The performance of a price series momentum strategy is improved after adding a simple indicator. Access to Part II of this article requires premium articles or premium insights subscriptions.

During this week you can use coupon PC20 for 20% discount on all subscription plans. The same coupon may be used to renew a subscription to extend expiration. The coupon will expire Friday, July 23, 11:59 pm ET.

By subscribing you have immediate access to hundreds of articles: Premium Insights subscribers have immediate access to more than a hundred articles, Premium Articles and Market Signals subscribers have immediate access to hundreds of articles that include the trader education section and All in One subscribers have access to all past premium content. Click here for more details.

Part I

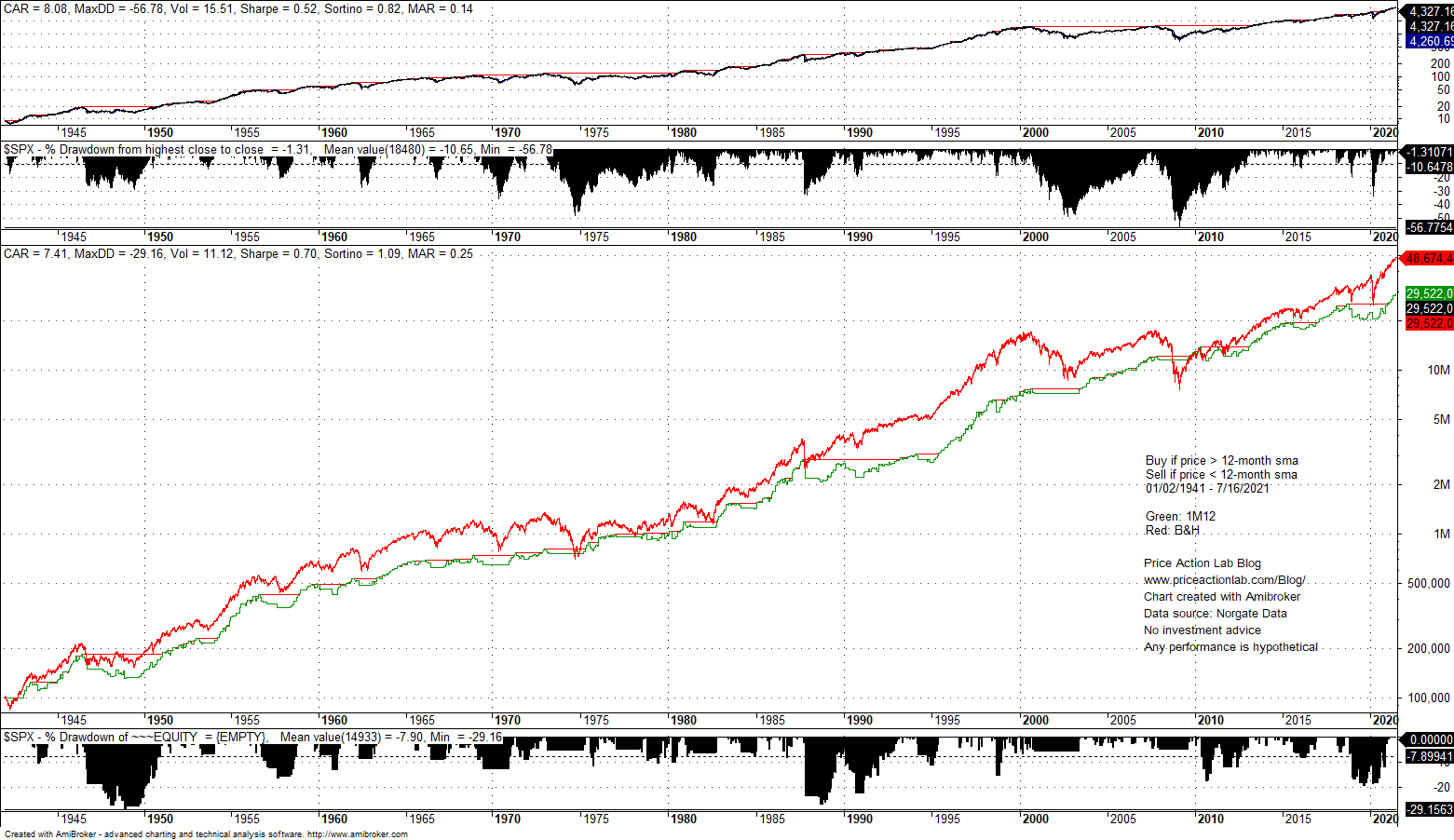

We consider the simple price series momentum strategy in monthly timeframe for S&P 500. This is a well-known strategy that goes long at the next month’s open when price is above the 12-month moving average and exits at the next month’s open when price crosses below the 12-month moving average.

Below is the performance of this simple strategy from 1/2/1941 to 07/16/2021.

The strategy (green line) improves Sharpe of buy and hold (red line) from 0.52 to 0.70 due to lower volatility. Annualized return of the strategy is 7.4% versus 8.1% for buy and hold. However, maximum drawdown of the strategy is -21.2% versus -56.8% for buy and hold. The strategy win rate is 61.7% with a sample of 47 trades in the monthly timeframe.

This momentum strategy offers improved risk-adjusted returns but lower absolute returns. This is the standard behavior of most momentum strategies and one reason they are not very popular among long-term investors since those market participants perceive drawdown as opportunity to buy lower. In fact, most of claims made by momentum proponents are ignored by the passive indexing crowd as naïve since they consider these strategies unnecessary “timing-the-market” burden.

Part II

However, if a momentum strategy could at least match buy and hold total return and at the same time reduce equity volatility significantly, then it may be appealing to a larger audience. In order to do that, we need to realize the following about momentum.

|

This post is for paid subscribers

Already a subscriber? Sign in |

If you have any questions, you may contact support.

Specific disclaimer: This report includes charts that may reference price target levels determined by technical and/or quantitative analysis. No updates to charts will be provided if market condition changes occur that affect the levels on the charts and/or any analysis based on them. All charts in this report are for informational purposes only. See the disclaimer for more information.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS or Email, or in Twitter

Price Action Lab Blog Premium Content