The sentiment inferred from social media and other alternative data can be wrong due to low signal to noise ratio and bluffing.

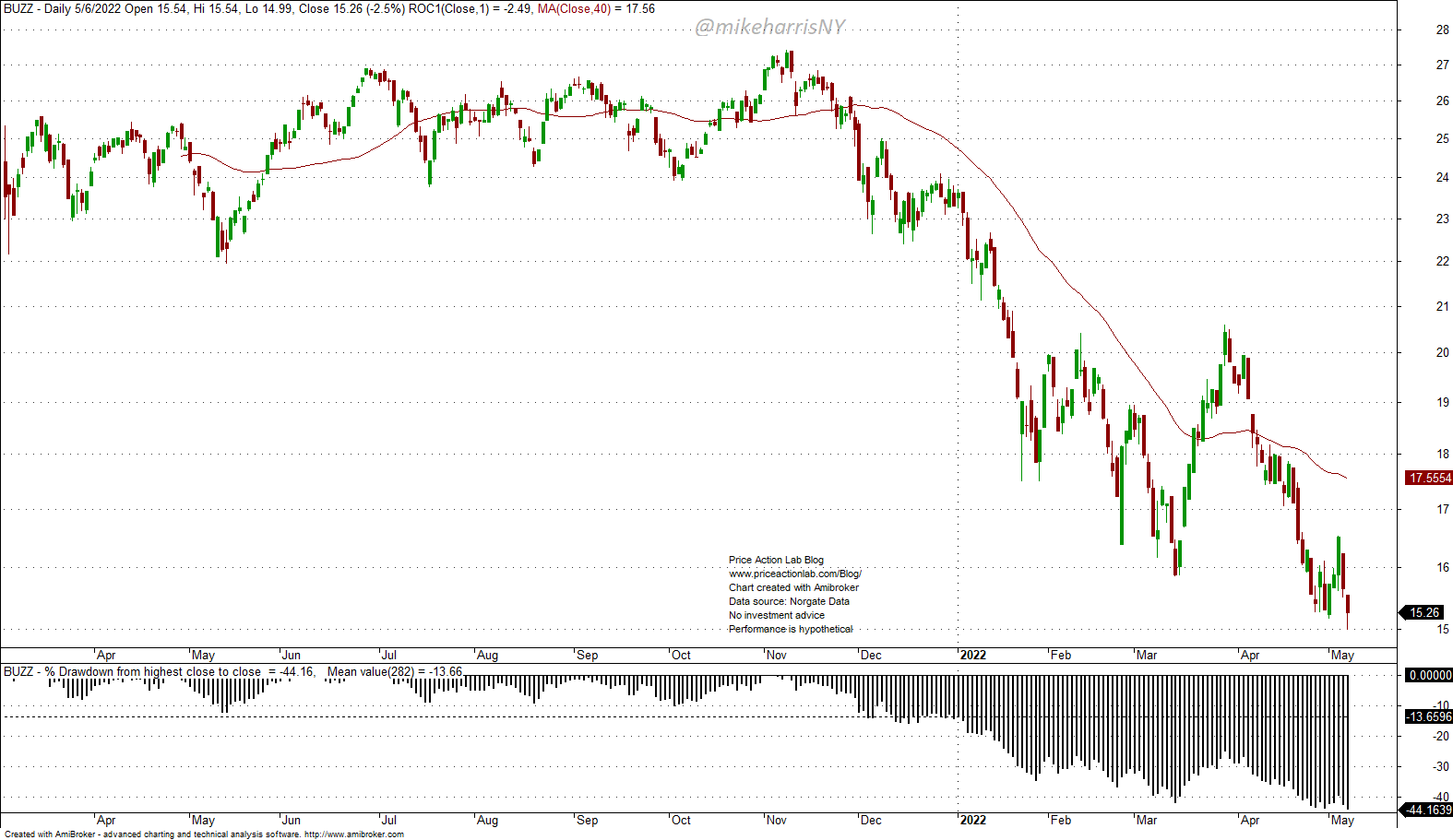

The inception date of BUZZ VanEck Social Sentiment ETF was on March 2, 2021. This ETF is down 34.5% year-to-date, down 35.1% since inception, and down 44.2% from highs.

I’m sure the administrator is doing a good job in measuring sentiment but, in my opinion, the problem is the noise in sentiment, the constant bluffing, and also alternative data in general.

In an article on September 1, 2019, I argued that there is no alpha in alternative data and the main reason is that markets have become increasingly algo-driven.

In addition, social media sentiment may have a low signal to noise ratio. Assigning credibility to posts in social messages to reduce noise is a daunting task since it’s usually the most sophisticated players who are the bluffers, just like in card games.

In fact, in my opinion, there is little correlation between what some people claim about the market and what they do. Markets are a sophisticated exercise in bluffing and the only reliable performance metric isn’t what people say but their P&L.

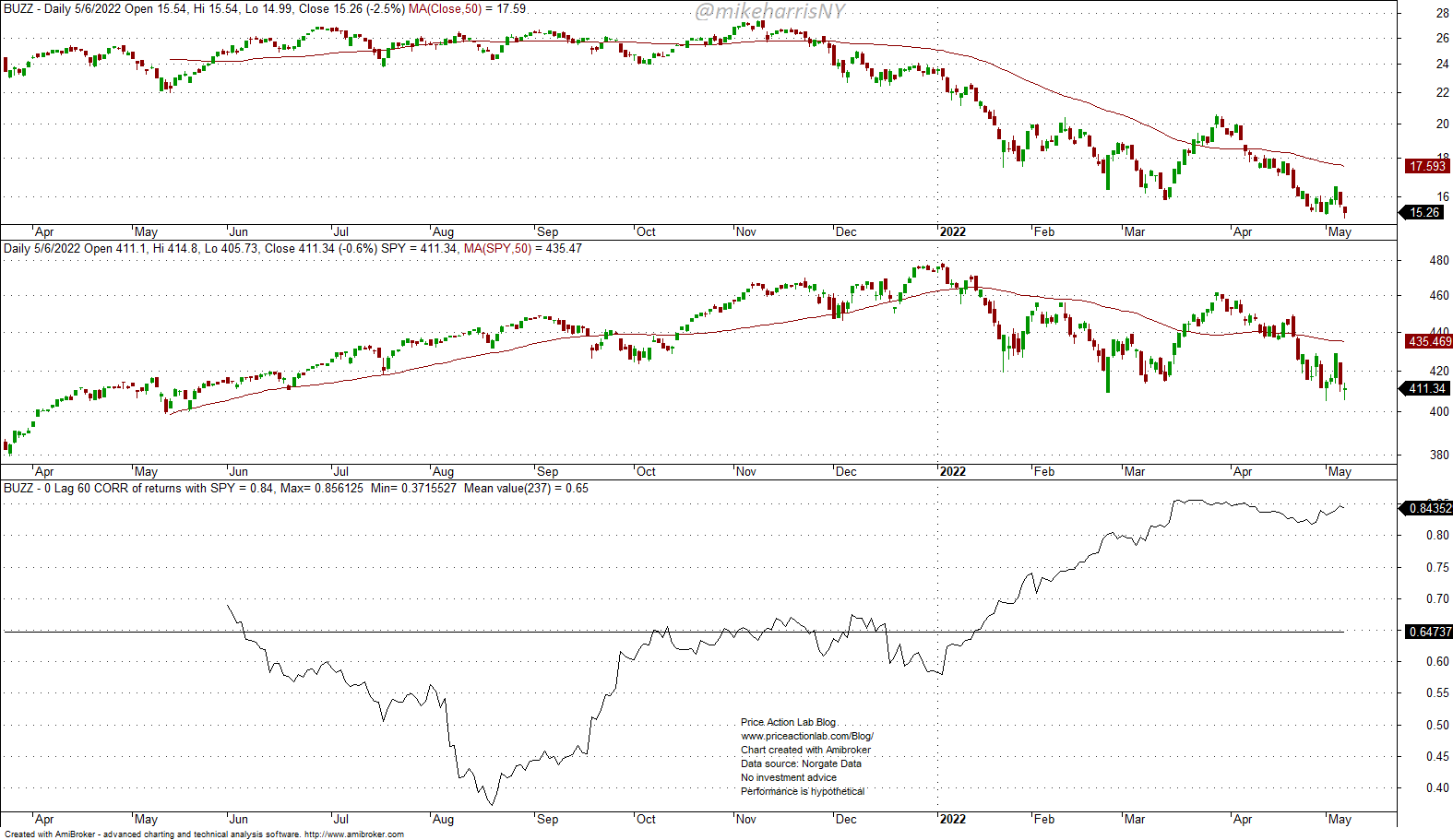

Since mid-August of last year, the 60-day correlation of BUZZ and SPY ETF has been increasing steadily and it’s now at 0.84. The low was 0.37. Therefore, this ETF has a high correlation with the market and this is probably because sentiment is driven by the market and not the other way around.

In the past, some people who develop sentiment indicators contacted me with an offer to work on a project. I looked at the data and there was high randomness, so I declined. Usually in-sample there is plenty of room for curve-fitting by adjusting key parameters that determine the score of social media messages and if that is done after looking at out-of-sample performance, then data-snooping is introduced and there is a high probability of failure in forward samples.

There is also the possibility that sentiment algos may get better in the future after “learning” how to score better. But that may be a slow process.

Premium Content 10% off for blog readers and Twitter followers with coupon NOW10

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS , Email, or Twitter.