A randomization test indicates that a net return for 2013 close to 19% is required to rule out luck at the 95% significance level in the case of SPY trading.

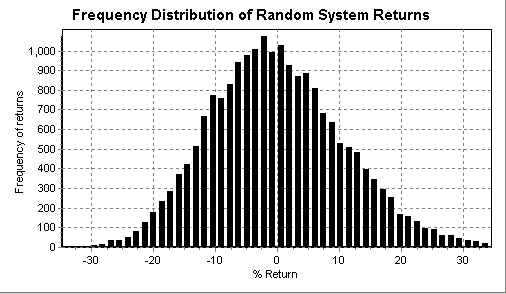

Below is the distribution of returns of 20,000 random SPY long/short trading systems during 2013, fully invested at each position. Commission was not applied for the purpose of obtaining the maximum threshold for a 95% significance level:

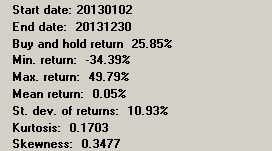

Statistics:

The minimum return for 95% significance is close to 19%. Nearly 48% of all systems generated a positive return and thus SPY trading this year was very rewarding even to gamblers.

The conclusion from this randomization study is that if your SPY trading generated less than 19% in profits the hypothesis that you are lucky vs. skilled cannot be rejected at the 95% significance level. The same threshold may be used as a performance criterion in the case of equity fund management in general but, of course, there may be other ones for the same purpose.

Disclosure: no relevant positions.

Charting program: Amibroker

Disclaimer