This is a simple strategy for trading Russell 3000 stocks short-only. The strategy has a high Sharpe ratio.

Update: This article was updated on December 29, 2023.

For all backtests in this article, we used Norgate data for the Russell 3000 index, which includes current and past constituents. We highly recommend this data service (we do not have a referral arrangement with the company).

Timeframe: Daily (adjusted data)

Index: Russell 3000 (current and past constituents)

Strategy type: Short-only tail hunting

Maximum open positions: 5

Position size: equity/5

Commission: 0.1%/share

Trade entry: All trades are executed at the open of the next bar

Backtest range: 01/02/2002 –12/29/2023

Comments

- The backtest started in 2002 because before that, the yearly returns were very high and, in our opinion, unrealistic in the current market environment.

- The strategy has no price action filters and uses tight stops.

- Only stocks with an unadjusted price higher than $10 are traded.

- The maximum number of shares traded is set at 2% of the daily volume for all tickers.

- Survivorship bias was removed from the backtest with the use of series with delistings.

- This strategy could be hard to trade due to demand for efficient execution.

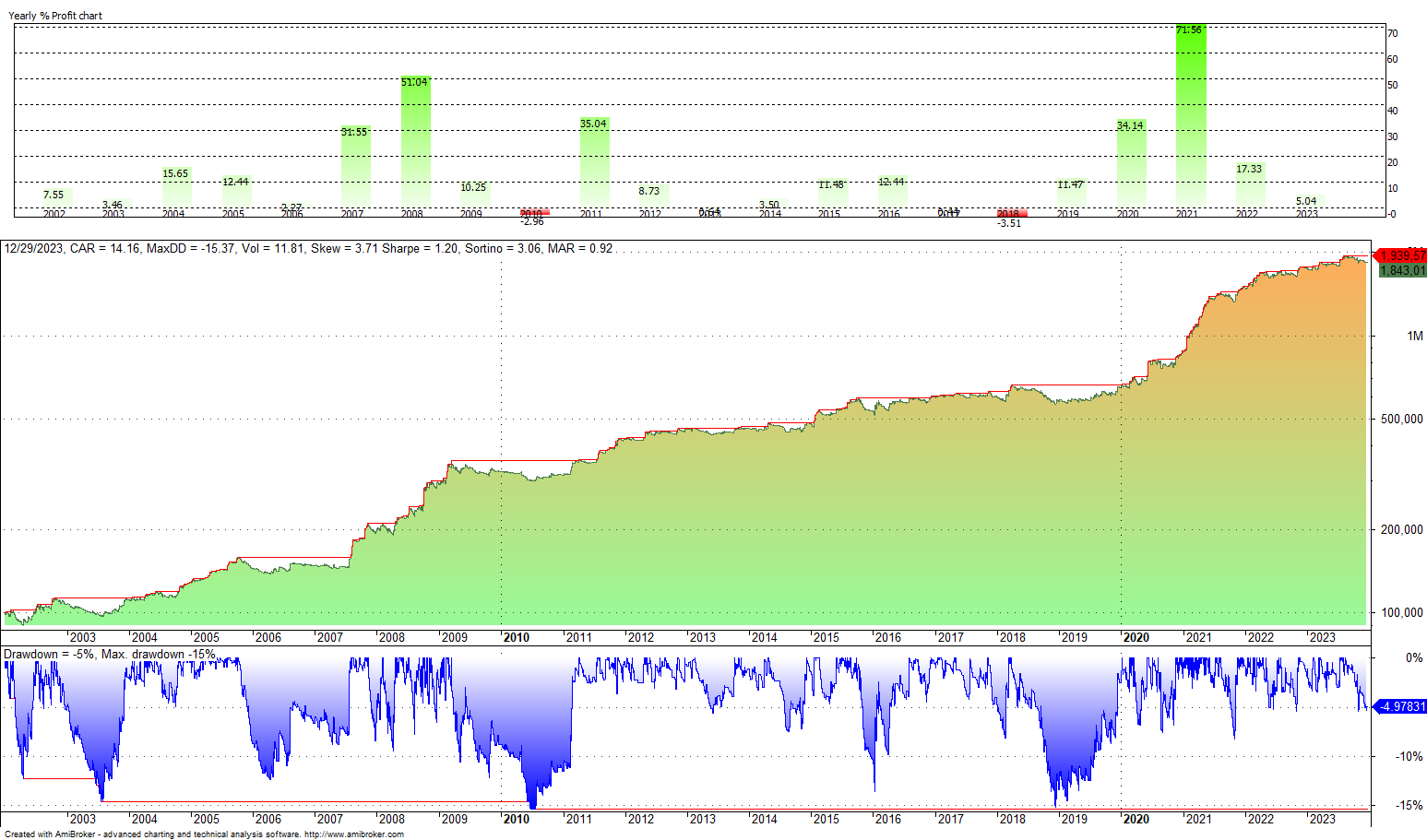

Equity curve, yearly returns, drawdown profile, and histogram of daily returns

Performance Summary

| CAGR | 14.1% |

| MDD | -15.4% |

| SHARPE | 1.20 |

| MAR (CAGR/MDD) | 0.92 |

| TRADES | 6,142 |

| WIN RATE | 24.4% |

| AVERAGE TRADE | 0.30% |

| PAYOFF | 4.1 |

| EXPOSURE | 25.2% |

| SKEW | +3.15 |

The strategy’s CAGR is 14.2% and the maximum drawdown is 15.4%. The Sharpe ratio is 1.2, and the win rate is 24.4%. The skew is 3.15.

The rules of the strategy are available separately and as part of the bundle of strategies. Contact us for more details. Instructions for unlocking the restricted content below will be emailed after payment is received.

|

This post is for paid subscribers

Already a subscriber? Sign in |

Click here for a list of strategies.

About the risks of left-tail hunting strategies

Left-tail hunting strategies are risky due to mean reversion, and stop-loss orders might not provide sufficient protection if there is a violent reversal to the upside.

Shorting stocks often suffers from the unavailability of inventory, recalls, and high borrowing costs.

Update on September 8, 2023

If you cannot borrow a stock to short, there may be a few choices:

1. Skip to the next stock you can borrow based on rank, if one is available.

2. Buy ITM puts. Sell ITM calls.

End of update

Tail-hunting strategies are only good for experienced traders who know how to manage risk and are willing to take on big risks.

When using a profitable tail-hunting strategy, inexperienced traders may lose money because they are afraid to act on signals that are risky at first but pay off in the long run. This is especially true for strategies with a lower win rate.

Tail-hunting strategies should be pursued with a small allocation of available trading capital. Their main objective is to provide positive skew and convexity when other strategies underperform.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS, Email, or Twitter