afterward starts increasing linearly. For a maximum of 400 stocks, the Sharpe ratio is about 0.55.

Is there a sweet spot for the number of stocks?

In the case of this particular trend-following strategy, the sweet spot seems to be between 30 and 100 stocks before the CAGR-Sharpe trade-off intensifies.

In other words, trading many stocks is a Sharpe maximization strategy that trades off returns and volatility: trading more stocks lowers the volatility but increases the Sharpe ratio.

Can we get around the trade-off?

It is possible to get around the CAGR-Sharpe trade-off by implementing dynamic stops and rebalancing based on the signal or trend strength of the positions. However, besides the risk of introducing overfitting in backtests, this method can increase tail risk due to concentrated risk. It is possible that some CTAs that outperform their peers by a wide margin use some form of risk adjustment for profitable positions. However, this is probably done at higher risk.

Summary

Trading many markets to catch outlier trades is a Sharpe maximization strategy. It may be suitable for funds with large AUM that aim to primarily preserve wealth and avoid liquidity constraints, but it is highly unlikely such an approach will ever maximize equity growth. Therefore, trading many markets depends on objectives and constraints, but it is not an optimal strategy in general.

Free Book

Get a free PDF of the book “Profitability and Systematic Trading” (Wiley, 2008) by subscribing to the Price Action Lab blog’s free email notifications of new posts and updates.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS, Email, or Twitter