This is a state-of-the-art market neutral long/short equity strategy based on the Dow stocks. Signals are generated after the close of each trading day and profit calculations are based on the change from the open and close of the next day. The strategy uses alpha factors calculated daily by a machine learning algorithm.

Market neutral long/short strategies are defined as follows:

Long/short equity strategies involve taking both long and short positions so that a net profit is made while market exposure is minimized. …usually during bull markets long positions tend to be more profitable than short and the other way around during bear markets. Therefore, the profitability of a long/short strategy does not depend on market direction. The strategy is called market neutral when allocations to long and short positions are equal.

A long/short equity strategy was presented in this article. In this article the strategy is in addition market neutral since at the close of each trading day three long and three short signals of equal position size are generated based on machine-designed alpha factors, also known as features, attributes or predictors in machine learning.

Generation of historical alpha factor values for backtesting

The historical values are generated by DLPAL LS, an institutional grade version of DLPAL software.

DLPAL LS takes the original historical data files of the stocks as input and creates new files with extension .pih that include the alpha factor values for each instance (row). An example is shown below for AAPL.

Using the historical alpha factor files

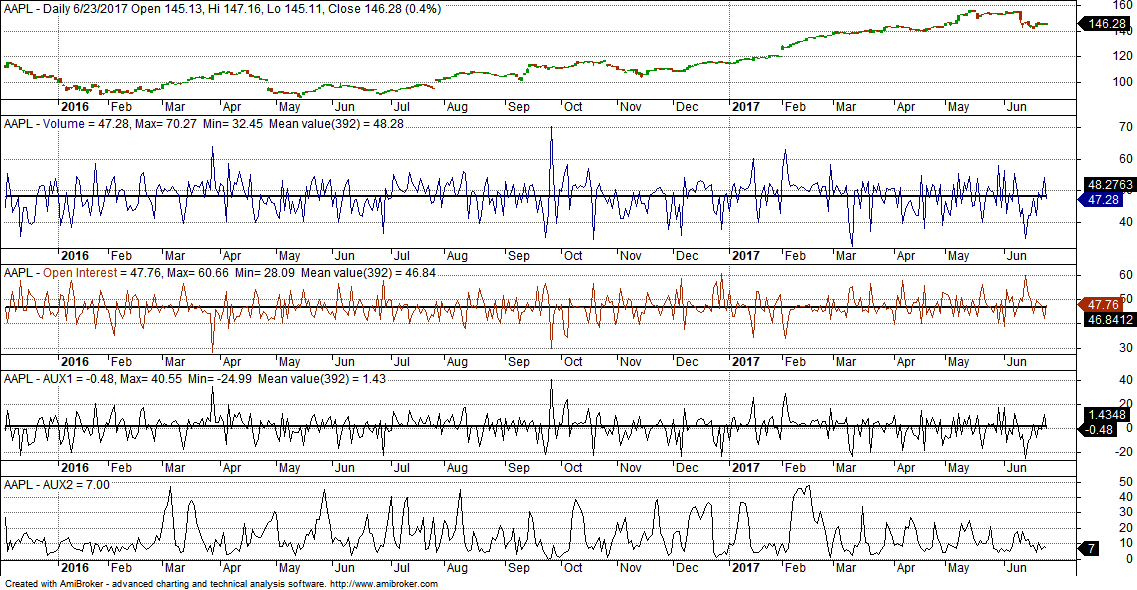

The generated .pih files for each stock are imported in a trading platform. We use Amibroker because of the ease of importing historical data with additional fields. The four indicators are imported as follows: PLong is assigned to Volume, PShort is assigned to Open Interest, Pdelta is assigned to AUX1 and S to AUX2. A typical chart of the stock with the indicators is shown below.

Strategy specifications

Time-frame: Daily (adjusted data)

Strategy type: Market neutral long/short equity

Universe: All Dow stocks from current composition

Backtest period: 01/04/2016 – 06/23/2017

Alpha factor calculation period: 01/03/2000 – 12/31/2015

Open positions: 3 long and 3 short

Position size per stock: Equity/6

Position entry: Open of next bar

Position exit: Open of next bar

Commission per share: $0.005

Strategy logic

Score: AUX1 × AUX2

Buy the top 3 and short the bottom 3 stocks based on the score at the open of next day

Strategy performance

| Parameter | Strategy |

| Return | 13.3% |

| Max. DD | -6.56% |

| Sharpe | 0.36 |

| MAR | 1.36 |

| Win rate | 50.7% |

| Trades | 1676 |

| Profit factor | 1.11 |

| Payoff ratio | 1.08 |

The strategy has low drawdown of less than 7% and can be leveraged 2x to generate returns in excess of SPY total return of 21.1% in the same period.

Below are the equity curve, underwater equity curve and monthly returns table. (Click on images to enlarge.)

|

|

|

Below is a Monte Carlo simulation graph.

There is less than 5% probability of 10% or higher drawdown according to the simulation. The probability of drawdown exceeding 14.7% is less than 1%.

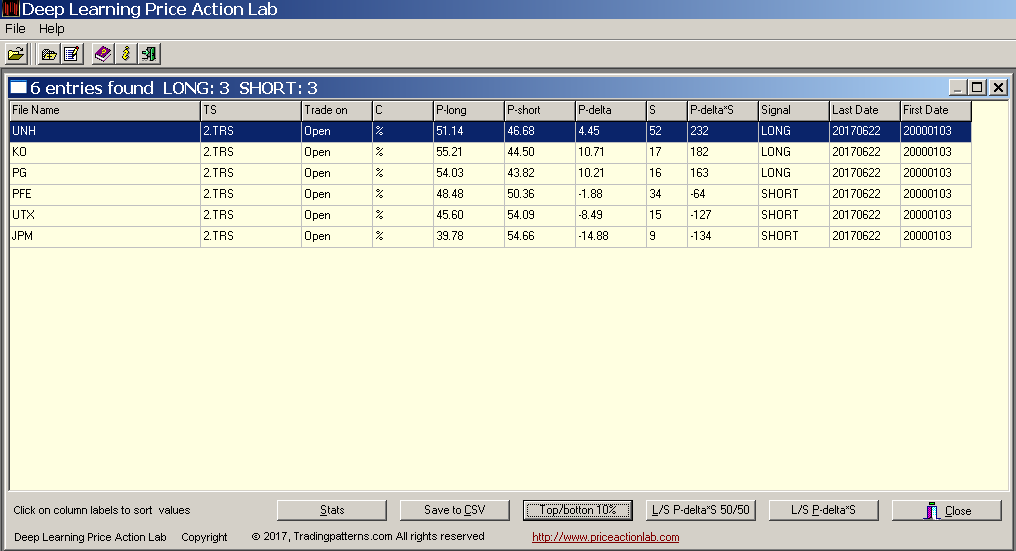

Daily Execution

Daily execution involves updating data files, ranking stocks according to score and then selecting top 3 and bottom 3. This is done in DLPAL LS with a few clicks. An example is shown below:

A CSV file is also generated for use with an API for executing trades automatically through a broker platform.

We can discuss trading this and similar strategies for long/short equity hedge funds or training in-house quants to use DLPAL LS in developing and executing these strategies.

More details about DLPAL LS can be found here. For more articles about DLPAL LS click here.

If you have any questions or comments, happy to connect on Twitter: @priceactionlab

Strategy performance results are hypothetical. Please read the Disclaimer and Terms and Conditions.