DLPAL LS can read end-of-day/week and higher timeframe ASCII files with the .txt extension. The data must be in ascending order so that the first line in the file has the oldest date.

Important: File names, excluding the path and the .txt extension, must be less than 26 characters.

The data fields can be single-spaced, comma or semicolon-delimited and have the following order:

Date Open High Low Close

with the date in YYYYMMDD format (example, 20020415). In the case of intraday data, an 8-digit increasing integer index must be used in the place of the Date field [example: index starts at 10000001] and no time field is allowed.

The following is part of a valid daily data file with single space delimited fields:

20020927 30.69 30.72 25.25 26.63

20020928 26.38 30.25 25.59 29.88

20020929 29.19 29.63 27.63 27.94

20021002 28 28.19 25.03 25.25

20021003 25.88 26.13 23 23.25

20021004 22.88 24.81 21.81 24.31

20021005 23.88 24.38 20.38 21.5

20021006 20.94 22.5 18.3 20.81

The following is part of a valid daily data file with comma delimited fields:

20050321,434.50,434.60,429.20,431.40

20050322,431.00,432.80,430.80,431.60

20050323,425.00,428.40,424.50,425.40

20050324,425.50,426.50,424.30,424.80

20050328,425.00,426.20,423.40,426.00

20050329,426.50,426.60,425.90,426.00

20050330,426.20,428.00,426.00,426.90

20050331,430.30,431.40,429.70,431.10

20050401,429.70,431.50,427.10,428.30

The following is part of a valid daily data file with semicolon-delimited fields:

20050211;37.03;37.85;36.93;37.7

20050214;37.7;37.94;37.69;37.87

20050215;37.9;38.48;37.82;38.12

20050216;38.03;38.16;37.83;37.98

20050217;38.05;38.14;37.43;37.47

20050218;37.48;37.57;37.26;37.35

20050222;37.03;37.55;36.79;36.89

20050223;37.04;37.07;36.7;36.94

20050224;36.85;37.44;36.76;37.41

Using Norgate data with DLPAL LS

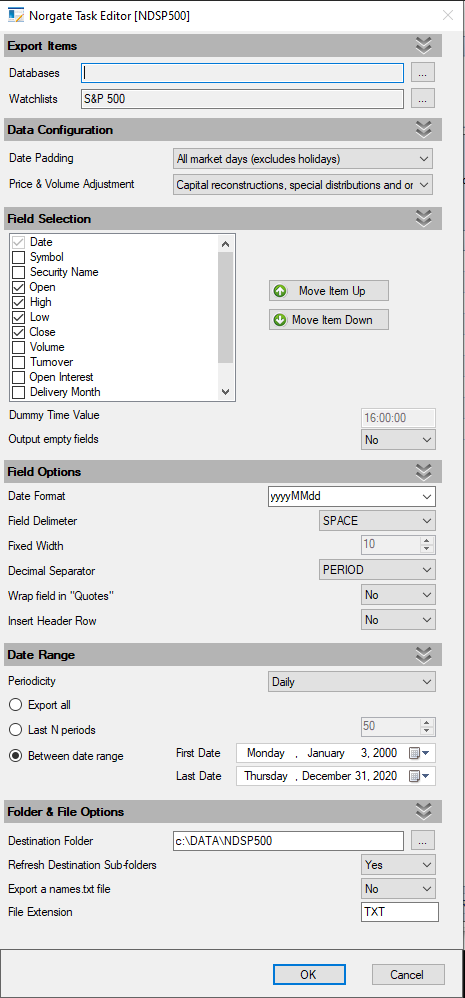

We use Norgate data. For major indexes the data include current and past constituents to remove survivorship bias in backtests. We highly recommend this data service (we do not have a referral arrangement with the company.)

We selected the SP500 watchlist in this example but any other list can be used for other scans.

Note that we start exporting after 1999 because the 90s uptrend introduces a long bias in our analysis and in this particular case we do not want that. In other cases, all available history may be desired.

Also note that we elect to Refresh Destination Sub-folders due to index delistings in this case. When generating signals we would like to have only the active symbols in the export list.

In this particular example we export daily data but weekly are also available.

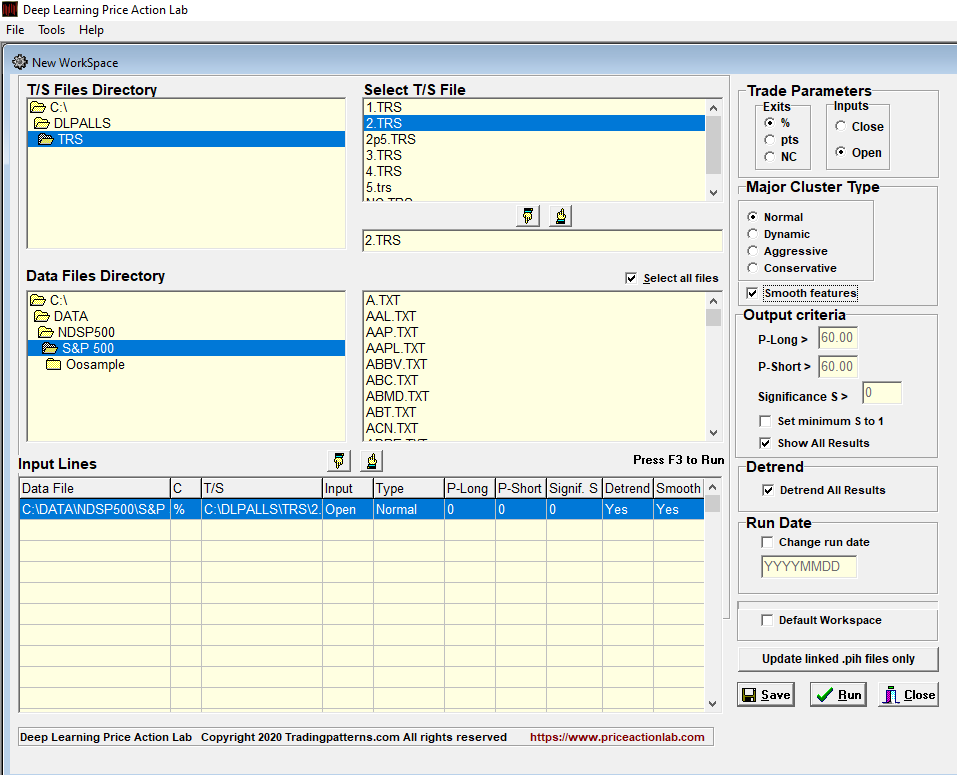

The next step is to use the data in DLPAL LS. Below is an example of a DLPAL LS workspace for calculating features based on the S&P 500 stocks for use in a long/short strategy.

It takes a few minutes every day to update and export the data and then we run DLPAL LS (actually many instances of the program working with multiple watchlists.)

This is how export data for multiple ETFs and run DLPAL LS for daily signals.

In the ETF case we use all available data.