Strategies fail when market regimes change. I include in this article an example of a popular trading strategy for trading NASDAQ-100 stocks with excellent backtest performance for 26 years before crashing.

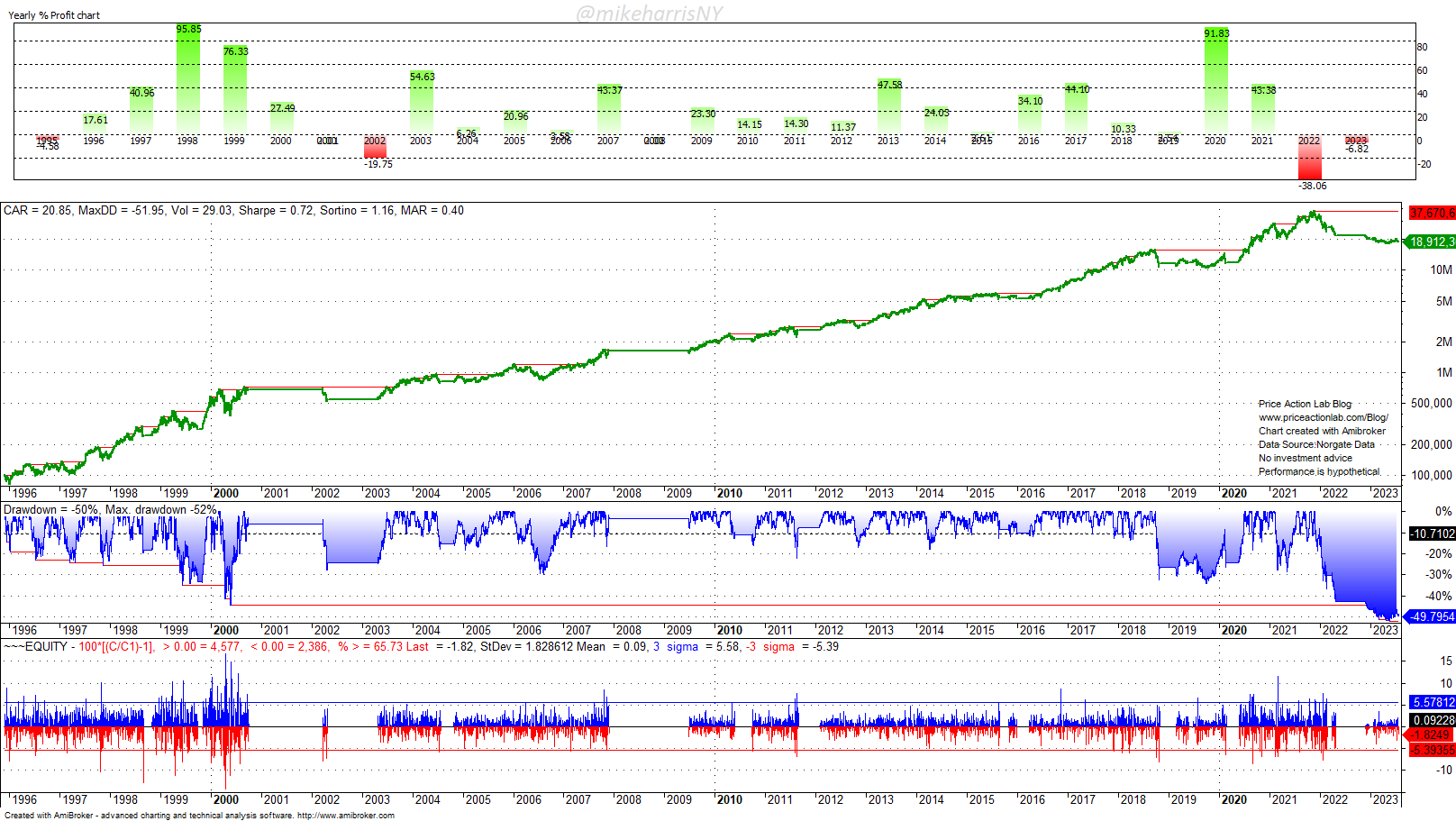

Trading NASDAQ-100 stocks with monthly rebalancing was a popular strategy for a few years before the 2022 market correction. The backtests indicated excellent performance, a significant alpha, and high risk-adjusted returns. Up until the trade became unsustainable due to a crowding effect and a market regime brought about by rising interest rates, some traders believed it to be almost the Holy Grail. The result was a nearly 50% drawdown after 2021.

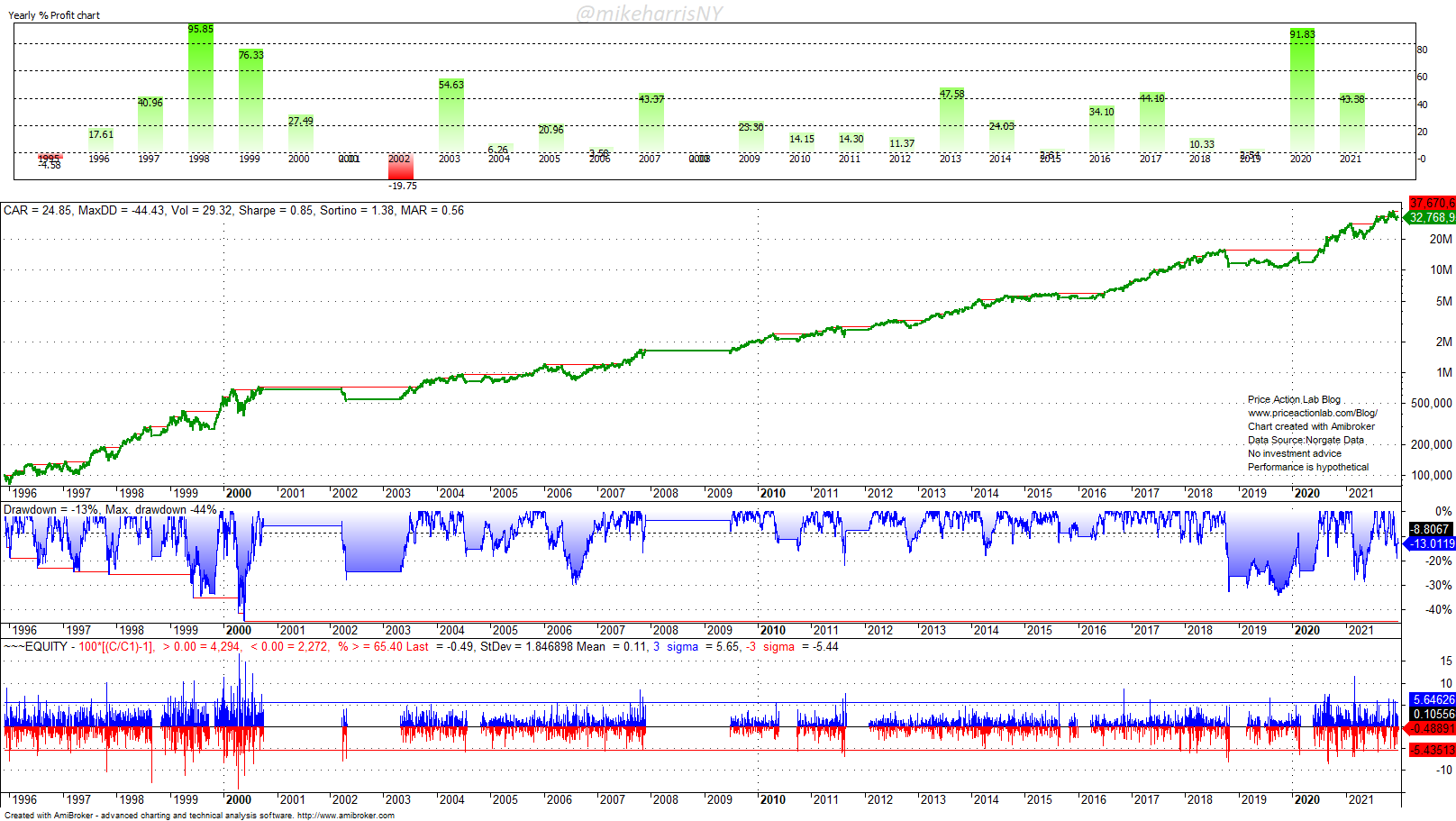

The strategy is simple. Buy several NASDAQ-100 stocks at the beginning of the month that are trading above their 200-day moving average, as long as the S&P 500 trades above its 200-day moving average. Exit at the open price of the month if the stock price or the S&P 500 drop below their 200-day moving average. Rebalance every month, and if there are more candidate stocks to go long, use the 252-day rate of change to rank them and consider only the top stocks. A popular choice for the number of stocks has been 6.

I used Norgate data for the NASDAQ-100 index, which includes current and historical constituents, for the backtests in this article. I recommend this data service (I do not have a referral arrangement with the company).

The annualized return is close to 25%! The Sharpe ratio is 0.85 because volatility is high at 29.3%. The maximum drawdown was 44.9% during the dot-com bear market, but the strategy was overall profitable during that period. With only two losing years and a gain of nearly 100% in 2020, some thought this came close to the Holy Grail. Financial bloggers with a limited understanding of the perils of backtesting and the risks of high volatility praised the strategy. Then the shock came.

In 2022, due to rising rates and long-duration tech stocks crashing, the strategy lost 38%. The maximum drawdown increased to nearly 50% this year. The strategy has failed due to a regime change. The odds of a rebound are slim, and the equity line of this strategy will drift sideways in the best-case scenario.

In trading and investing, if it is too good to be true, there is probably a catch. Some strategies, like our B2S2 mean-reversion for Dow 30 stocks, have high annualized returns and Sharpe ratios of about 1, but they are risky due to not using stops. But mean-reversion is unlikely to go away anytime soon. On the other hand, strategies that rely on favorable interest rate regimes, like the NASDAQ-100 strategy discussed above, have risks from regime changes and can generate large losses. Using an ensemble of strategies reduces the variability of returns, but at the cost of lowering absolute performance; there is no free lunch in the markets.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS, Email, or Twitter