We provide in this article three examples of how volatility has affected the performance of trading strategies.

Are there any advantages in trading only when volatility is low? It seems that the answer depends on the details, i.e., strategy type, timeframe, friction, etc. Since trading performance is both path and strategy dependent, it is hard to generalize. It is also dangerous to make any generalizations in trading.

We will only consider strategies in the daily timeframe in this article. All equity curves below are based on backtests and include $0.01/share commission for fully invested capital.

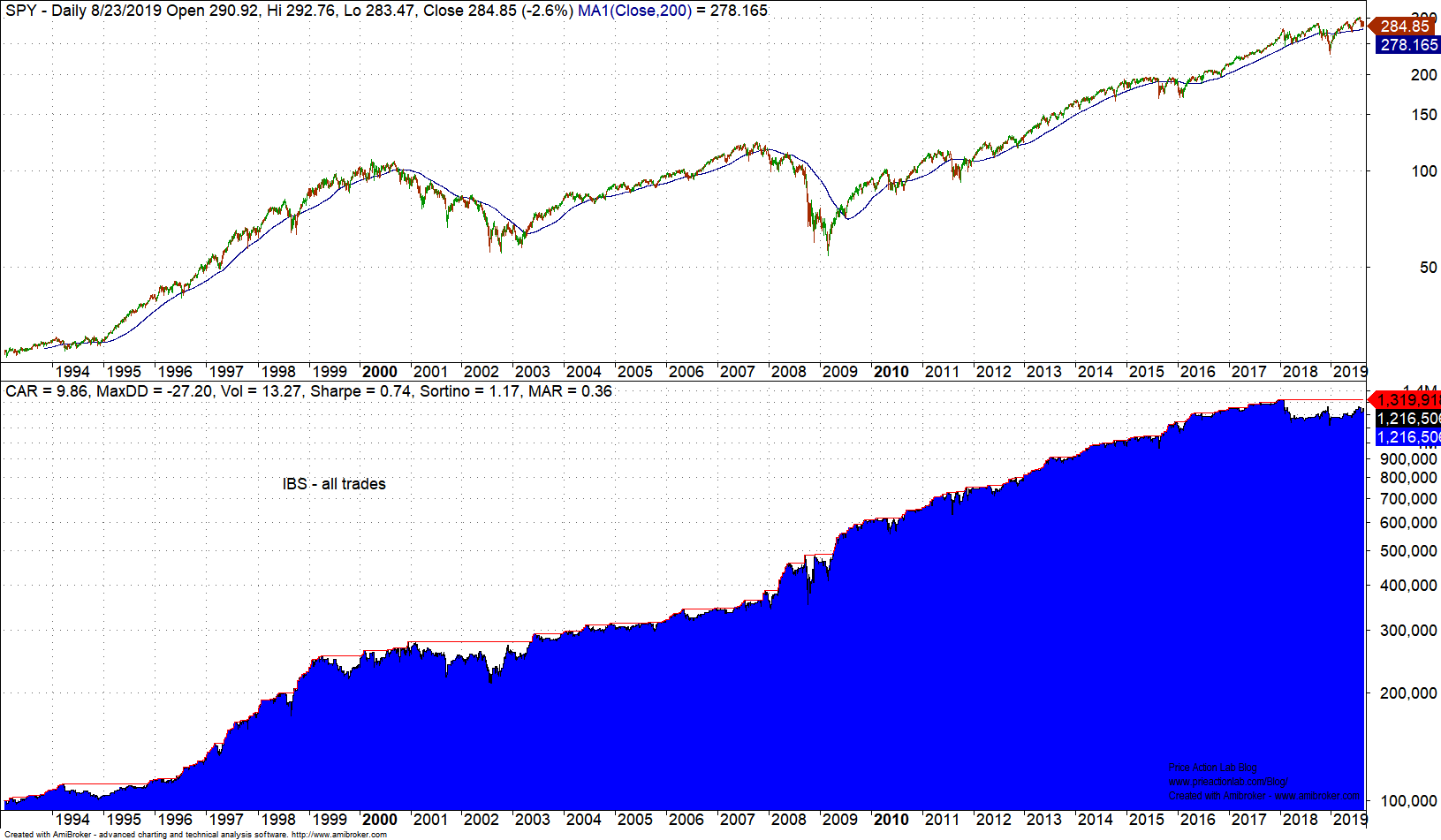

Let us look at the performance of the popular IBS strategy. This strategy trades SPY and has generated a loss of 12% last year although in 2008 and 2011 performance was excellent.

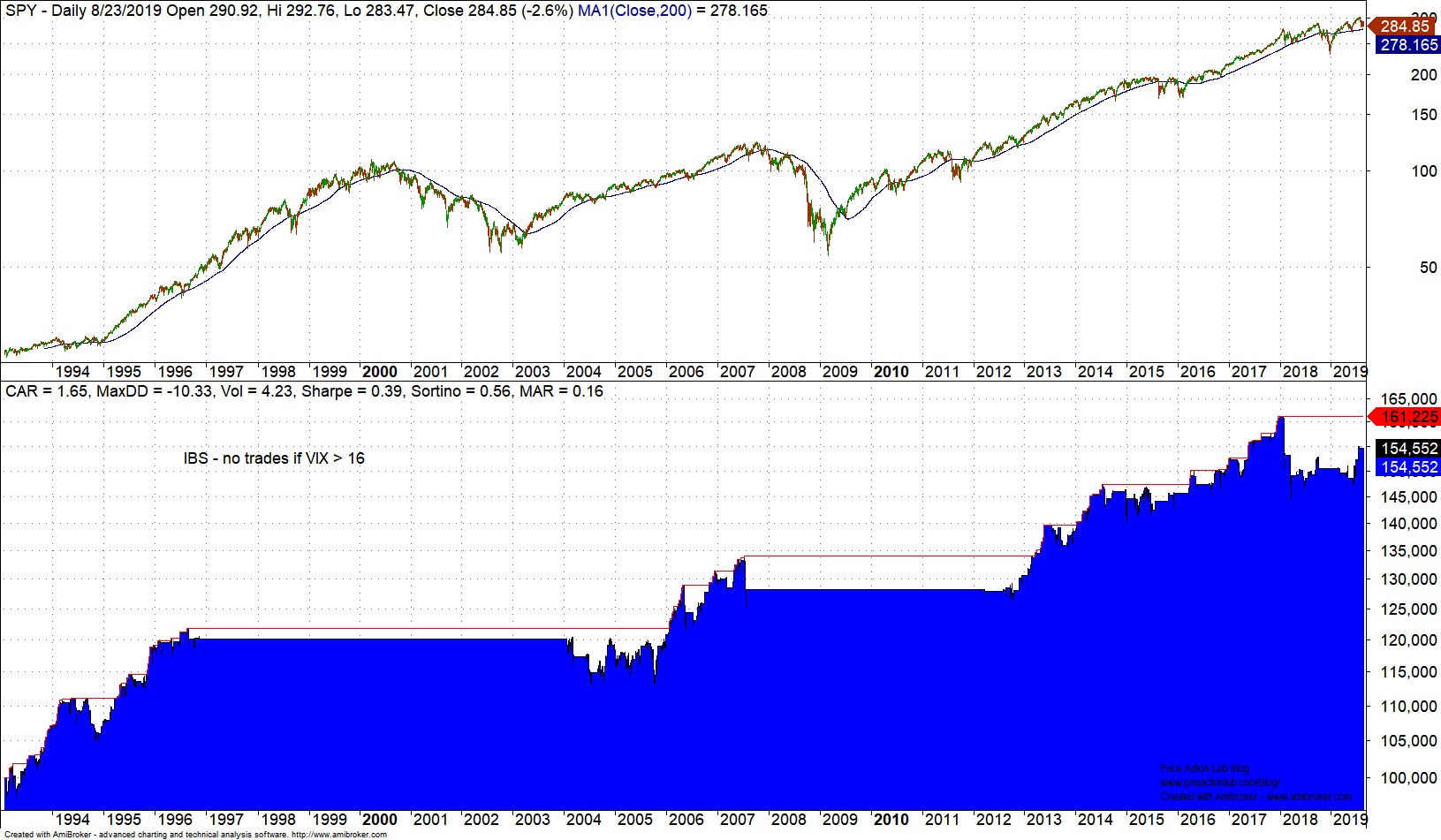

Next we consider only those trades when VIX was less than 16 (a level suggested in social media posts.)

It may be seen that CAGR falls from 9.86% to just 1.65%. It appears then that the bulk of the profits were made historically during higher volatility periods. Maximum drawdown fell from 27.2% to 10.3% but risk-adjusted returns are lower by a factor of 2.25 when we compare MAR.

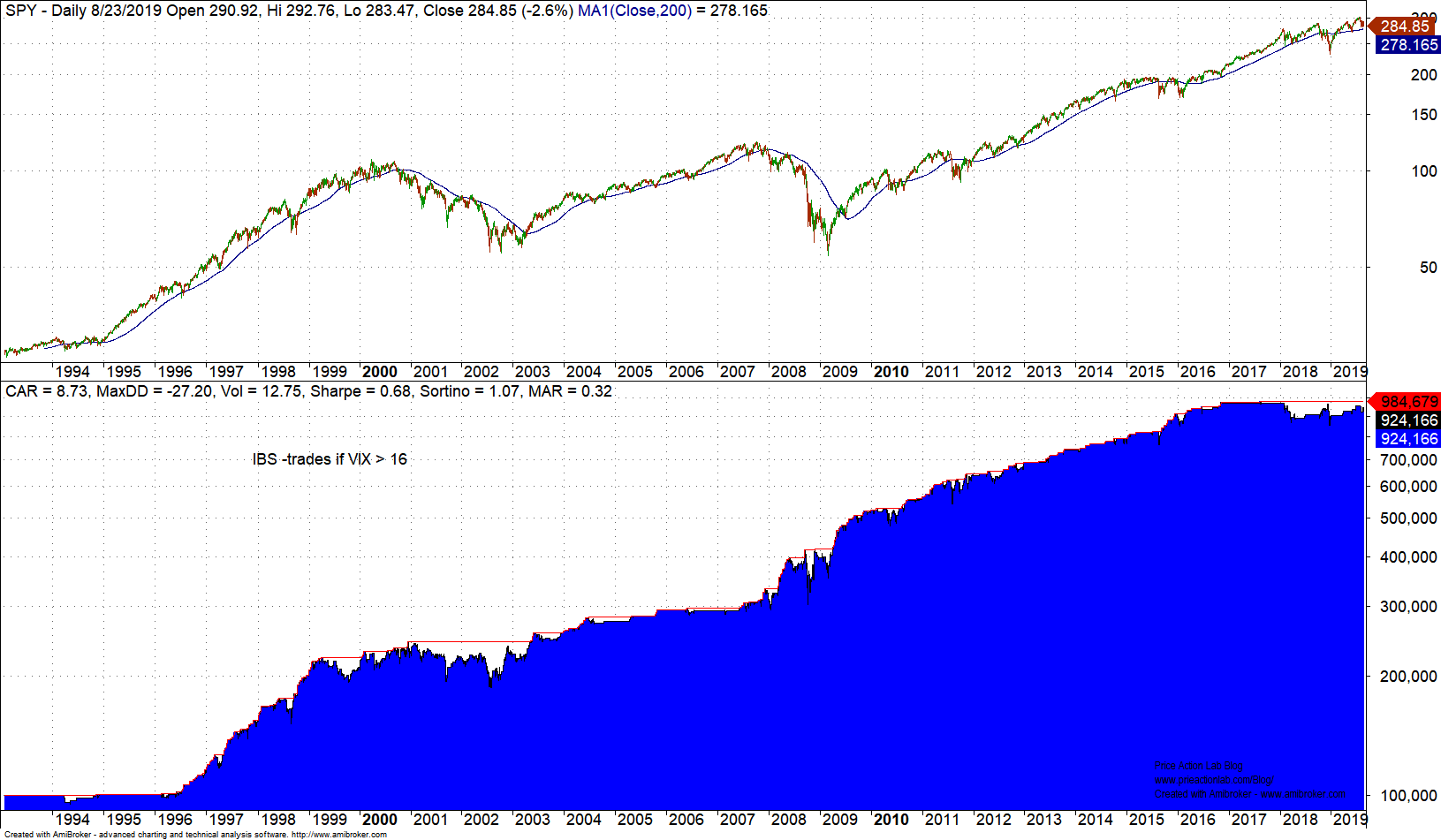

Below is the equity chart of the IBS strategy with trades only when VIX is higher than 16. The results confirm that the bulk of gains came from higher volatility periods.

Maybe this behavior is specific to IBS strategy. Next let us look at the popular RSI2 strategy and also at the PSI5 proprietary strategy. The results for CAGR are shown in the table below. (SPY trading.)

| Strategy | All trades | VIX < 16 trades | VIX > 16 trades |

| RSI2 | 7.0% | 1.6% | 6.2% |

| PSI5 | 8.3% | 2.1% | 7.0% |

We notice similar behavior with those two strategies: the bulk of the profits were generated during higher volatility periods.

Can we draw any general conclusions from this brief analysis? Obviously not. But it makes sense to assume that higher risk offers higher opportunity for profit and the notion that high profits can be realized during low volatility periods is probably the result of recency bias. However, there may be strategies with options and volatility derivatives that benefit most during low volatility periods.

If you found this article interesting, I invite you follow this blog via any of the methods below.

Subscribe via RSS or Email, or follow us on Twitter

If you have any questions or comments, happy to connect on Twitter: @mikeharrisNY

Charting and backtesting program: Amibroker