Growth and value relative strength has changed in different regimes based on the momentum of the companies included in these classifications/factors. Therefore, what occurred in the past may not necessarily occur in the future. Possibly, these notions are outdated.

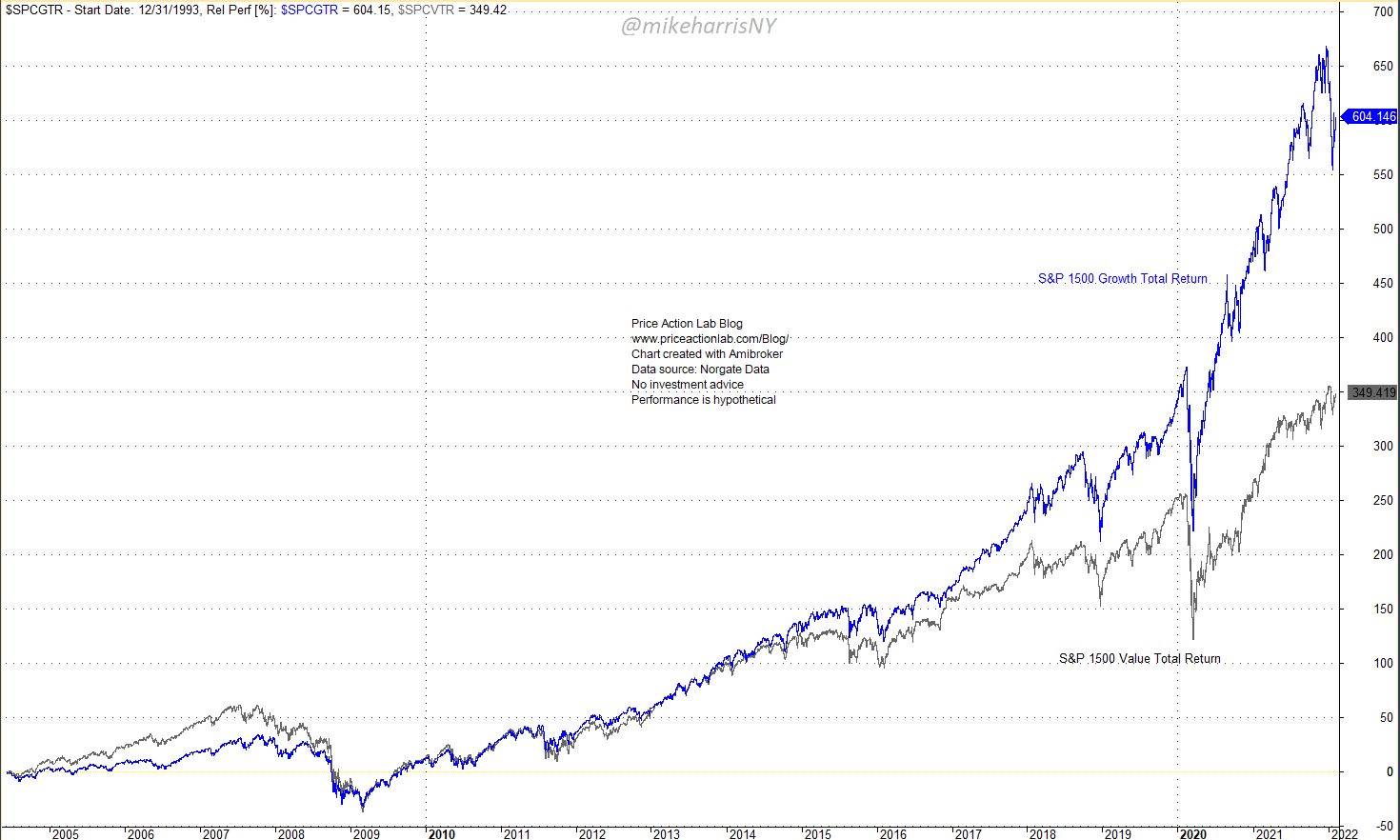

The relative performance chart below shows how value (S&P 1500 Value Total Return) outperformed growth (S&P 1500 Growth Total Return) from 2005 to 2008 but after 2014 there has been a wide divergence in the performance of these two indexes/factors.

There is vast literature on this subject by practitioners and academics. The point in this brief article is more of an epistemological one: do we know what we mean by growth and value in different market regimes and how does meaning change?

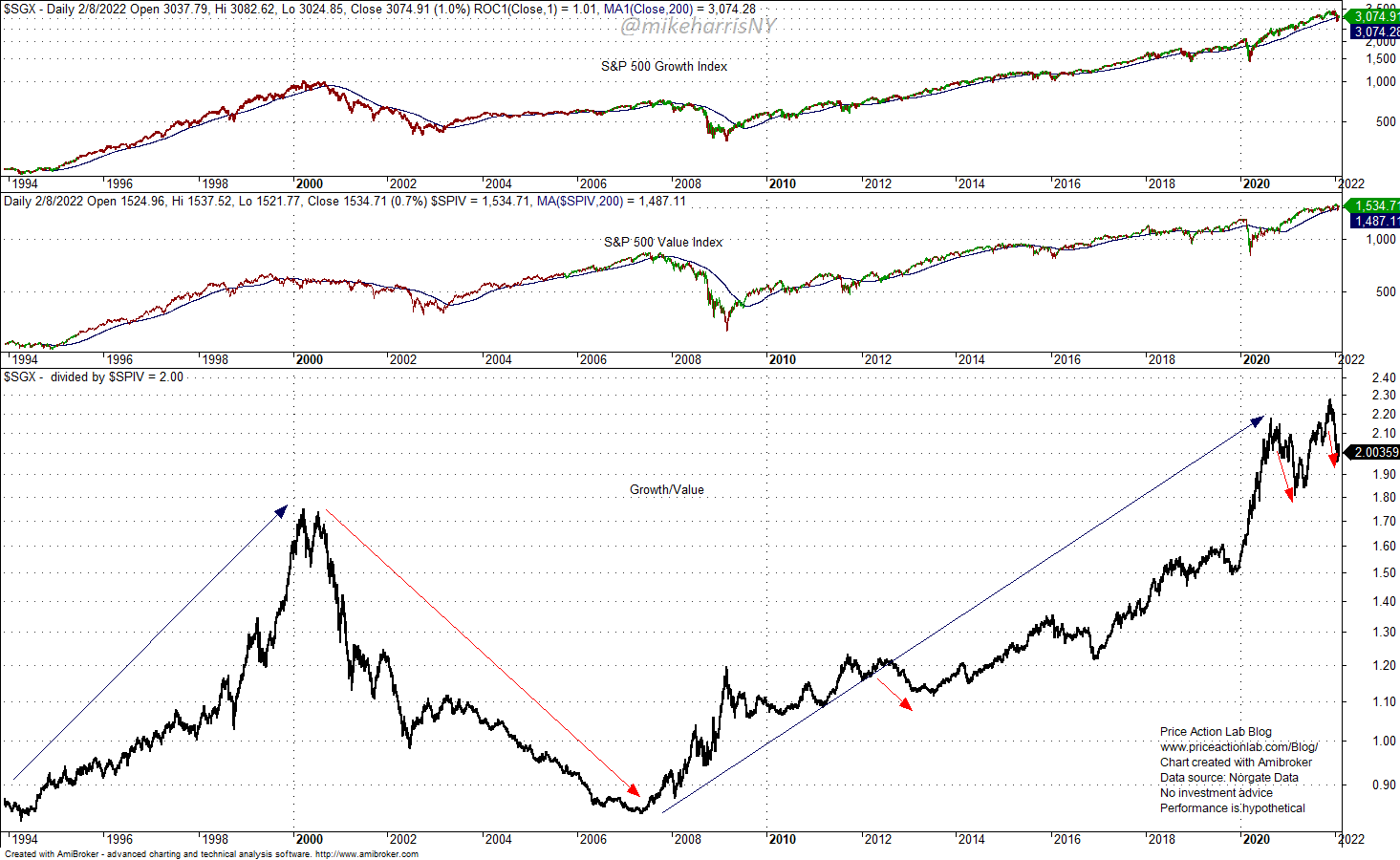

For example, AAPL could be classified as both a growth and a value stock. The current market regime has little relation to 90s regime when growth outperformed value followed by the dot com crash and a long period of value outperformance, as shown in the chart below At this point there is significant overlapping in value and growth as the economy has changed significantly.

The above chart does not show total return indexes but it suffices to reflect what occurred in the 90s, the subsequent collapse of growth, the rise of value, and then the return of growth after the 2008 bear market. Since about 2014 value has struggled but emerged as a dominant factor after the market crash of March 2020. After a few swings, value is again leading, as shown by the red arrows. Can we use past as guide for future?

In my opinion and while respecting those who are experts on this area, what we mean by growth nowadays as compared to the 90s are two different things. As far as value, I assume there is no much change in meaning due to regime changes. However, the dynamic regime changes impact the notion of both.

In other words, growth in the 90s was more fragile notion because of early stage developments in information technology. Nowadays this area is mature and the names we see, for example Meta, Amazon, Netflix, Tesla, Nvidia, etc., utilize mature but evolving technology to innovate and increase market share; this isn’t related to the irrational exuberance of the late 90s. Although there may be many growth companies that won’t deliver in the future, the mega caps are driving the market have done exceptionally well even under pandemic conditions.

Therefore, I’m not sure even in case of a bear market if value will take the lead because (a) there is some overlap between value and growth and (b) this is a different growth regime than in the 90s.

In my opinion, the recent gains in value were “transitory” but value is everywhere and also in growth. So maybe the time has come to declare these factors/classification outdated.

Premium Content 10% off for blog readers and Twitter followers with coupon NOW10

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS or Email, or in Twitter.