The impact of dividends on the rolling 30-year S&P 500 total return has been decreasing steadily since the 1960s. Although wealth accumulation in the past relied mainly on dividend reinvestment, nowadays it is more related to share price gains. Depending on how one looks at this fact, it can be good or bad.

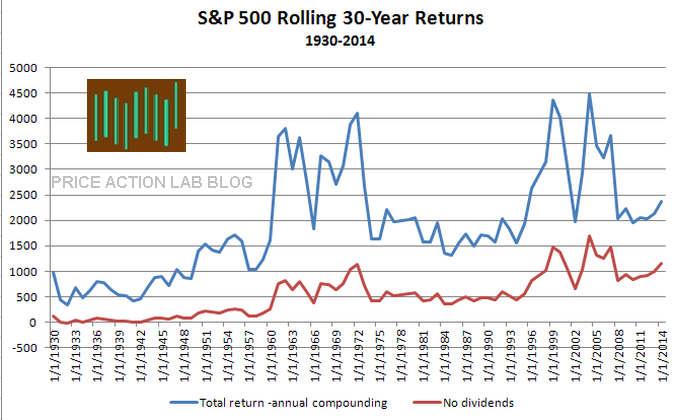

Note that exact total returns figures are difficult to generate due to practical considerations. Below is a chart that shows the S&P 500 rolling 30-year return, total (blue) and with no dividends (red), from 01/1930 to 12/2014:

The effect of dividends on returns is large and that is of course expected. Below are some key statistics:

| Rolling 30-Year | Total return | Without dividends |

| Mean | 1927% | 581% |

| Median | 1715% | 479% |

| Min | 340% (1992) | -15.28% (1932) |

| Max | 4489% (2004) | 1688% (2004) |

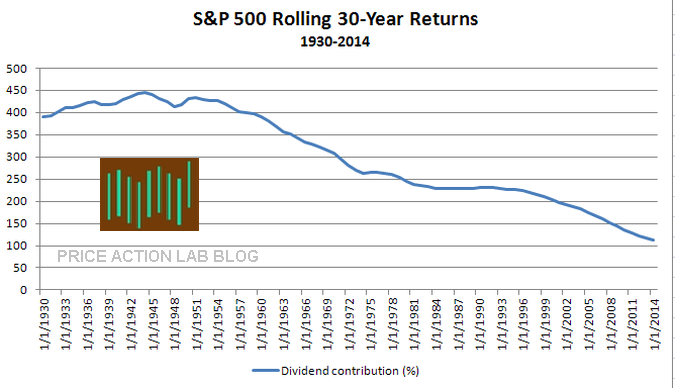

It may be seen from the above table that the impact of dividends is significant. What is not directly evident is how this impact has varied as a function of time. Below is a chart that shows the magnitude of the factor by which dividends have impacted rolling 30-year returns:

A pattern has emerged that is quite significant. For about three decades, from 1930 to 1960, the dividend impact factor was 420% on the average. Since then, this factor has been decreasing in an almost linear fashion and is currently at about 111%. This means that the contributions of dividends and share prices appreciation to the total return are about equal. This is a dramatic change from the past. Is this good or bad?

One thing I know about finance is that everything has two sides, a good and a bad, like every trade has a buyer and a seller. The pattern just identified may mean that:

(A) Longer-term wealth accumulation now relies more on share price appreciation and it is therefore not sustainable.

(B) In the past companies had to pay larger dividends to keep investors but at this point due to higher longer-term expectations, investors will accept a lower dividend impact on total returns because of the potential of future share appreciation.

The maximum 30-year total return of 4489% was realized in 2004. At that time the dividend impact factor was about 200%. This means that the return excluding any dividends was about a third of the total return. At the end of 2014, the two got about even. Obviously, the strong uptrend due to quantitative easing contributed to share appreciation and to a drop in the dividend impact factor. If we accept A above, then it appears that longer-term wealth-appreciation by investing in the S&P 500 will become much more difficult with no support from central banks. However, if we accept B, at some point dividend payments may not matter much as price share appreciation may get explosive.

I do not know the answer. But I choose B. I am an optimist and I hope that we will see Dow 100K in our lifetime. However, I also believe that relying solely on gains from stocks to retire may not be a good idea because volatility may increase and bear market cycles may get longer and more violent. Decisions should not be made based on optimism or wishful thinking but instead should accommodate worst case scenarios.

Subscribe via RSS or Email, or follow us on Twitter.

Charting and backtesting program: Amibroker

Disclaimer

Detailed technical and quantitative analysis of Dow-30 stocks and popular ETFs can be found in our Weekly Premium Report.