The fallacy of the persistent IPO investor is not only due to hindsight bias. There are at least two more cognitive biases involved: survivorship and selection.

A remarkable claim was made a few days ago: Everyone with a computer and a brokerage account can be rich. The example was the +53,000% rise in the stock of NVIDIA corporation (NVDA) since IPO and all someone has to do is to invest in good companies, just like NIVDIA.

Obviously, the above claim suffers from a number of cognitive biases. I introduce in the article the cognitive bias of the persistent IPO investor. This bias is due to other biases: hindsight and survivorship.

The persistent IPO investor bias has become a meme over the years. I have written a few articles in this blog to counter this annoying meme, for example Only Speculators Would Have Held Amazon Stock Since IPO.

Let us take a look at NVDA below. I will argue there is high probability most IPO investors did not make it past 2003.

The daily NVDA chart from IPO to June 28, 2021, also shows the drawdown profiles from all-time high close to close and all-time high and low.

By October 2002, the stock has fallen about 90% from the highs of January of the same year. IPO investors were still making about 50%. Those who did not sell along the 2002 crash probably waited for the rebound in early 2003 and got out. Maybe few devoted investors did not sell.

The argument made in favor of being a persistent IPO investor and not selling after a 90% drawdown is the potential of the company.

“Look how NIVDIA is dominating the GPU space and has profited from crypto mining.”

But crypto didn’t exist in 2003. In fact, there wasn’t such a good story in 2003 in favor of being a persistent investor in NVDA. The story is only available in hindsight. Decision making in 2003 with information available after 2010 is impossible and this mistake is due to hindsight bias.

There is also survivorship bias: why NVDA? Why not another of those dot com stocks that vanished after the bear market? This is survivorship bias.

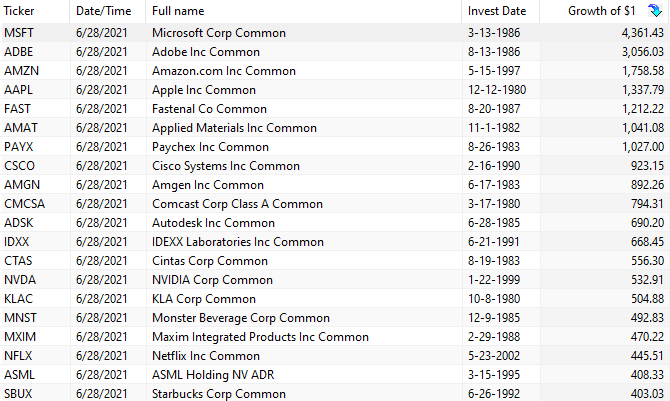

NVDA shows a horrendous drawdown profile. In the case of most tech stocks, IPO investing has been a roller coaster. Below is a table of the most profitable NASDAQ-100 IPOs made since 1990 (current index constituents.)

Source: Price Action lab Blog. Generated with Amibroker

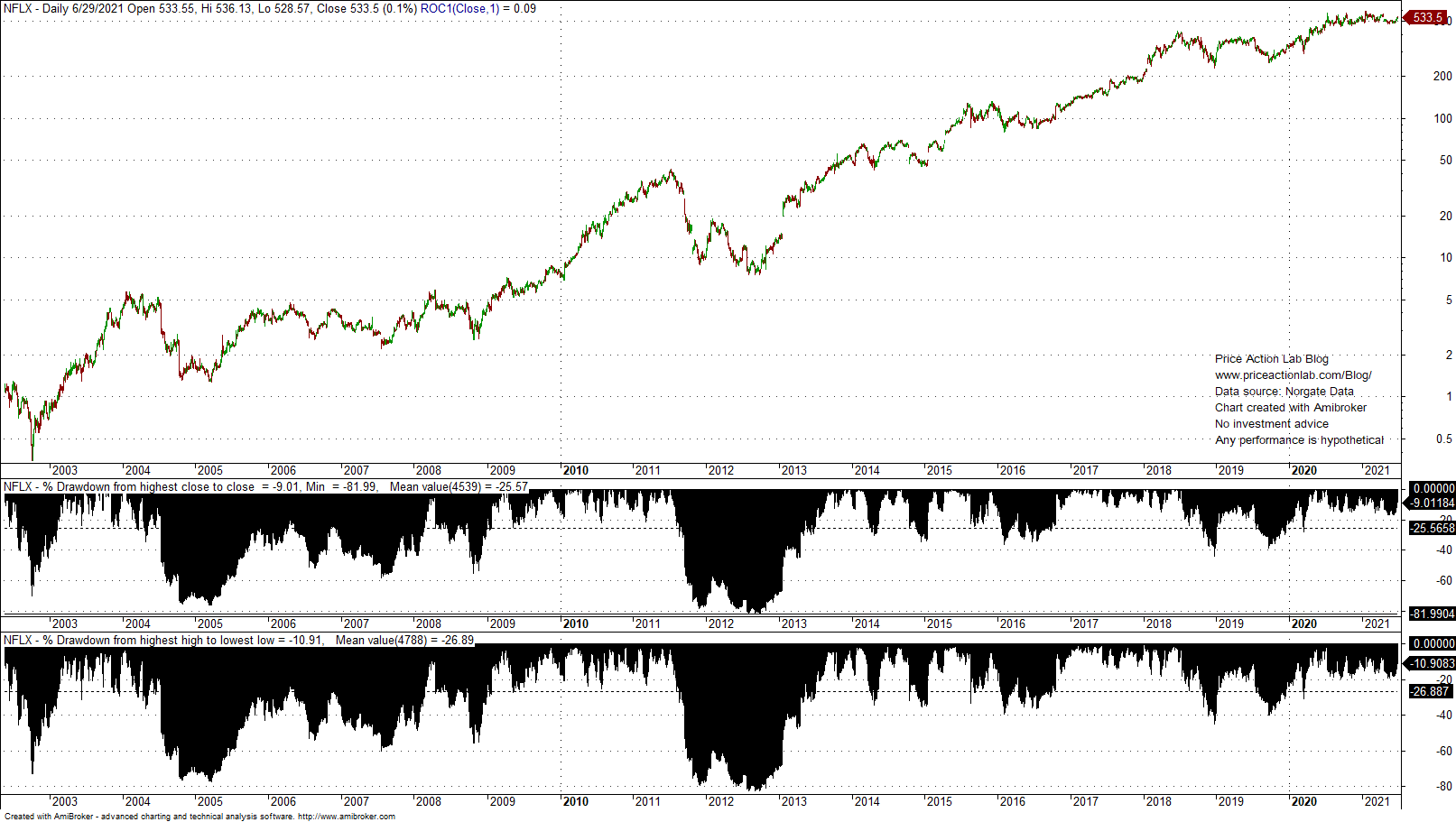

NFLX with an IPO on May 23, 2002 is another one used in “If you have invested X amount of money…” memes. But let us look at the drawdown profile of the stock.

After two massive drawdowns in excess of -76% and -81% in 2005 and 2013, respectively, it is highly unlikely many IPO investors were so persistent to realize gains after 2013.

In my opinion, persistent IPO investing is not for the average person with a computer (nowadays mobile phone) and a brokerage account. IPO investing is sophisticated, highly speculative and at times requires supporting the position to detriment of overall portfolio. Success is maybe 10% work and 90% luck. In a dynamic world there are so many things that can go wrong, as also many things that can be beneficial.

The persistent IPO investor bias shows how very complicated processes in finance are reduced to simple claims of post hoc success due to hindsight and survivorship.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS or Email, or in Twitter

Offer: 25% off with coupon code DC25. Expires Wednesday, June 30, 2021.

Price Action Lab Blog Premium Content