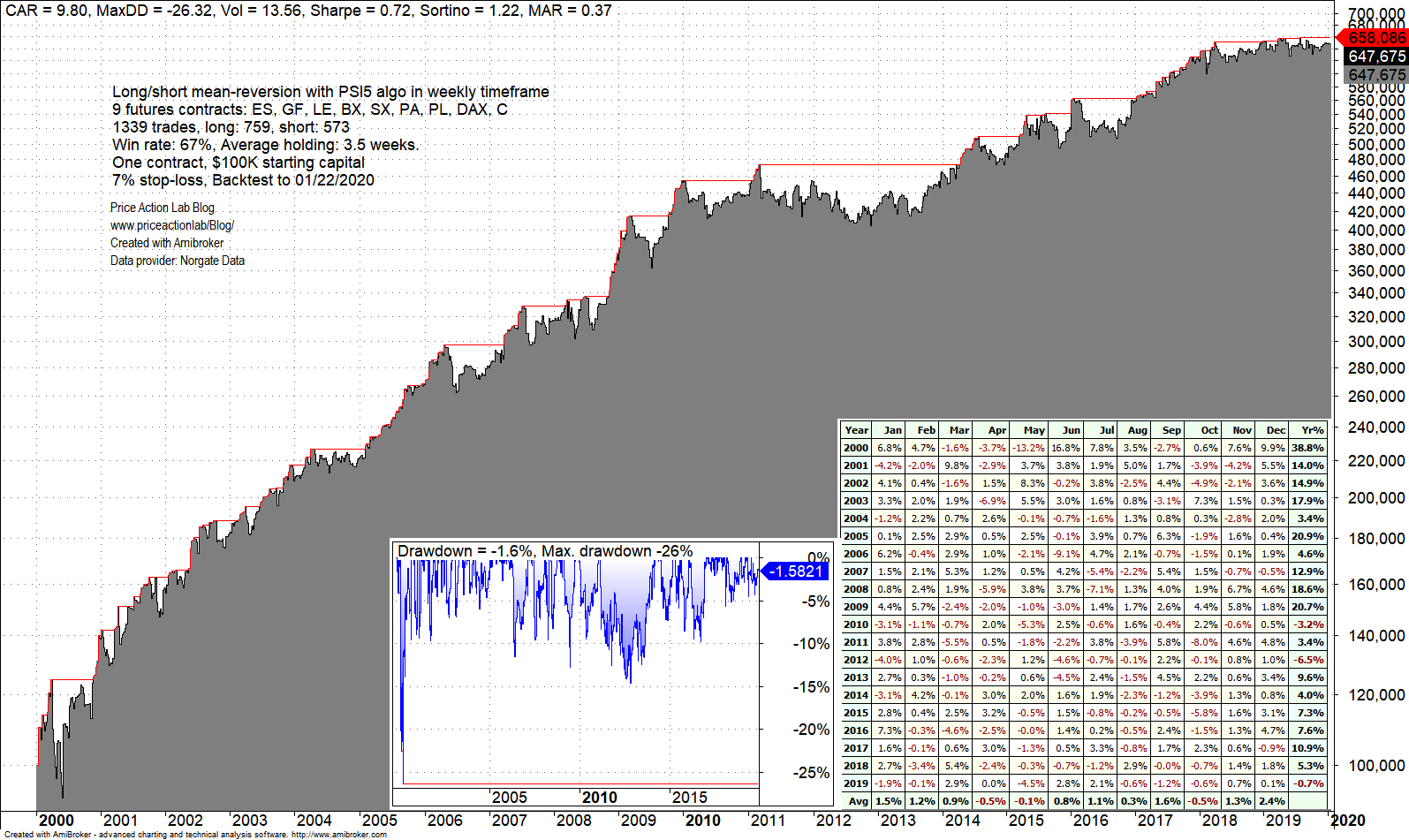

The strategy trades nine futures contracts in weekly mean-reversion mode based on a formula from a probability theory textbook.

This is a weekly long/short strategy for futures contracts that uses the PSI5 algo that is based on a formula from a text in probability to model price action. The PSI5 is available for sale to professional traders and hedge funds subject to acceptance of a non-disclosure agreement.

Strategy backtest settings

Strategy: Mean-reversion based on PSI5 algo

Strategy type: Long/short (exit and reverse)

Time-frame: Weekly (back adjusted futures data)

Futures markets: ES, GF, LE, BX, SX, PA, PL, DAX, C

Backtest period: 01/03/2000 – 2020/01/22

Commission per contract one way: $5

Initial capital: $100K

Position size : One contract per futures market

Maximum open positions: 9

Trade entry and exit: Open of next bar

Stop-Loss per position: 7%

Backtest results

The strategy performed well during dot com and 2008 bear markets offering equity market tail risk hedge. CAGR is 9.8% at 26.3% maximum drawdown.

The table below summarizes the performance of the strategy.

| CAGR | 9.8% |

| Max. DD | -23.3% |

| Sharpe | 0.72 |

| Win rate | 67% |

| Trades | 1339 |

| Long trades | 759 |

| Short trades | 580 |

| Avg. holding period (weeks) | 3.5 |

The win rate is 67%. The high win rate of PSI5 algo in all markets and timeframes minimizes the probability of a large cumulative loss.

Stop-loss can be adjusted to satisfy different risk criteria. In the article we used 7%.

The PSI5 algo works well across equities and futures in both daily and weekly timeframes. Click here for more articles.

Charting and backtesting program: Amibroker

Data provider: Norgate Data

Technical and quantitative analysis of major stock indexes and 34 popular ETFs are included in our Weekly Premium Reports. Market signals for position traders are offered by our premium Market Signals service

If you found this article interesting, you may follow this blog via RSS or Email, or in Twitter