There is a recurring theme in the financial mainstream media about market timing being ineffective because a small number of large returns drive stock market performance. The conclusion is disconnected from the facts.

Summary

Market timing is often argued to be ineffective due to the small number of large daily returns driving stock market performance. However, quant analysts know that the bulk of large returns in the stock market have been due to reflex rallies during large corrections. This is important because passive investors may hit the “uncle point” and exit the market before these large returns are realized. The majority of returns occur while the market is in a large drawdown, and the paradox is that for investors to realize the market total return, they should be willing to withstand large drawdowns where the large returns the financial media and passive indexing advertise often appear. Market timing has been under attack by academics and the passive indexing industry, but it has worked so far.

The claim

The claim was repeated yesterday in mainstream financial media, with the conclusion that indexing only works for investors.

However, quant analysts know that the bulk of large returns in the stock market have been due to reflex rallies during large corrections.

What does this matter? It matters because passive investors may hit the “uncle point”, especially those who are close to retirement, and exit the market before these large returns are even realized.

Let us look at specific statistics below.

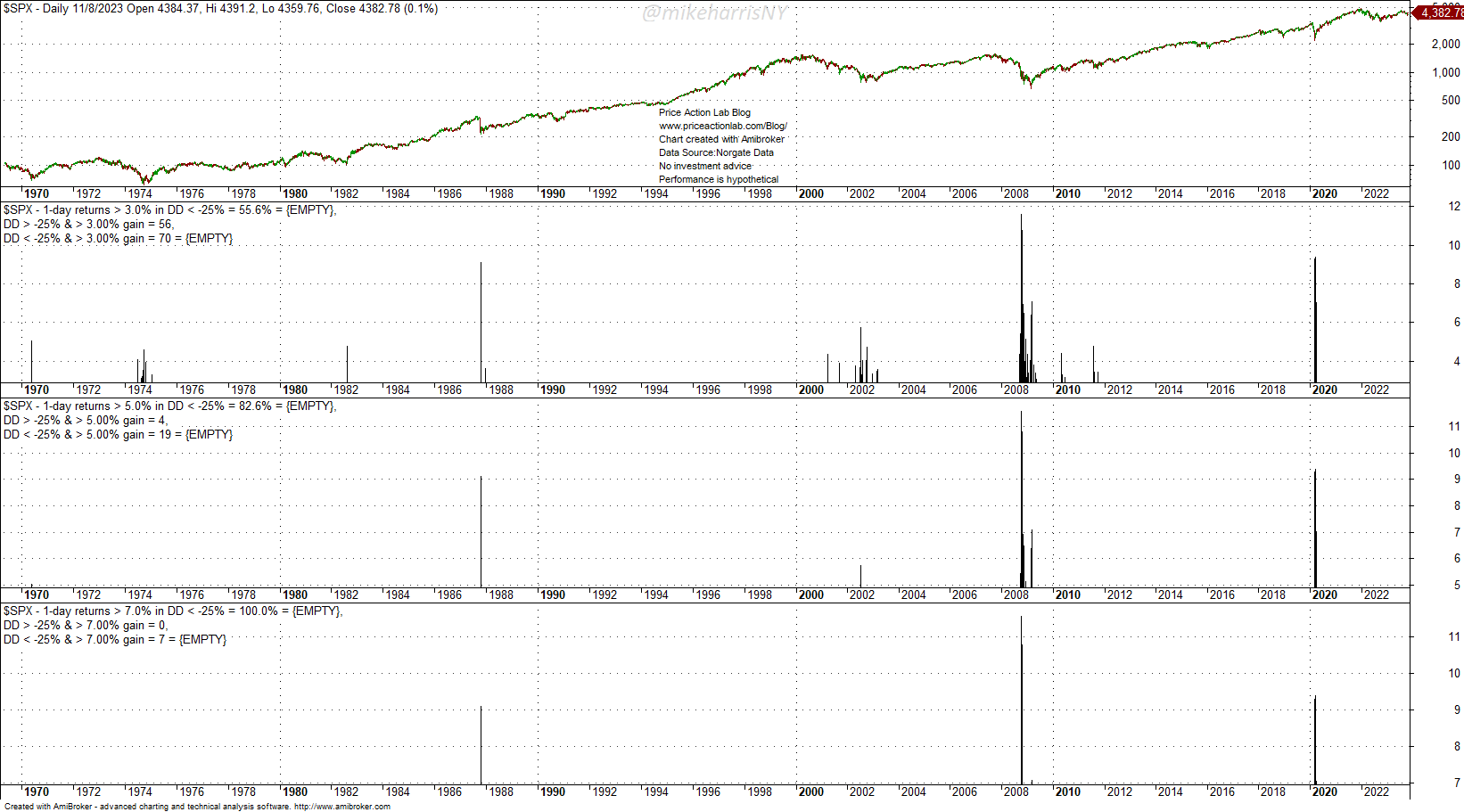

The chart shows +2%, +5%, and +7% daily returns that have occurred while the S&P 500 was in a 25% or larger drawdown. Below is a summary table.

| Daily Returns | Drawdown > 25% | Drawdown < 25% |

| > +3% | 70 | 56 |

| > +5% | 19 | 4 |

| > +7% | 7 | 0 |

The overwhelming majority of the returns, as they get larger, occur while the market is in a large drawdown. For example, there have been 23 returns larger than 5%, and 19 have occurred while the market was 25% or more below all-time highs. In the case of 7% of larger returns, all have occurred while the markets were 25% or more below all-time highs.

The hidden paradox is that for investors to realize a large total return, they should be willing to withstand large drawdowns where those large returns the financial media and passive indexing advertise often appear.

There must be a better way

There must be a better way, and there is. It is called market timing and has been under attack by academics and the passive indexing industry for years. Here is one of the simplest examples.

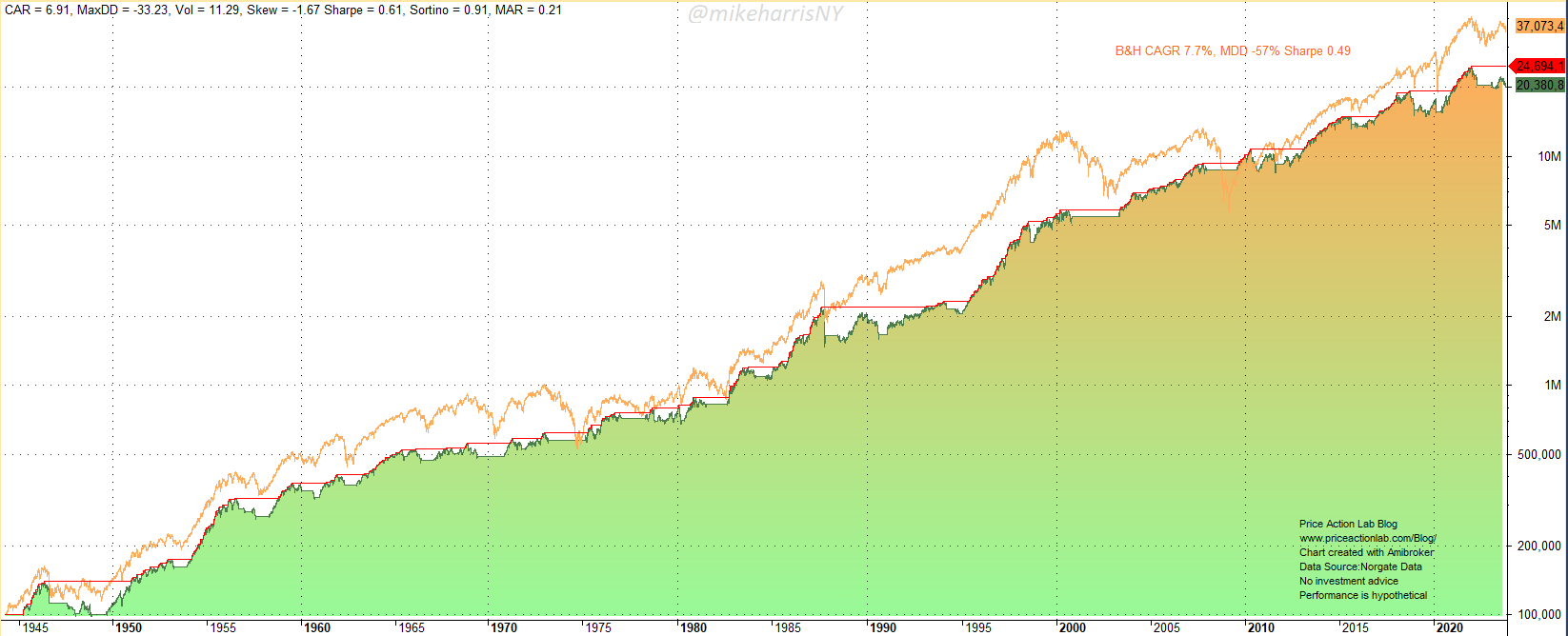

The strategy involves staying invested in the market as long as the S&P 500 index is above the 12-month moving average and exiting when it falls below it.

There is no alpha in this strategy, but it has avoided a few large corrections, while the maximum drawdown is 33.2% versus 57% for buy and hold. The Sharpe ratio increases from 0.499 to 0.61. The strategy trades off annualized returns for better risk-adjusted returns. Simple timing is the key to achieving this.

Many other strategies can be used for market timing, some based on moving averages and others based on the cross-sectional momentum of several assets to achieve diversification. Then, there are long/short beta-neutral strategies and, of course, trend-following CTA strategies that are known to even provide convexity during equity bear markets.

Summary

The argument that market timing is not possible because the total return depends on a small fraction of returns is an artificial image to attack. Most investors will gladly trade off their annualized return for peace of mind by staying out of the market during periods of high volatility and drawdowns. There are also the gamblers who want to maximize returns by risking uncle point. These are personal preferences about risk, but the point is that market timing works, or at least has worked until now.

Price Action Lab Blog Premium Content

Subscribe for immediate access to hundreds of articles. Premium Articles subscribers have immediate access to more than two hundred articles, and All in One subscribers have access to all premium articles, books, premium insights, and market signal content.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS, Email, or Twitter.