Bear markets have posed so far no major risks to equity market timing because most models, even the simple ones, have successfully avoided them. But there is a significant source of risk for equity market timing that is rarely discussed. Furthermore, some popular timing strategies may be artifacts of data-mining bias.

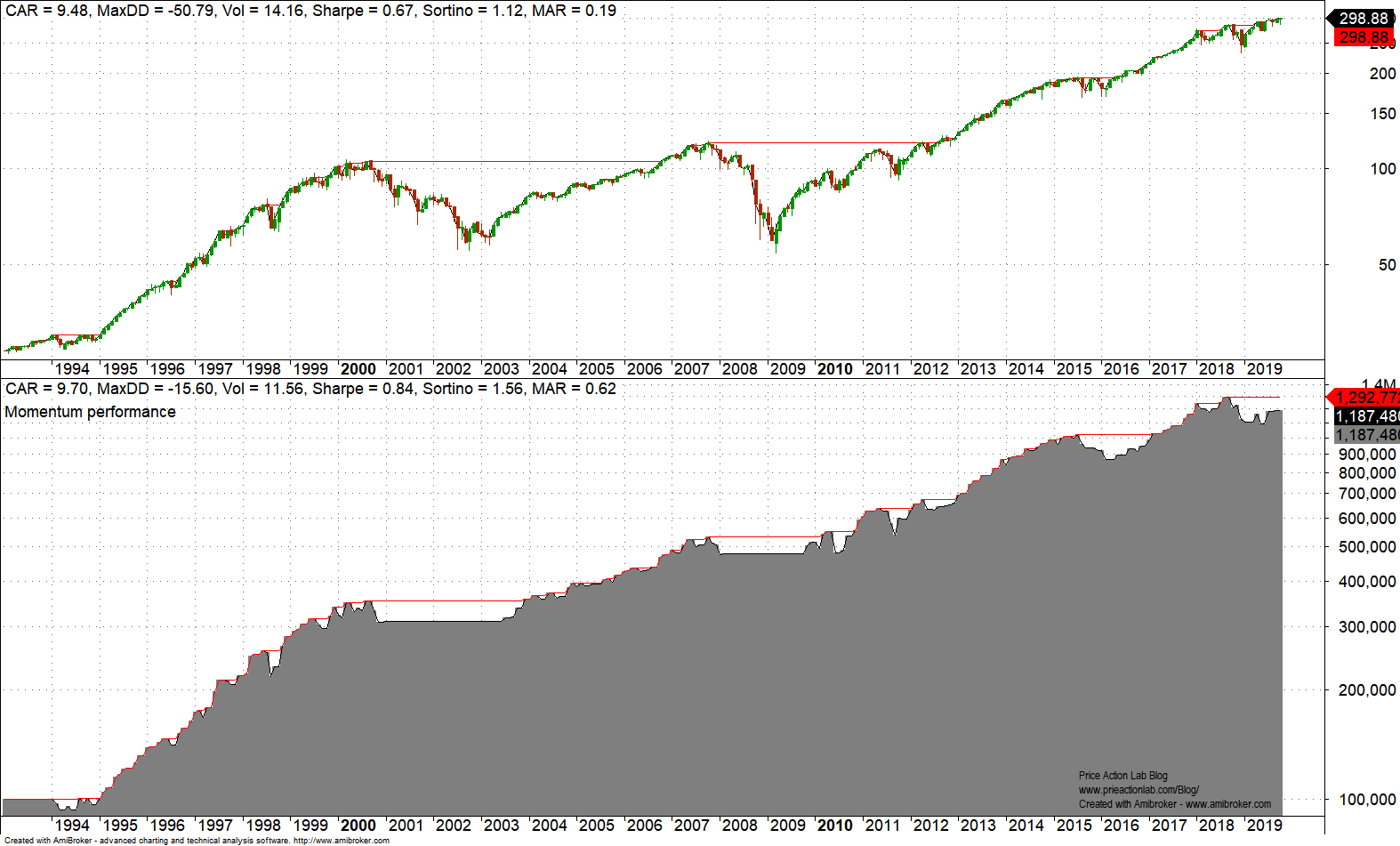

Everyone is impressed by the performance of a simple momentum strategy in SPY ETF since inception that goes long when the 12-month rate-of-change is positive and exits when it turns negative. Below is the equity performance for fully invested equity and $0.01 per share commission. All trades occur at the open of the month following the signal.

CAGR for the simple momentum model is 9.7% versus 9.5% for buy and hold but risk-adjusted performance is significantly higher due to a much smaller maximum drawdown for momentum versus buy and hold, -15.6% versus -50.8%, respectively. This is a substantial improvement that offers hope for the sustainable performance of these strategies. This improvement is made possible by avoiding the two bear markets in 2000-2003 and 2008.

However, it is important to notice that this market has not experienced a prolonged sideways movement. On the contrary, recovery from bear markets has taken place in the form of V-bottoms, as may be seen from the above chart. Therefore, there was never any risk to the momentum strategy due to choppy price action. This is a significant observation that many have missed in articles and books about timing models.

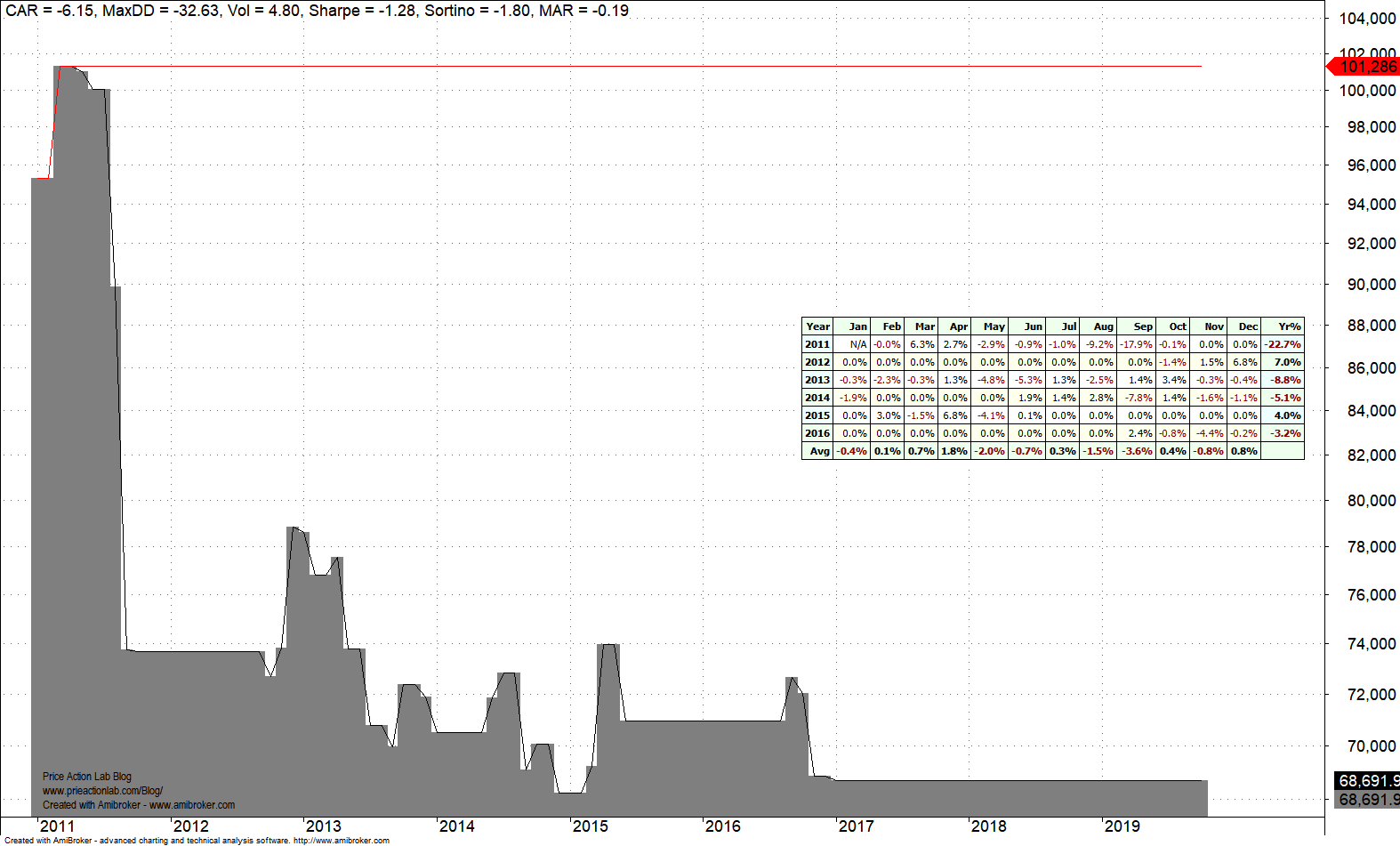

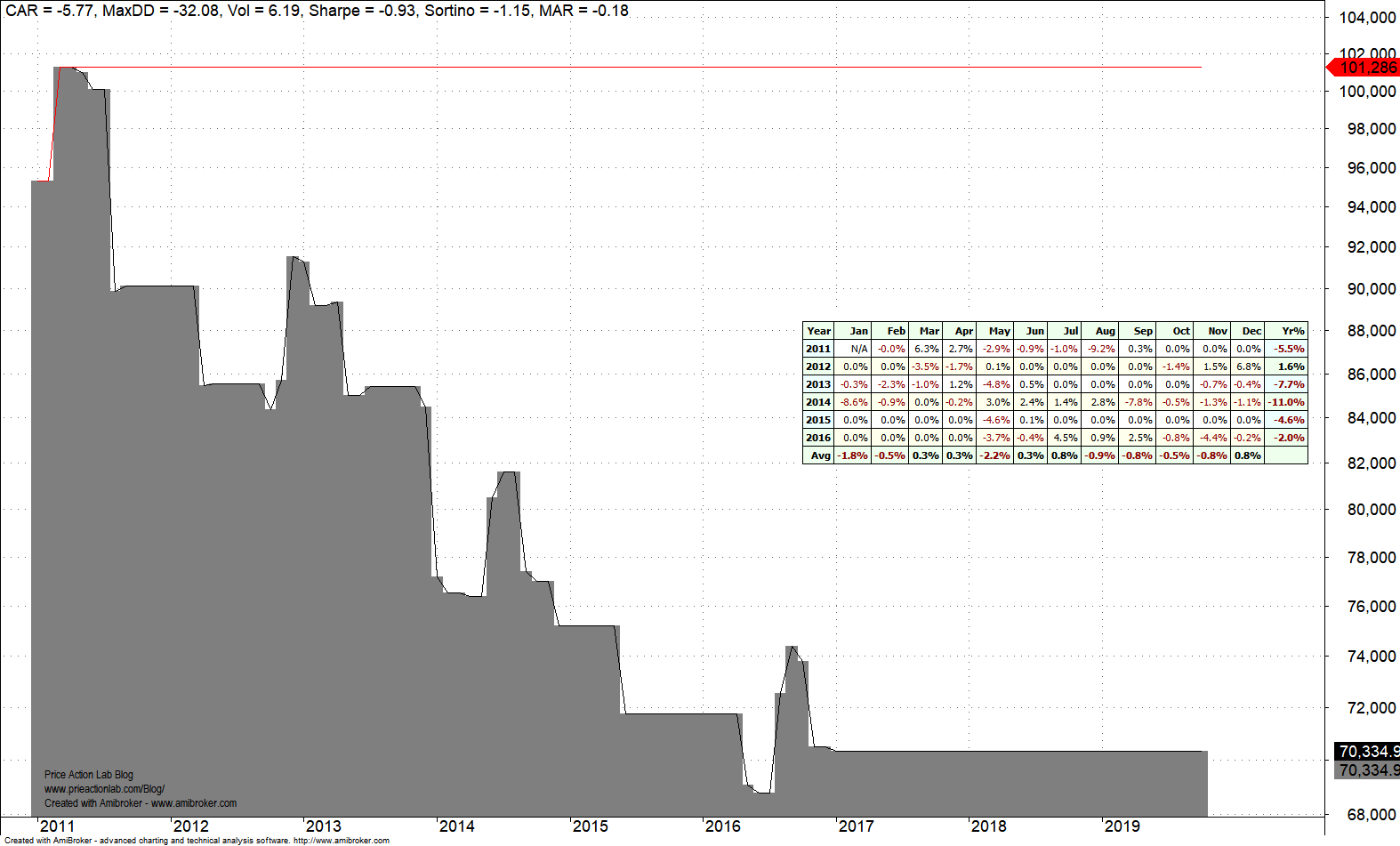

In case of a prolonged sideways market, timing strategies can incur significant losses. To get an idea of the magnitude of the losses, we will backtest a momentum model and a trend-following model in EEM ETF data from 01/2011 to 12/2016, which was a sideways market, as shown in the chart below.

Momentum

We use the 12-month rate-of-change of the closing price.

Buy next open if ROC(C,12) > 0 – Sell next open if ROC(C,12) < 0.

Trend-following

We use a 12-month moving average crossover of the closing price with the price itself.

Buy next open of C > MA(C,12) – Sell next open if C < MA(C,12)

Backtest details

Market: EEM ETF

Backtest period: 01/2011 – 12/2016

Data adjusted for dividends

Timeframe: Monthly

Commissions: $0.01 per share

Equity fully invested

Starting capital is $100K

All signals are for the open of the next monthly bar

Backtest results (Click on images to enlarge)

Momentum

Trend-following

Below is a table with key performance parameters

| Parameter | Momentum | Trend-following |

| CAGR | -6.2% | -5.3% |

| Return | -31.2% | -29.7% |

| Max. DD | -34.4% | -32.1% |

| Sharpe | -1.28 | -0.93 |

| Trades | 7 | 9 |

| Win rate | 43% | 22% |

The performance of both models is significantly negative with trend-following only slightly better. Using these timing models during a prolonged sideways market could be equivalent to passive investing during a bear market, in terms of risk.

Are momentum and trend-following artifacts of data-mining bias?

Popular trend-following and momentum strategies presented in some books and articles as solutions to the market timing problem may be artifacts of data-mining bias due to special conditions in price series that allowed high performance in the past. In case of a major regime change, for example, a prolonged sideways market, these models will be crushed and investors and funds that use them will end up deep in the red. The beneficiaries will be passive investors with more or less flat performance and some algos, including equity long/short.

If you found this article interesting, you may follow this blog via RSS, Email, or Twitter.

If you have any questions or comments, be happy to connect on Twitter: @mikeharrisNY

Charting and backtesting program: Amibroker

Technical and quantitative analysis of major stock indexes and 34 popular ETFs are included in our Weekly Premium Report. Market signals for position traders are offered by our premium Market Signals service