Many investors are searching for the next Nvidia, Apple, or Tesla. Naïve diversification may not capture the future big winners. These investors may be better off with passive index investing.

Identifying the next big stock market winners is not trivial at all, and some may argue it is impossible due to market uncertainty and fast-changing regimes. But many try to make their dream a reality: get that stock that will generate 20% or more on average in the next 30 years. This turns out to be an exercise in futility, based on the statistics shown below.

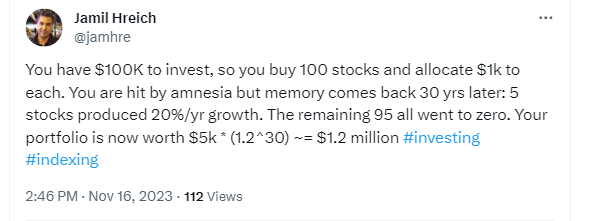

A post on X by a follower was the motivation for this article.

The follower continued with the realization that the annualized return is 8.6%, and this is why indexing works. The posts did a good job summarizing the advantages of passive indexing and the fact that only a select few stocks are responsible for long-term returns. Of course, the prerequisite for passive indexing is some form of “amnesia”. However, since most investors are not amnesiac, as it turns out, passive indexing has high risks, as discussed in this article.

In this article, I use simulations to show that, on average, buy and hold investors who diversify in the hope of catching large winners underperform passive index investors.

For the analysis in the article, we used Norgate data, which includes current and historical constituents for several stock market index indices. Without considering delistings, the analysis in this article would not be realistic. We highly recommend this data service (we do not have a referral arrangement with the company).

The simulation invests randomly in 100 stocks sampled from the S&P 500 and Russell 3000 indexes. These stocks were purchased on January 4, 1993, and held until November 16, 2023, or until they were delisted. The allocation to the 100 stocks is the same in dollar value. In each case, we repeat the simulation 100 times and calculate the statistics. Below are the results of the simulation.

| S&P 500 Index | Russell 3000 Index | |

| Average annualized return | 8.5% | 7.6% |

| Median annualized return | 8.4% | 7.6% |

| Minimum annualized return | 7.2% | 4.6% |

| Maximum annualized return | 10.2% | 10.9% |

| Average maximum drawdown | -38.5% | -37.3% |

| Median average drawdown | -38.5% | -37.4% |

| Minimum average drawdown | -30.5% | -21.3% |

| Maximum average drawdown | -50.6% | -56.3% |

| Buy and hold total return | 9.8% | 9.9% |

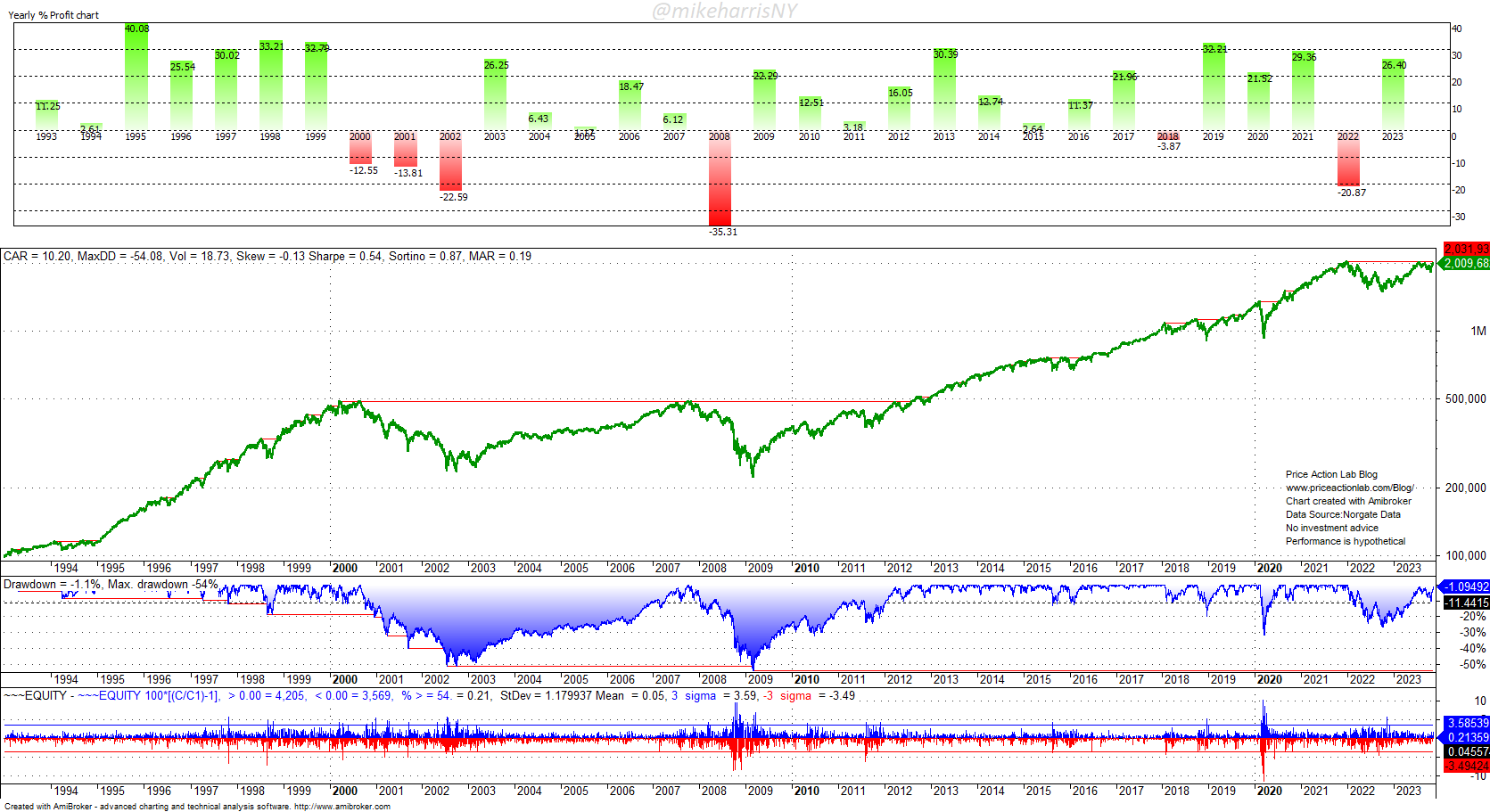

As it is evident from the above table, on average, the diversification into 100 stocks results in annualized return underperformance, which is worse when there are many more alternatives, as in the case of the Russell 3000. More alternatives also mean a higher probability that a large number of stocks will be delisted, either due to going private or due to bankruptcies. Therefore, sampling from the S&P 500 may be better than sampling from a broader index like the Russell 3000, although this may sound counter-intuitive. Buying and holding the S&P 100 may be the best choice since predicting large future winners is impossible. Below is the S&P 100 total return buy and hold performance.

The annualized return is 10.2% and matches the maximum values of the simulations. After all, the S&P 100 is a trading strategy to start with; it involves stock selection by experts and periodic rebalancing.

Summary

The newsletter in the email inbox that claims to forecast the next big winners in the stock market is probably part of a clickbait campaign. There is no way to forecast big winners. On average, investors who attempt to predict which stocks will outperform in the future do worse than passive index investors. Some are luckier than others when they sample broad market indexes for big future winners, but most cannot outperform passive index investing in a more concentrated large-cap index like the S&P 100.

Of course, passive investing requires some form of “amnesia”, as the follower noted at the start of this article. This is the hardest part because this condition hardly exists. In reality, passive investors are gamblers, just like traders. But whereas traders may be gambling for recreation, passive investors may be gambling with their financial futures because, during the next large correction, they may reach the uncle point.

Price Action Lab Blog Premium Content

Subscribe for immediate access to hundreds of articles. Premium Articles subscribers have immediate access to more than two hundred articles, and All in One subscribers have access to all premium articles, books, premium insights, and market signal content.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS, Email, or Twitter.