In the markets there are short-term traders and tactical investors. Both these market participants and their strategies are usually considered the same group but this is due to confusion: traders need high volatility to profit whereas tactical investing works best in a low volatility environment with a smooth trend.

It is not accidental the number of retail brokerage accounts spikes during market turmoil periods. Even amateurs understand that volatility means opportunity for traders but it seems many in the field do not and treat short-term trading and tactical investing as one subject. This is due to misunderstanding the business.

For example, a strategy that goes flat when the S&P 500 falls and stays below its 200-day moving average may be useful and profitable but it does not have a very good connection to what most active traders do.

The 200-day moving average cross condition in S&P 500 occurred on March 5 of this year and some strategies that use this filter have been out of the market for 51 trading days. During this time, the S&P 500 fell 26% to the bottom of March 23 and then rose 32% as of May 18. This was a high volatility period that offered high potential for profit but also risks to active traders during which many tactical investing strategies were flat.

There is nothing wrong with being flat and actually that may be a good decision but it is not active trading: anyone who does that is obviously not trading and many that do it actually do not know how to trade high volatility periods although they consider themselves traders.

With simulations we will demonstrate how profit potential increases during high volatility periods. We will compare the performance range (minimum and maximum returns) of a large number of random traders (20000) that use a fair coin to trade SPY ETF as follows:

Case 1: Long at the close of the day if heads – short at the close of the day if tails.

Case 2: Long at the close of the day if heads – exit at the close of the day if tails.

In all simulations commission is $0.01/share, starting capital is $100K and there is no reinvestment of profits. There simulations are performed over four time periods chosen to correspond with high and low volatility periods, as follows:

Period 1: 01/02/2008 – 05/13/2008 (high volatility)

Period 2: 01/02/2013 – 05/14/2013 (low volatility)

Period 3: 01/03/2017 – 05/15/2017 (low volatility)

Period 4: 01/01/2020 – 05/13/2020 (high volatility)

Below are the results of the simulation for Case 1 in terms of % positive, minimum and maximum returns:

| Period | % positive | Minimum % Return | Maximum % Return |

| 1 | 46.2 | -42.6 | +40.6 |

| 2 | 45.3 | -22.9 | +24.8 |

| 3 | 46.9 | -13.7 | +12.8 |

| 4 | 46.6 | -65.3 | +99.7 |

We notice the following from above table:

1. Percentage of positive returns is about the same despite volatility level.

2. The minimum and maximum returns are significantly higher during high volatility periods.

Therefore, we confirm that profit potential increased in high volatility periods along with maximum risk. This is what traders are looking for and they know that higher profits come at higher risks. For example, in Period 4 the maximum potential was about 7.8 times that of Period 3.

Next, below are the results for Case 2 (long-only)

| Period | % positive | Minimum % Return | Maximum % Return |

| 1 | 38.7 | -24.5 | +22.9 |

| 2 | 96.9 | -6.9 | +18.5 |

| 3 | 94.1 | -4.9 | +11.9 |

| 4 | 33.8 | -44.9 | +51.2 |

We notice the following from above table:

1. Percentage of positive results is much lower in high volatility periods as expected and in low volatility are close to 95%.

2. Long-only traders still have higher profit potential in high volatility periods although the odds of winning are lower.

The above results may be counter-intuitive to some; despite market fluctuations in 2008 and 2020 (Periods 1 and 4), long-only maximum returns are higher than in smooth markets in 2013 and 2017 (Periods 2 and 3.) This shows why even long-only traders prefer high volatility environments and feel there is no opportunity in smooth markets.

Although for every trading success story there are many stories about failures, the objective of this analysis was to show why traders like volatility: it offers opportunity for high returns. Traders are not stupid; they know they may lose everything but they prefer putting the hard work for low odds of making 20% rather than for high odds of making 5%. Many do not understand these dynamics and confuse various styles of trading and especially they call tactical investors traders, which they may be but in a restricted sense of the word.

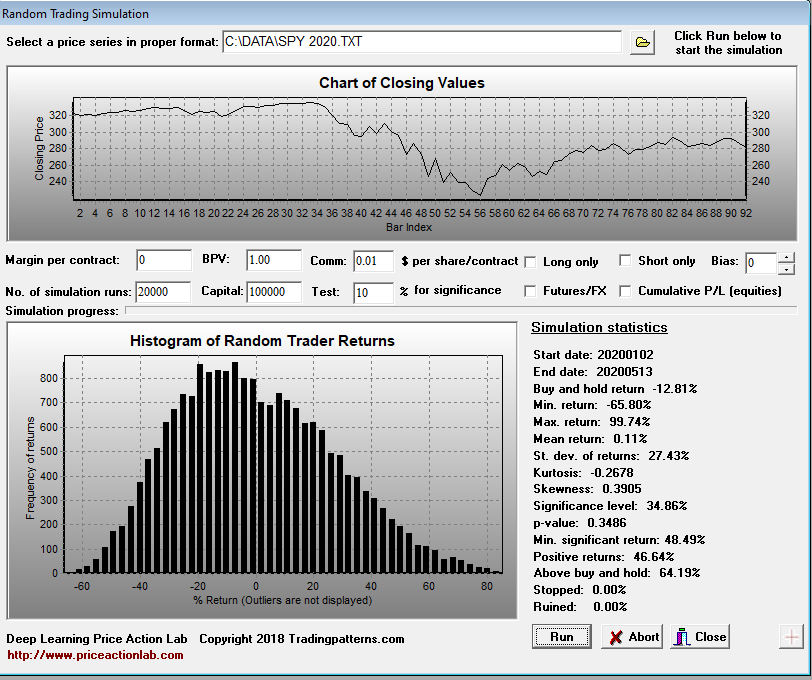

Finally, this is an example of results for Period 4 and Case 1. The simulations were performed with DLPAL S software Random Trading Simulation function.

Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS or Email, or in Twitter

Price Action Lab Blog Premium Content