In this article we investigate whether the addition of mean-reversion can increase the performance of an equity long/short trading strategy based on price action features.

One fundamental trade-off in trading strategy design is that increasing the annualized return usually causes an increase in drawdown. This is in agreement with the empirical fact that higher returns require higher risks.

In this article, the equity/long short strategy is based on features calculated by DLPAL LS as described in more detail in this article. For this article we consider maximum 6 open positions, long or short. The details of the strategy are given below.

Strategy details

Time-frame: Daily (adjusted data)

Strategy type: Long/short equity (with bias, i.e., not dollar neutral)

Universe: Dow stocks from current composition (DOW not included and DWDP data ended 05/31/2019)

Backtest period: 01/03/2008 – 01/31/2020

History considered for feature calculations: 01/03/2000 – 12/31/2007

Maximum open positions: 6

Position size per stock: Equity/6

Minimum holding period: 1 day

Position entry: Open of next bar

Position exit: Open of next bar

Commission: $0.005/share

DLPAL LS generates various types of features for individual but also for groups of securities but the two relevant for the long/short strategy in this article are the directional bias Pdelta and its significance S.

The strategy is as follows:

Buy/Cover if Pdelta × S > 0

Short/Sell if Pdelta × S < 0

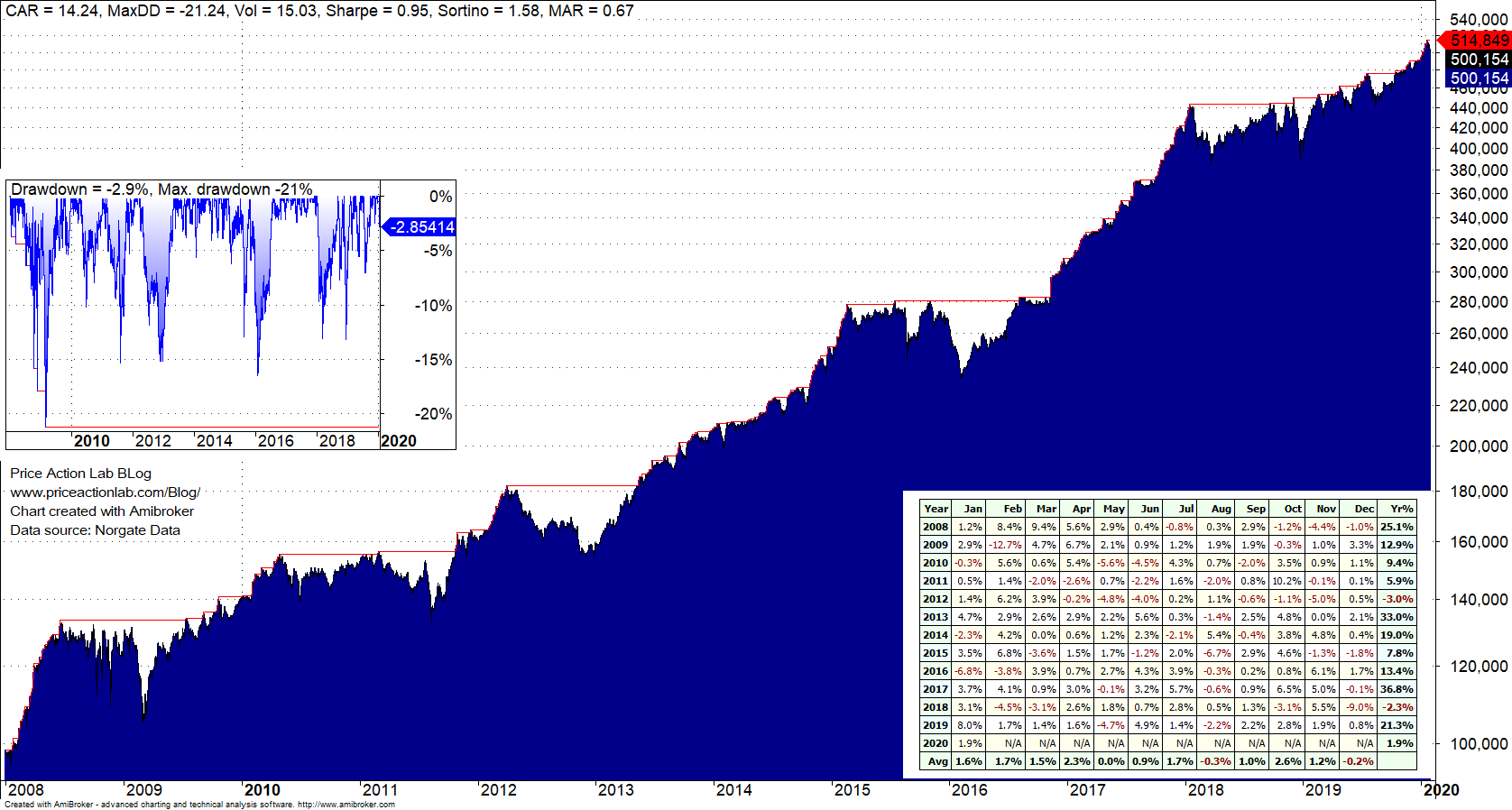

Below are the equity curve, monthly returns and drawdown profile for the backtest period.

The strategy (called ML in this article) shows good performance in 2008 and 2011 with potentially convex returns during bear markets. More details about performance later.

We are interested in finding out whether addition of a mean-reversion component to the strategy can improve performance. For this purpose we will use our proprietary PSI5 mean-reversion algo.

There are several ways of combining strategies: the union, the intersection or variations of these two based on long and short component and addition of other filters. Below we list the two strategies that resulted in higher CAGR and/or lower maximum drawdown:

ML long/short OR PSI5 long component (MLPSI5L)

Buy/Cover if Pdelta × S > 0 OR PSI5 long signal

Short/Sell if Pdelta × S < 0

ML long/short when uptrend in a security, ML long/short OR PSI5 long/short when downtrend in a security (MLPSI5TF)

If uptrend

Buy/Cover if Pdelta × S > 0

Short/Sell if Pdelta × S < 0

If downtrend

Buy/Cover if Pdelta × S > 0 OR PSI5 long signal

Short/Sell if Pdelta × S < 0 OR PSI5 short signal

Below is a table with the results for all three strategies:

| Parameter | ML | MLPSI5L | MLPSI5TF |

| CAGR | 14.2% | 14.9% | 14.6% |

| Max. DD | -21.2$ | -19.0% | -16.1% |

| Sharpe | 0.95 | 0.95 | 1.06 |

| Win rate | 55.6% | 56.2% | 56.1% |

| All trades | 4906 | 5670 | 5474 |

| Long trades | 3697 | 3763 | 3634 |

| Short trades | 1209 | 1307 | 1840 |

| Payoff ratio | 1.02 | 1.00 | 0.97 |

| 2008 return | 25.1% | 25.8% | 6.4% |

| 2011 return | 5.9% | 7.5% | 15.5% |

The trade-off is evident from the above table: since CAGR is about the same, the impact on performance depends on redistribution of returns. There is a large difference between the 2008 return of ML and MLPSI5TF strategies while at the same time there is inverse impact on 2011 return. Selecting a strategy based on redistribution of returns from a group of strategies with statistically indistinguishable performance is difficult.

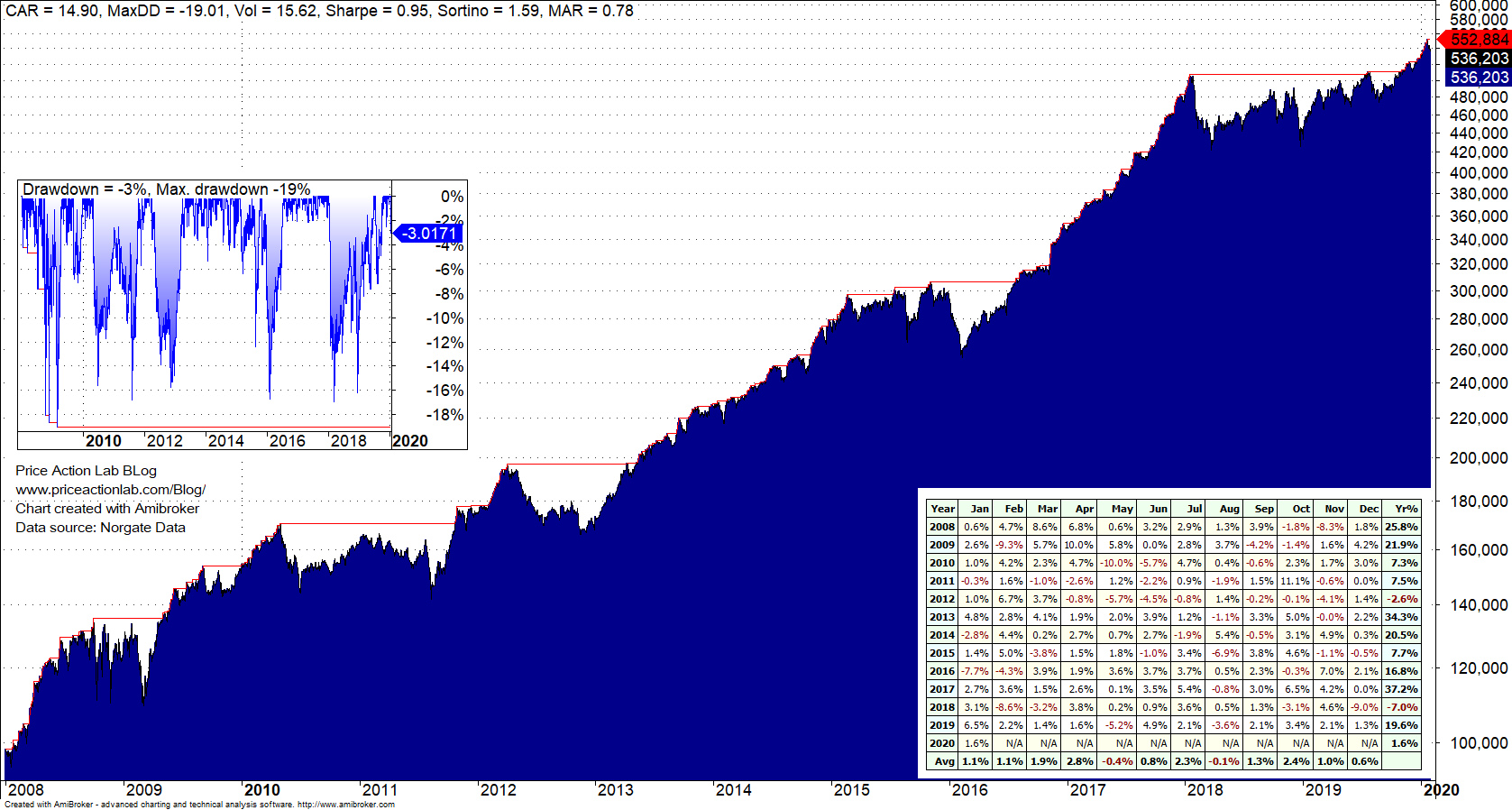

Below are the equity curve, monthly returns and drawdown profile of the MLPSI5L strategy for the backtest period.

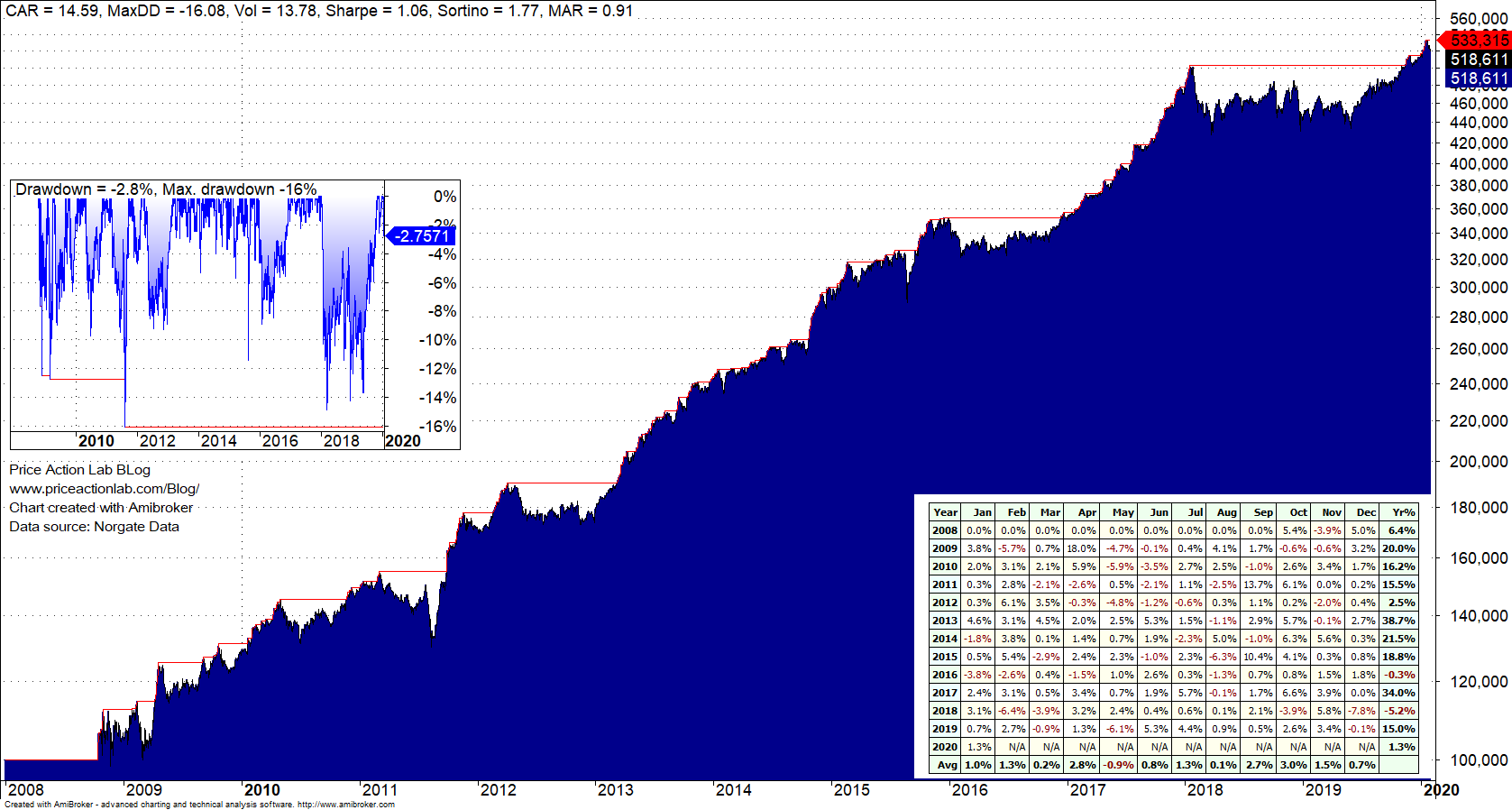

Below are the equity curve, monthly returns and drawdown profile of the MLPSITRF strategy for the backtest period.

I prefer MLPSI5L because of the good performance in 2008 and the fact that long/short strategies are supposed to outperform in bear markets and make up for periods of lackluster returns. Those who look at absolute returns may choose MLPSI5TF.

There were other combinations that generated even smoother equity curves but lower CAGR and/or higher maximum drawdown and were rejected.

Conclusion

Mean-reversion does not add significant alpha to long/short because it is already accounted for in the DLPAL LS features. However, there can be sizable impact on maximum drawdown if mean-reversion is used appropriately. The results indicate that the best time to use mean reversion may be during downtrends.

A different way of developing trading strategies

DLPAL LS offers a different way of developing trading strategies that does not rely on traditional indicators and naive approaches of combining them through random mutations or genetic algorithms. This program is used by fund managers around the world to develop long-short but also directional strategies in a variety of markets.

More details about DLPAL LS can be found here. For more articles about DLPAL LS click here.

If you have any questions or comments, happy to connect on Twitter: @priceactionlab

Strategy performance results are hypothetical. Please read the Disclaimer and Terms and Conditions.