The ensemble of trend-following and mean-reversion strategies boosts the Sharpe ratio significantly due to a low correlation of returns and lower volatility of the ensemble.

The trend-following and mean-reversion strategies are based on the same algo, the PSI5. The trend-following strategy uses the PSI5 algo in divergent mode and the mean-reversion in convergent mode. Only the lookback period changes.

The same basic algo structure results in strategies with uncorrelated returns. This is important because it minimizes data-mining bias that arises from trying to identify algos that yield low correlation for long-term and short-term trading.

| Trend-Following Strategy | Mean-Reversion Strategy | |

| Markets | 23 futures contracts | SPY ETF |

| Timeframe | Daily | Daily |

| Positions | Long and short | Long-only |

| Structure | One entry, one exit, stop-loss | One entry, one exit, no stop-loss |

Backtest period: 01/03/2000 – 02/03/2022.

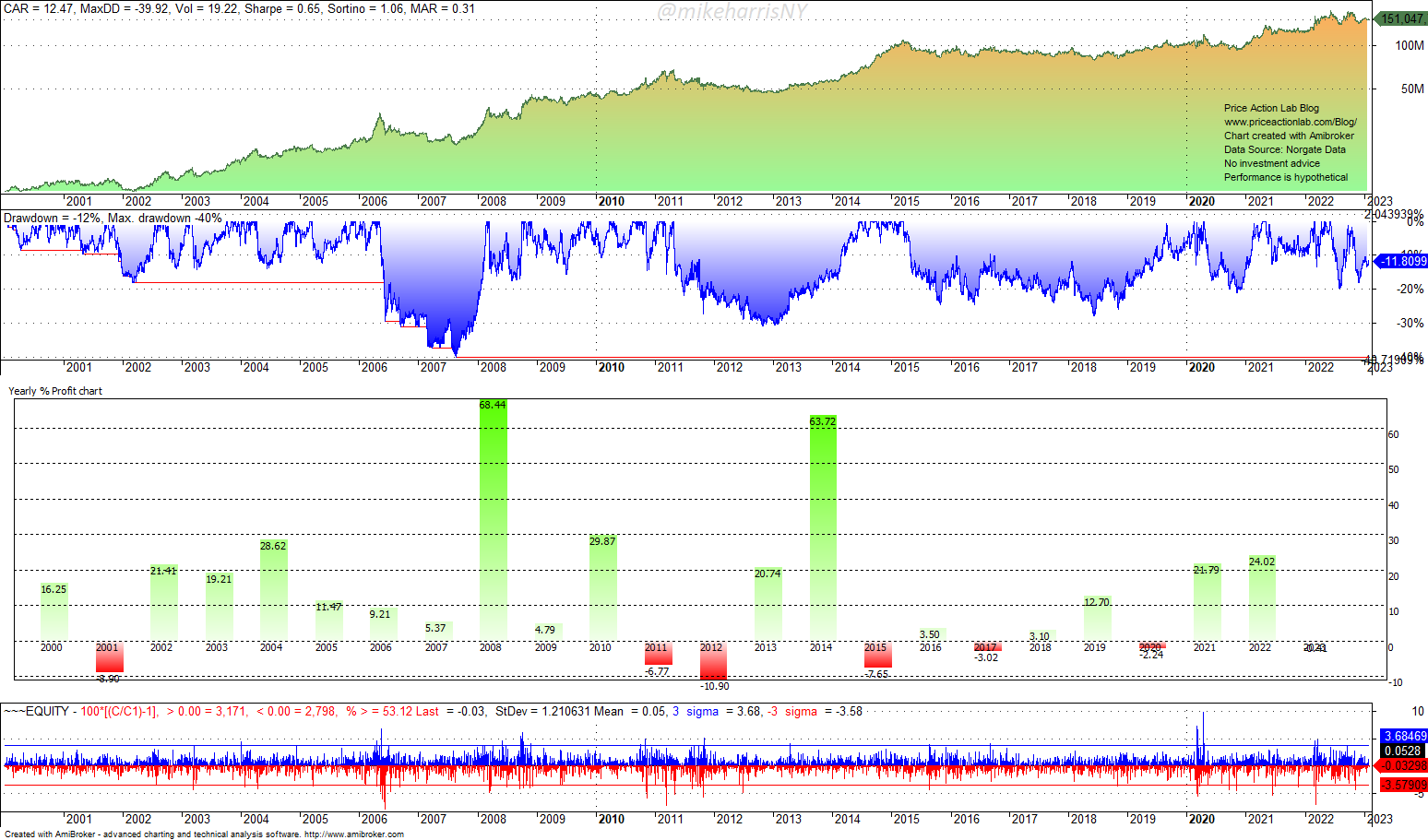

Trend-following strategy equity curve and performance statistics

Comments: The annualized return of 12.5% is high but comes at a high maximum drawdown of 39.9%. The Sharpe is 0.65. Trend-following strategies usually generate high returns but at higher drawdowns. Volatility targeting may be used to smooth the drawdown profile but that comes with a reduction in annualized returns. We prefer the simplest possible structure based on one entry, one exit, and a stop-loss, as opposed to other structures that include trailing stops and volatility targeting due to the risk of curve-fitting. This strategy has provided good convexity during equity markets’ down years, as is evident from the yearly performance chart.

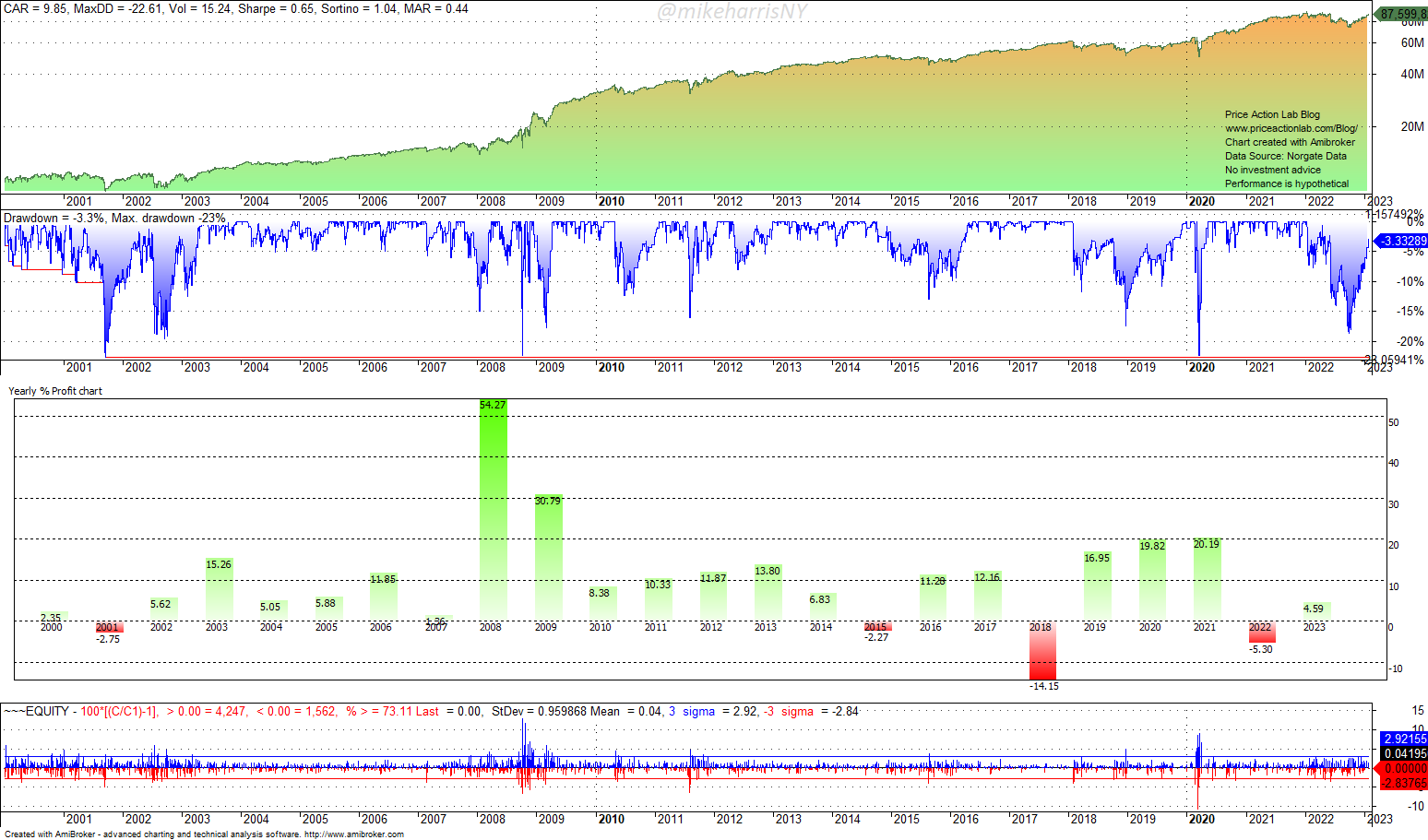

Mean-reversion strategy equity curve and performance statistics

Comments: The annualized return of 9.9% is satisfactory and comes at a lower maximum drawdown of 23%. The Sharpe is also 0.65 for this strategy. Mean-reversion strategies have high risks because there is no stop-loss and they rely on a high win rate to compensate for a low payoff ratio. It is interesting that in 2008 this long-only strategy generated high returns above 50%. This was due to a mean-reversion regime causing strong relief rallies. Last year, strong relief rallies were absent for the most part, and the strategy fell 5.3% but still outperformed buy and hold by a wide margin.

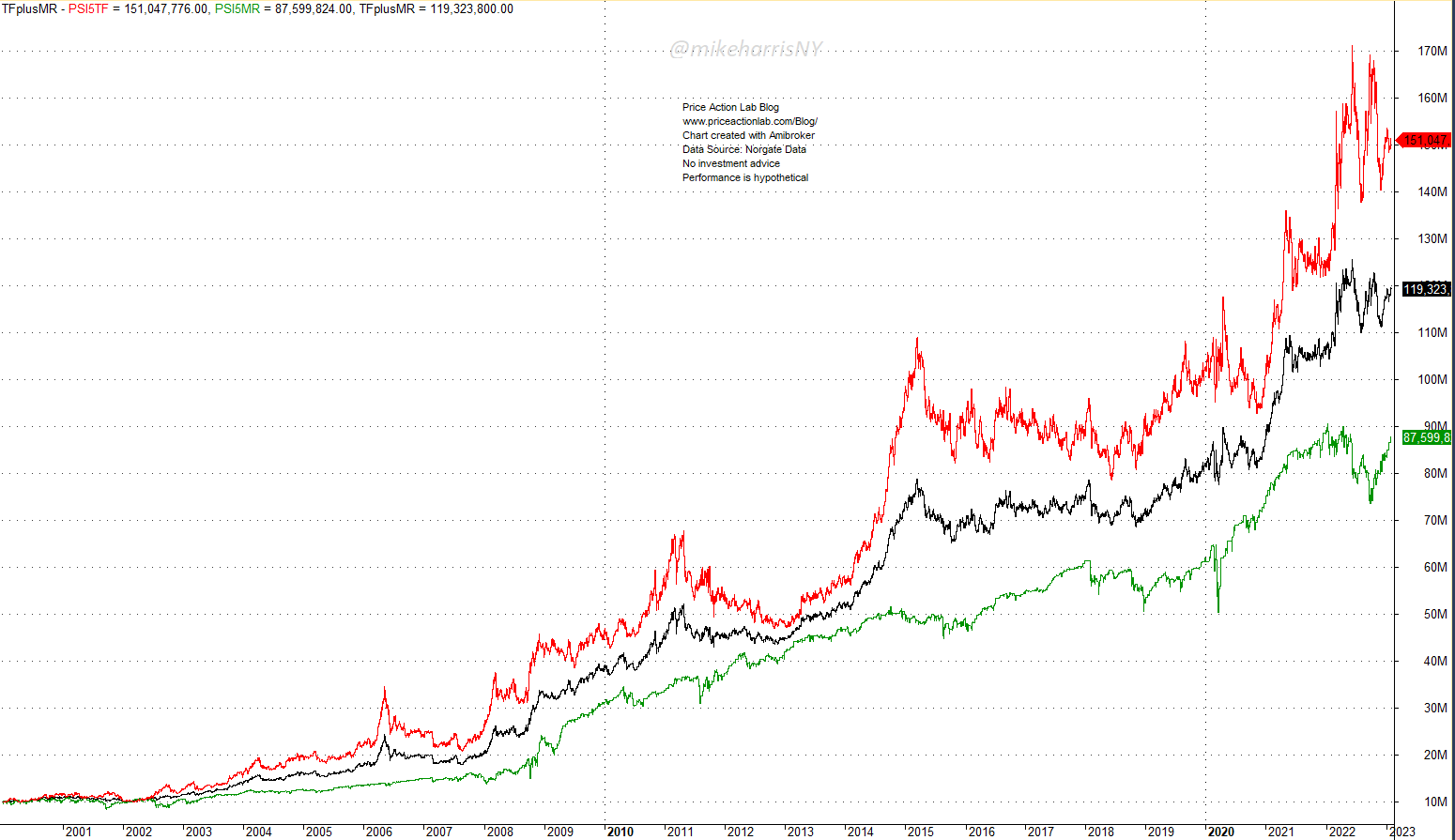

Equity curve comparison

Due to a higher annualized return, the final equity of the trend-following strategy (red line) is nearly double that of the mean-reversion strategy. However, trend-following has higher equity volatility than mean-reversion. The black line is the equal weight allocation to the two strategies (50% weighting) and is smoother.

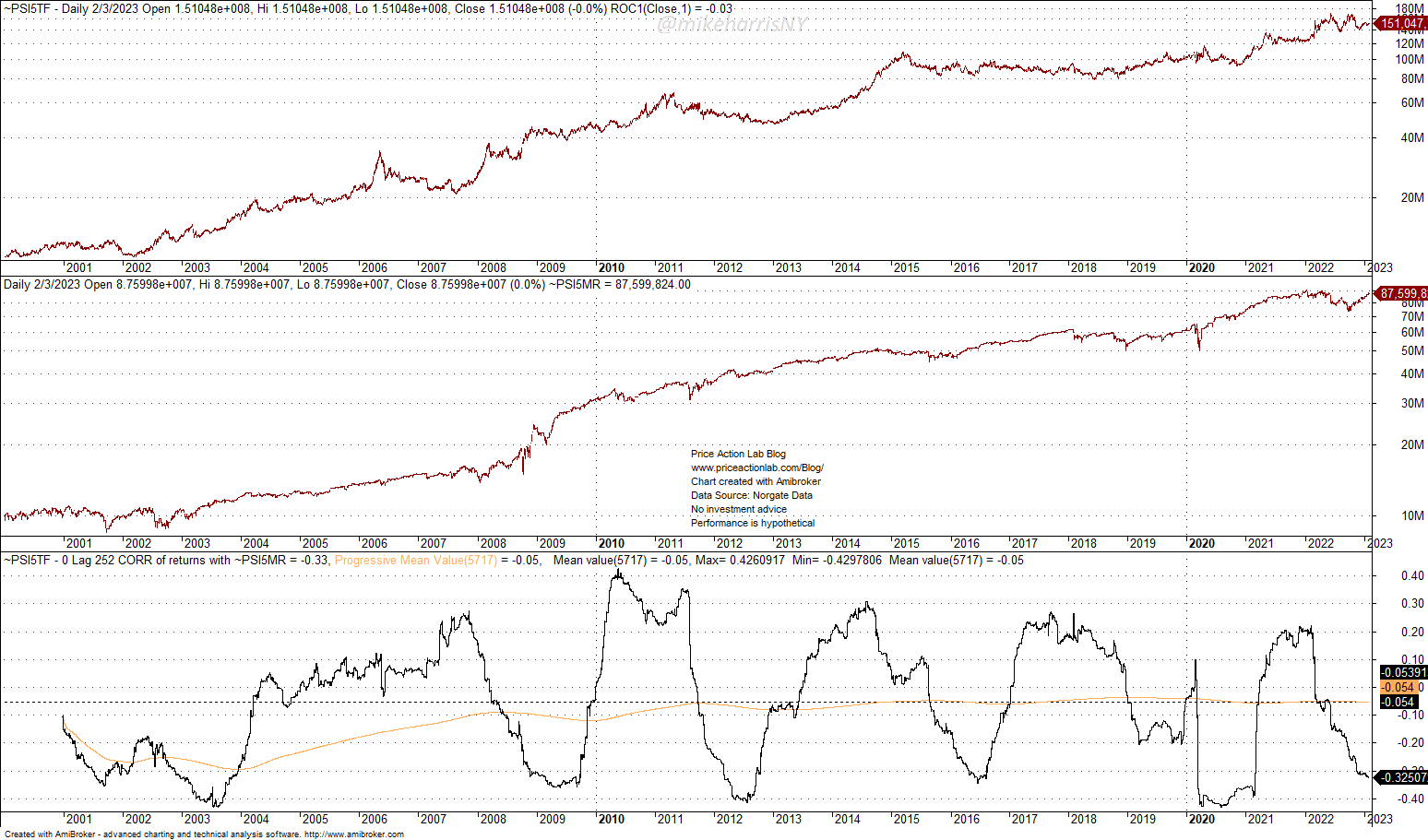

Only in the case that the two equity curves are uncorrelated it makes sense to combine these strategies. Below is the rolling 252-day correlation of the two equity curves.

The 0-lag, 252-day correlation has varied between 0.42 and -0.42 but the average is -0.05. We conclude that the two strategies are uncorrelated on average. Below is the performance of the equal allocation.

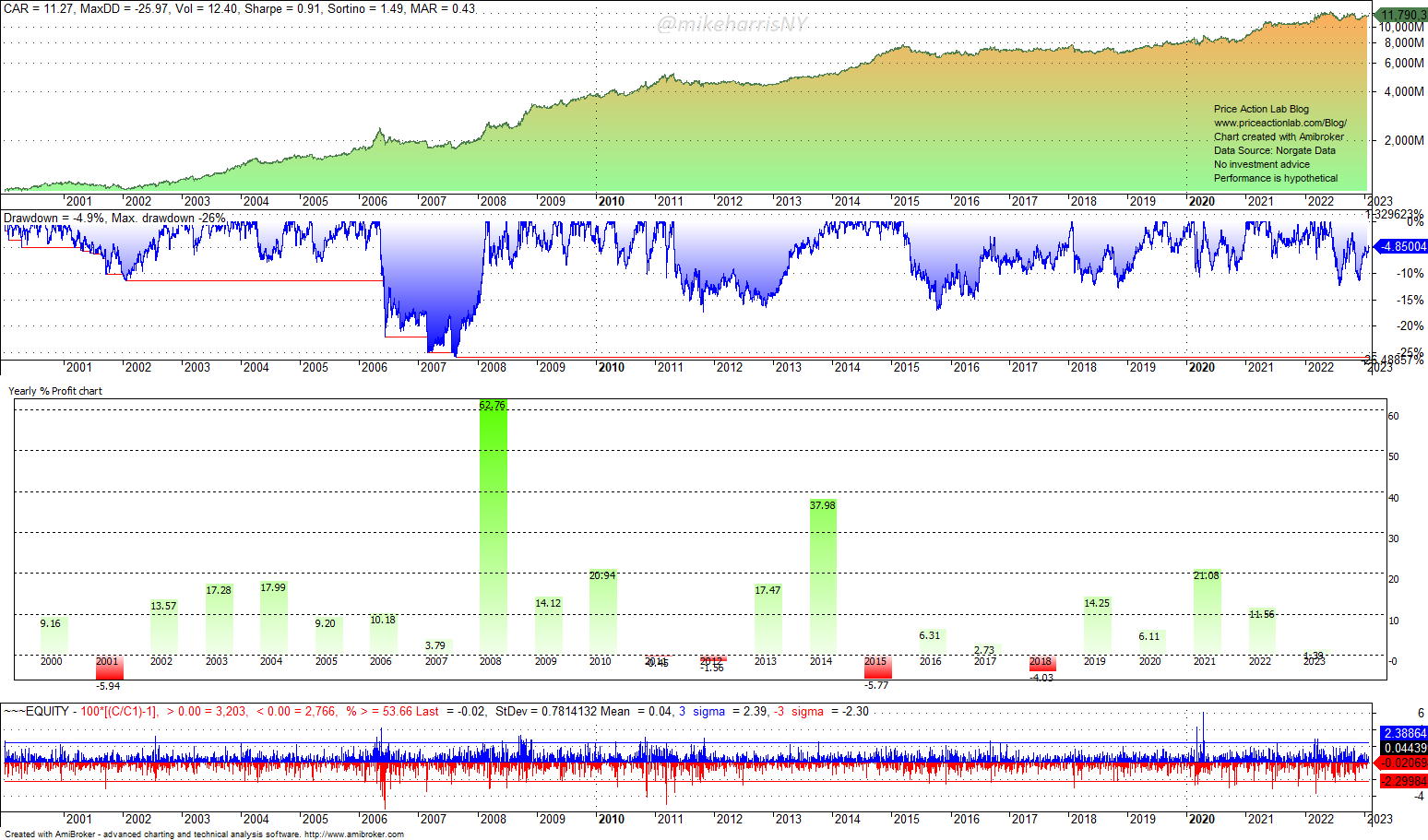

Due to uncorrelated equity curves on average, the Sharpe of the equal allocation increased to 0.91, as expected. The volatility dropped to 12.4% and the annualized return is 11.3%. The maximum drawdown dropped to 26%.

Below is a table with the performance statistics.

| Trend-Following | Mean-Reversion | Equal Allocation | |

| Annualized Return | 12.5% | 9.9% | 11.3% |

| Maximum Drawdown | -39.9% | -22.6% | -26.0% |

| Volatility | 19.2% | 15.2% | 12.4% |

| Sharpe Ratio | 0.65 | 0.65 | 0.91 |

| Average Trade | 12.3% | 0.27% | – |

| Payoff Ratio | 5.1 | 0.71 | – |

| Win Rate | 22.3% | 68.0% | – |

| Number of Trades | 1401 | 863 | – |

| Avg. Holding Period | 73.6 days | 3.9 days | – |

| Exposure | 61.3% | 43.7% | – |

Comments: The equal allocation Sharpe of close to 1 offers the potential for significant leveraged alpha. The ensemble of divergence and convergence behavior of the same algo has better performance.

The PSI5 algo rules are available for sale. Click here for more details.

Q: Why is the algo for sale when it has the potential of generating superior results?

Experience traders manage risk carefully by controlling relevant parameters and the allocation to strategies. Wealth accumulation with proper risk management requires large capital. Those who do not raise money from customers, i.e., those who are not fund managers, must raise capital to trade by selling assets. Since trading performance depends on many other factors and especially on discipline to follow the signals while exercising proper risk management, the potential edge is not in danger from arbitrage.