When a scan is completed, the results are displayed on the screen.

In the case no strategies are found

In the case no strategies are found based on the scan parameters specified, the following message is shown:

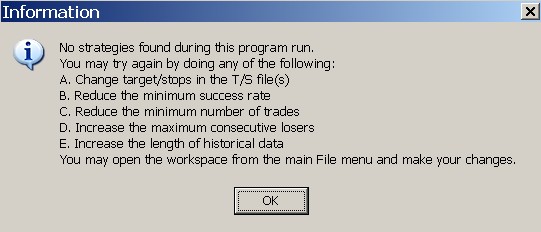

Clicking Help offers general advice on what could be done to increase the chances of finding strategies in the specific data file.

Click OK to close the popup window.

In the case that strategies are found

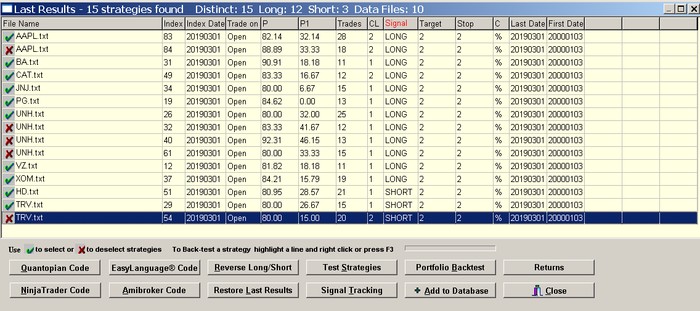

The strategies found by the program are displayed on the results form. Each line represents a strategy with some of its key performance parameters:

Saving the results

To save the results click File on the main menu and then Save. You can also select specific strategies to save in a new results file.

To select specific strategies click the × sign of a strategy line so it turns into the √ sign. In the following example we remove multiple strategies for same symbols:

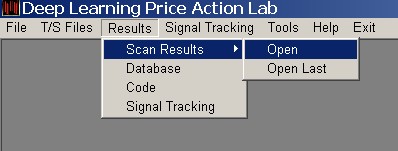

Opening saved results files

To display results already saved click Results from the main program menu, then select Scan Results and then select Open. Open last displays the most recent results generated by the program.

Scan Results Options

The results form offers several options:

Add to Database adds all strategies found to the program database.

QuantopianCode generates Quantopian code for selected strategies.

EasyLanguage Code generates EasyLanguage code for selected strategies.

NinjaTrader Code generates condition code for NinjaTrader selected strategies.

Amibroker Code generates code in Amibroker AFL selected strategies.

Signal Tracking allows adding strategies to a list for monitoring signal generation.

Test Strategies allows bulk strategy testing independent of any selection and updates the results.

Portfolio Backtest allows testing all strategies in the results on a portfolio of securities. (Warning: for the results to make sense, all securities in the portfolio must have the same point value.)

Reverse Long/Short allows reversing the LONG and SHORT type designations of all strategies in the results.

Restore Last results can be used to reload the results generated by the last scan. Useful after operations are performed on the results, such as portfolio backtest or Robustness.

Returns is used to calculate the next bar returns from open to close assuming equal allocation for all signals in the results. Returns are shown under Returns column.

To deselect all strategies from the results click on the File Name column label on the workspace results form. To select all strategies Click again on the File Name column label. To select specific strategies click the × sign of a strategy line so it turns into the √ sign.

Strategy Back-testing

To back-test a strategy, select the strategy line by clicking on it and hit the F3 key or click the right mouse button and select Back-test. To back-test a strategy on a portfolio of securities, select the strategy by clicking on it, then right click mouse and select Back-test portfolio (Warning: for the results to make sense, all securities in the portfolio must have the same point value).

Saving results in .CSV format

The results can be saved in CSV format by clicking File from the main menu and then Save in CSV format.