We present the results of a strategy that switches to leverage ETFs using a simple market timing method for the purpose of improving SPY buy and hold return.

The strategy considers SPY, SSO (2x) and UPRO (3x) ETFs and switches to the most appropriate one for the purpose of realizing higher risk-adjusted returns as measured by MAR, which is the ratio of CAGR to maximum drawdown.

Strategy: ETF switching

Method: Details will be included in Market Signals next weekly report.

Backtest period: 01/04/2010 – 06/24/2019

Commission: $0.01 per share

Equity: Fully invested.

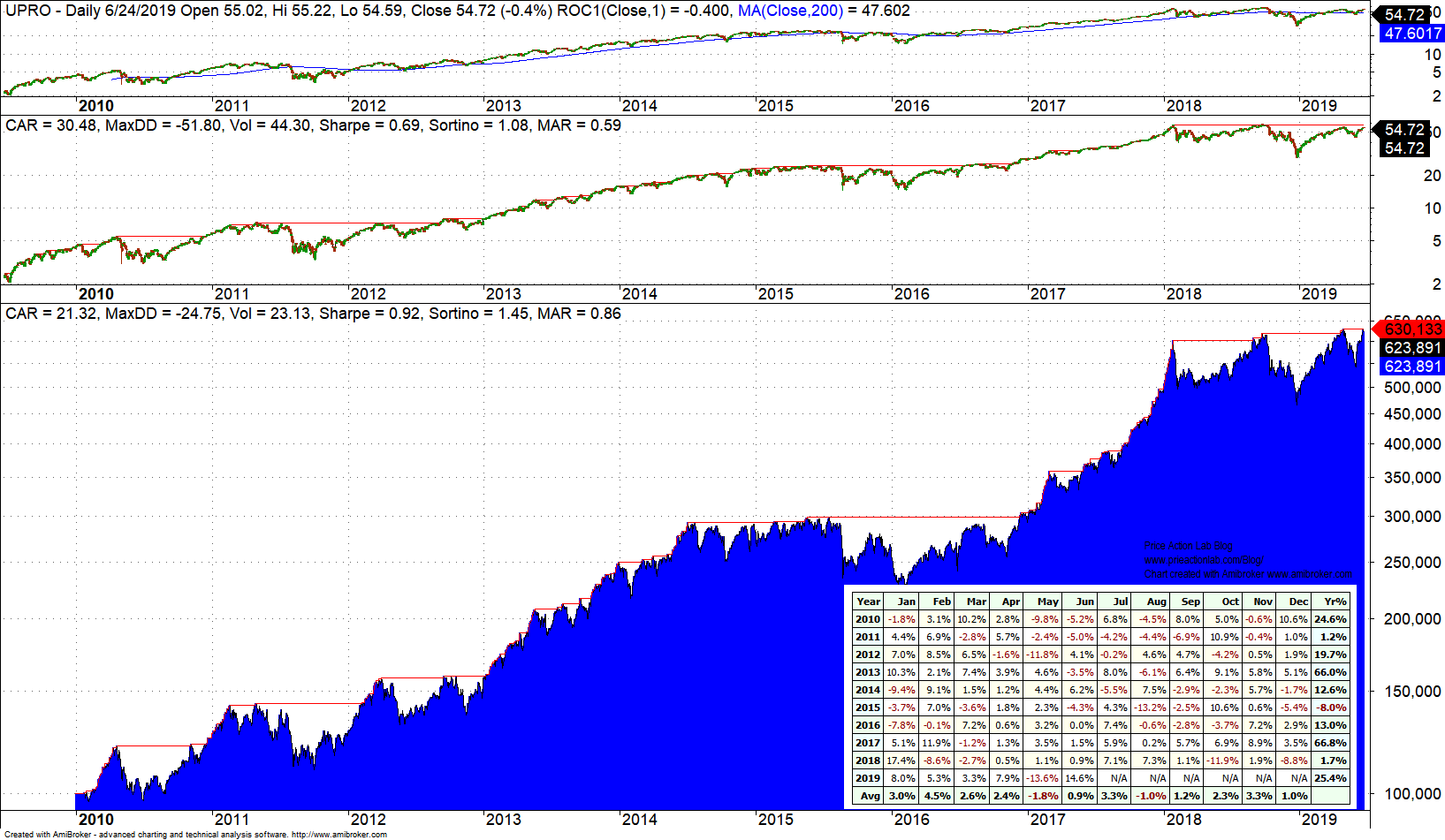

Backtest results

Equity is volatile because in essence this is SPY buy and hold strategy with a tactical overlay for ETF switching. The UPRO buy and hold performance without any switching is shown in middle pane. The bottom pane shows the equity of the strategy and a table of monthly returns. Worst year for the strategy is 2015 with -8% return and best year is 66.8% in 2017. Below is a table that compares key performance metrics.

| SPY | SSO | UPRO | Strategy | |

| CAGR | 12.8% | 21.9% | 30.8% | 26.32% |

| Max. DD | -19.4% | -36.6% | -51.9% | -24.8% |

| Sharpe | 0.87 | 0.74 | 0.69 | 0.92 |

| MAR | 0.66 | 0.60 | 0.59 | 0.86 |

It may be seen from the above table that the switching strategy has the highest Sharpe and MAR. CAGR for the strategy is about the average of the CAGR values for SSO and UPRO buy and hold while the maximum drawdown is less that that of SSO buy and hold. As a result this appears to be a superior strategy given the limitations of backtesting.

The strategy logic will be included in Market Signals next report during the weekend.

If you found this article interesting, I invite you follow this blog via any of the methods below.

Subscribe via RSS or Email, or follow us on Twitter

If you have any questions or comments, happy to connect on Twitter: @mikeharrisNY