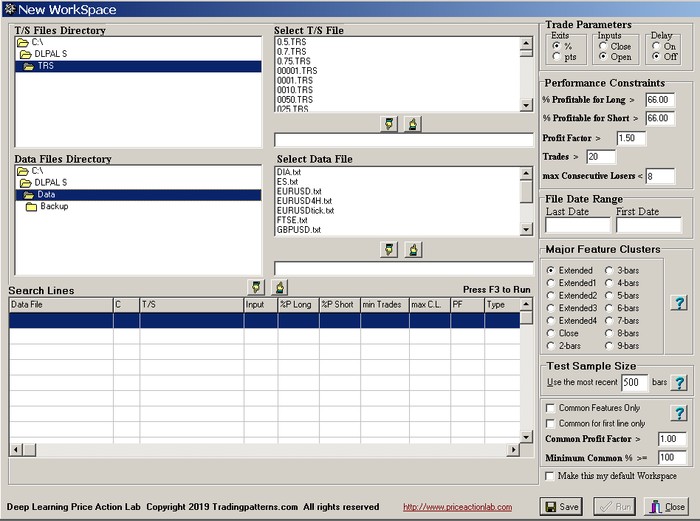

To open an existing search workspace or create a new one

Click File and then click Search Workspace. Select Open Existing Workspace and then click OK. Select a file and then click Open.

To Create a new workspace

Click File, then click Search Workspace, select Create New Workspace and click OK. Then, click on the first empty search line to start the process of parameter selection.

The following must be specified on the workspace for each separate search line:

1. T/S file

2. Data file (must have proper format)

3. Trade parameters: Exits based on percentages (%) or points (pys) of entry price, trade inputs on Open or Close and option to apply trade input delay

4. Performance Constraints: Minimum success rate for long and short strategies, minimum Profit Factor (sum of winners/sum of losers) minimum number of historical trades and maximum number of consecutive losers

5.Major Features Cluster: Choice of major features cluster

6. Test Sample Size: The number of bars in the data file, or bars, to be used for test sample. Recommended value is the default of 500 bars for daily data. In the case of intraday data the value will depend on the timeframe.

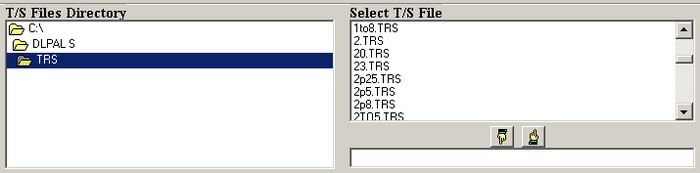

To Select a T/S file

Select a T/S file from the appropriate directory. Click on a file to highlight it and then click the hand icon pointing down to move it in the selection field. Alternatively, you can just doubleclick a file and it will automatically get selected. To change the T/S file click the hand icon pointing up and repeat the selection process.

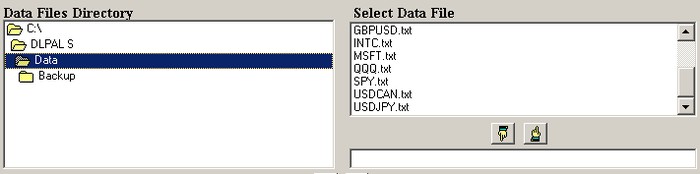

To Select a data file

Select a data file from the appropriate directory. Click on a file to highlight it and then click the hand icon pointing down to move it in the selection field. Alternatively, you can just doubleclick a file and it will automatically get selected. To change a data file click the hand icon pointing up and repeat the selection process.

Trade Parameters and Performance Constraints

Specify the type of exits (profit target and stop-loss) to use by selecting either % for percentages of entry price or inc for points (pts) added to entry price. Specify the type of trade input by selecting either Open or Close. If Open is selected then the entry price will be the open of the bar following a signal generation by a strategy. If Close is specified, then the entry price will be the close of the bar where a signal is generated.

Specify if you want to apply a delay in the trade input of strategies. To select a delay, check the On option under Delay and specify the delay range. Allowable values are 1 – 5.

Note: If you check On for the delay and specify a range for this variable DLPAL will determine the best value for the delay to apply for each strategy. In many cases, DLPAL may discover more strategies as compared to a search with no delay applied.

Warning! Activating the delay option may slow down the search considerably. It is recommended that the default range (1-5) is used.

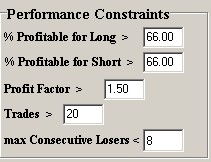

Specify the minimum % profitable (success rate) for long and short strategies by inputting the appropriate value to use in the fields. This parameter is equal to the number of winning trades divided by the total number of trades multiplies by 100. (The defaults are set to 66.00.) Then, specify the minimum Profit Factor, which is equal to the sum of winning trades divided by the sum of losing trades). Next specify the minimum number of trades strategies must generate in the train and test sample combined. (The default is 20 trades). Finally, specify the maximum number of consecutive losers each strategy is allowed to have in the combined data sample, max Consecutive Losers. (Default is 3 consecutive losers and shown as “< 4”). These performance constraints will apply to all strategies identified by the program and only those that meet them will be reported on the results..

File Data Range

As soon as a data file is selected, the date range of the combined sample, train plus test, is automatically shown in the First Date and Last Date fields. These fields cannot be changed.

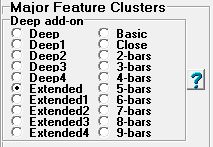

Major Cluster Types

Extended: 120 sub-clusters with 2-6 bar lookback

Extended1 – Extended4: 30 sub-clusters each with 2-6 bar lookback

Note: Extended1+Extended2+Extended3+Extended4 = Extended

Close: 67 sub-clusters with 3-9 bar lookback. Only the Closing prices is used

2-bars: 24 sub-clusters with 2 bar lookback

3-bars: 41 sub-clusters with 3 bar lookback

4-bars: 31 sub-clusters with 4 bar lookback

5-bars: 47 sub-clusters with 5 bar lookback

6-bars: 54 sub-clusters with 6 bar lookback

7-bars: 74 sub-clusters with 7 bar lookback

8-bars: 114 sub-clusters with 8 bar lookback

9-bars: 171 sub-clusters with 9 bar lookback

Deep: 616 sub-clusters with 9 bar lookback

Deep1 – Deep4: 154 sub-clusters each with 9 bar lookback

Note: Deep1+Deep2+Deep3+Deep4 = Deep

Note that: Number of sub-clusters in Close+Mixed+High Low+Open Close = Number of sub-clusters in Deep

Test Sample Size, Common Features Only, Common Profit Factor, Minimum Common % and Default Workspace

The default Test Sample Size is 500 bars. Changing this parameter impacts the time taken to complete the search. A minimum of 250 bars is recommended in the case of daily data. Note that this parameter is not related to the back-testing range used during the search, which considers the combined sample.

Checking the option Common Features Only instructs the program to look for strategies in each instrument on the workspace that are also profitable in all other instruments. This works as follows: when the program finds a strategy in one instrument that satisfies the criteria set on the workspace, it also backtests its performance in all other instruments using the parameters of the original instrument (target, stop, etc.). If the profit factors calculated is greater than the minimum Common Profit Factor (default is 1.00), then the strategy is reported in the results. Notes: (1) The chances of finding strategies with common features decreases with the number of instruments and as the Common Profit Factor value is increased. (2) When this option is selected, all data files on the workspace must have the same point value in the case point stops are used. For example, when using currency pairs with point stops (pips), often EURUSD and USDJPY have different point values. These must be adjusted in the historical file before the search for common features so that a point stop of 0.01 in EURUSD ( 100 pips), for example, also corresponds to the same number of pips in USDJPY.

The default Minimum Common % is 100. In this case each strategy found will have the minimum profit factor specified in all instruments tested. This value can be set to anything between 0 and 100. For example, if the value is set to 75, then all strategies with common features reported will have the minimum profit factor in at least 75% of the instruments tested.

Note:

Use “Common for first line only” to find common features for symbol in first search line.

The Test Sample Size, delay option values and the parameters related to common features are not saved when the workspace is saved.

Default workspace

You may mark a workspace as the default workspace of the program by checking the box next to Make this my default workspace.

Creating a Search Line

To create a new search line, click on the first empty search line. After the file and parameter selections click on the hand icon pointing downwards. To delete a search line, click on that line and hit the DEL key, or use the hand icon pointing upwards to remove it.

Saving the workspace and Running a search

Click Save to save the workspace. Click Run or hit the F3 key to start the search.